If you had no idea how the Brexit vote turned out, you could certainly surmise what happened just by glancing at the following chart:

What do you see? That’s right, a stronger dollar, a stronger yen, and sharp declines in the Chinese yuan and British pound.

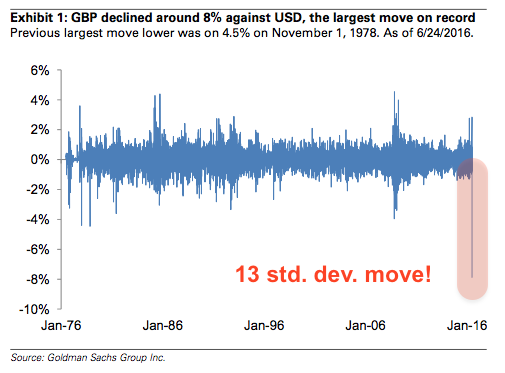

Actually it’s not entirely accurate to call the pound’s decline “sharp.” It’s historic. Harrowing. And statistically speaking, so anomalous that it technically shouldn’t have been possible:

(Chart: Goldman, with additions)

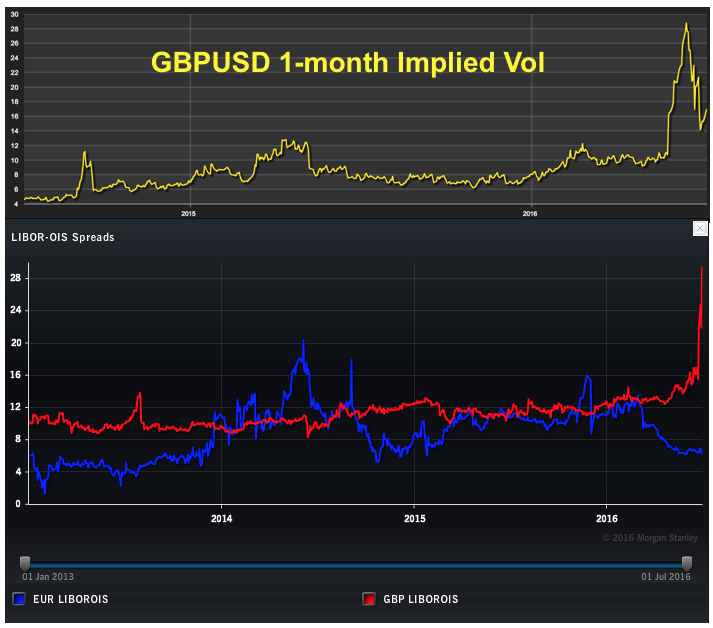

Needless to say, GBP vol and sterling LIBOR-OIS spiked - hard:

Now you might not care a whole lot about cable and you likely don’t care at all about British money markets (you probably don’t plan on becoming a British bank any time in the near future), but make no mistake, you should pay attention to what’s going on with the pound and, more broadly, what’s going in the post-referendum UK.

For anyone who might have missed it, the gates have gone up on more than a half dozen UK real estate funds. Translation: investors can’t get their money out.

The problem is pretty simple. Everyone and their brother thinks London property values are likely to fall steeply in the event the UK packs up and leaves the EU. Investors in real estate funds don’t want to stick around for that, so the redemptions starting rolling in. Of course asset managers don’t hold enough cash and/or cash equivalents to meet a sudden surge of withdrawal requests. If they did, they couldn’t put money to work in the assets that their investors want exposure to. But when those assets are illiquid and suddenly everyone wants their money back, managers have no choice but to gate. Put simply: it’s not so easy to sell an overvalued office building into an inflated market on the heels of a black swan event like the UK referendum results. Here’s Bloomberg with a bit of color:

“Aberdeen Fund Managers Ltd. cut the value of a property fund by 17 percent and suspended redemptions so that investors who asked for their money back have time to reconsider.”

“‘Shareholders wishing to redeem will do so at a price which is subject to the above dilution adjustment in order to reflect the current market environment and the fact that short-term trading in the property market has relatively penal consequences,’ the firm said.”

Yes, “penal consequences.” Like having your money locked up in illiquid assets that are falling in value.

This eventually becomes a self-fulfilling prophecy. If you’re in a real estate fund and you see other funds suspending redemptions, what’s the first thing you’re going to do? You’re going to ask for your money back. Before you know it, your manager has to gate too. And so on.

“So what? I don’t have any money in London real estate,” you might be thinking. Trust us when we tell you that risk will not be happy if the UK real estate market collapses. And neither, in all likelihood, will the pound which Goldman and Deutsche Bank are out gloomy on this week. Here’s Goldman:

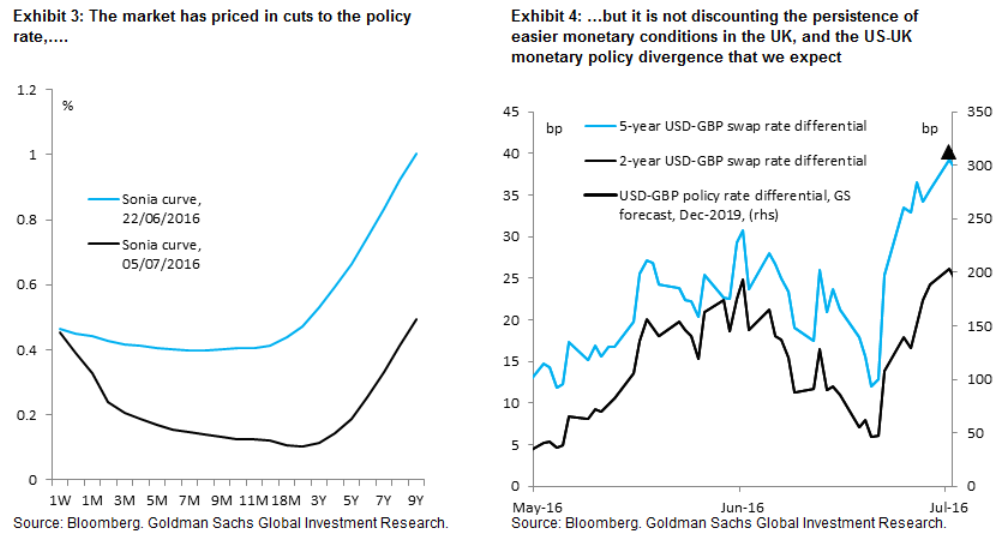

“The uncertainty created by the Brexit vote constitutes a material negative shock to the UK economy, one that requires a monetary policy response, not least given the political vacuum until September. Our UK economist Andrew Benito expects the Bank of England to announce asset purchases worth £100bn at the August 4 meeting, together with a 25bp cut to the policy rate. Further, it is possible that there will be a number of dovish dissents at the July 14 meeting and that the minutes will be exceptionally dovish, so that – to a material degree – August 4 easing could be pre-announced next week. This is why our new forecast front-loads GBP weakness, with GBP/$ at 1.20, 1.21 and 1.25 in 3, 6 and 12 months and EUR/GBP at 0.90, 0.86 and 0.80 over the same time frame.”

Deutsche is even more pessimistic:

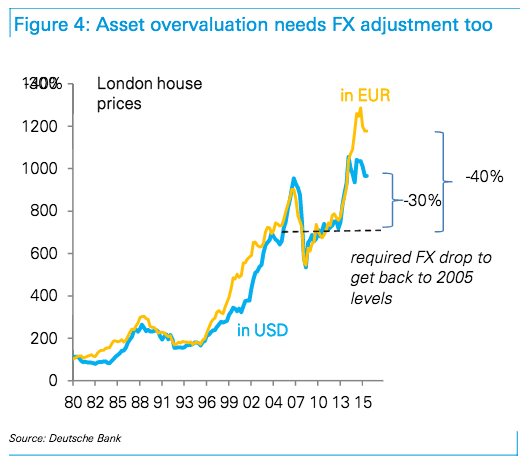

“Our forecasts for GBP/USD looks aggressive at 1.15 by the end of this year respectively, but how did we arrive at these numbers? A starting point is purchasing power parity (PPP), which measures the exchange rate that equates the price of a ‘big mac’ between two countries. Our assumption is that the UK is undergoing an unparalleled negative ‘terms of trade’ shock, which requires GBP to reach historical (under)valuation extremes. As the charts below show, there is much more to go before GBP is considered excessively ‘cheap’. Even a move down to 1.10 in GBP/USD and 1.03 in EUR/GBP would only take sterling to 20% PPP valuation extremes that have not been uncommon in the past.”

(Chart: Deutsche Bank)

And just how much would the pound need to fall in order for foreign investors to rush in and put a bid in under the London property market thus helping to arrest a potential slide? Well, a whole lot:

(Chart: Deutsche Bank)

So even after a 13-sigma drop and ensuing grind lower for GBP, “big macs” are still too expensive in the UK. So are “big” buildings.

Now who’s next of the list of funds suspending redemptions?

2 Comments

Vicky W.

July 7, 2016What does "PPP" stand for please?

TheoTrade Support

July 7, 2016Purchasing Power Parity