First thing’s first. Here’s the only chart you need to make sense of the two-day risk-on move (i.e. the rally):

You’ll likely see several versions of that throughout the rest of the day assuming equities hang on to outsized gains.

Basically, Treasurys aren’t buying what stocks err … aren’t selling. Ok, that’s a confused attempt at a double entendre. Let’s try again: Treasurys are holding up and yields remain largely suppressed even as stocks soar. Here’s another way of conceptualizing it:

What you see there is a measure of euro bank default risk graphed with the 10Y German bund yield. Take a look at the lower right-hand corner. See how the blue line rose sharply on Tuesday but the orange line continued to fall? Well, the left scale is inverted, so when the blue line rises, it signals that the market is pricing in less risk among European banks (the real trouble spot). That should be accompanied by rising yields on German bonds (i.e. risk-on sentiment). But it wasn’t.

The fact that you haven’t seen yields on safe haven securities rise markedly over the past two days suggests some folks are still pretty anxious. The relatively “high” yield on US paper versus Japanese government bonds is probably keeping a bid under the UST market, but then again, yields are lower on Japanese government bonds too (as an aside, 85% of the JGB curve is now negative). Here’s a bit of color from Bloomberg that describes the overnight trade:

“Long-end of the Treasury curve continues to outperform, while yields across front-end creep higher. Large buying of long-end out of foreign real money pushed curve flatter in overnight session, similar flow seen in yday’s session, says trader. Japanese accounts seen buying 10Y in London session, domestic names have been selling in the belly, says one trader in southern Europe. Core EGBs, USTs have been resilient despite sharp rally in risk assets. Sharp rally in Gilts, boosts Bund futures to session highs, supporting U.S. 10Y notes.”

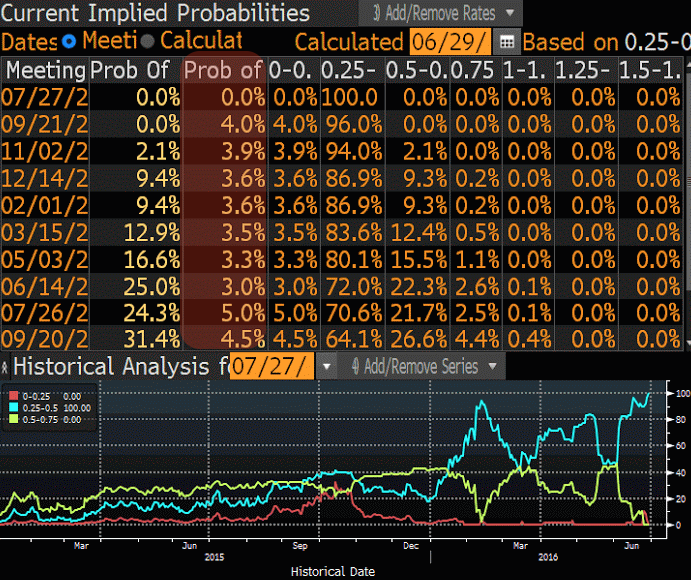

So what gives? Well, it’s starting to look like we’re reverting back to the old “bad news is good news” dynamic vis-a-vis markets and central banks. That is, the Brexit plunge pretty much guarantees further stimulus from the ECB and the BoJ and perhaps even from the Fed. In fact, the market is now pricing in a chance of a Fed cut in September!

Yesterday:

(Bloomberg)

And today:

(Bloomberg)

So they’ve come in a little, but you get the point. The market now thinks there’s a chance the Fed will ultimately be forced to reverse course. This just weeks after everyone and their brother thought a June hike was a foregone conclusion.

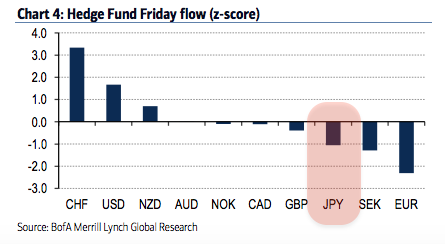

We can all talk until we’re blue in the face about whether the fact that wild swings in capital markets impact the real economy means policymakers should explicitly include financial conditions in their reaction function, but the reality is, policy is increasingly beholden to risk assets. Have a look, for instance, at what hedge funds were selling last Friday:

(Chart: BofAML)

Now why, you might ask, would anyone want to sell the yen (a veritable sponge for safe haven flows) in the wake of a destabilizing event like the Brexit vote? Well, probably because they think the uncertainty surrounding a tail event like the results of the UK referendum will force Japan to either intervene in FX markets pushing the yen lower (weaker) or else launch more stimulus. So what you see in the chart above is likely hedge funds trying to skate ahead of the monetary policy puck, so to speak.

But the faith in more of the same with regard to accommodative monetary policy seems misplaced at this juncture. As we’ve seen, it’s becoming less effective with each successive iteration.

Throw in the fact that the market’s newfound exuberance may be at least partially attributable to quarter-end window dressing and you’ve painted yourself a picture that screams “sucker’s rally.” On that note, we’ll close with a bit from Bloomberg’s Richard Breslow:

“I was thinking about the long weekend. Not the U.S. Independence Day holiday, the timing and name of which seems infused with taunting irony after the EU referendum. Rather, last New Year’s Eve.”

“Back then, markets played the quarter (year) end card of putting money to work and making balance sheets look as robust and engaged as possible. A snapshot and performance fees trump a thousand measures of caution or reality. And then there was January.”