Election 2020 Hedging Edition

Many investors are nervous about the upcoming election. Do we know who wins on November 3rd or 4th? Heck, will we even know by the end of the month? Also, what will the market’s response be to the election results?

There is definitely more questions than answers and even if the election results are in on November 3, there isn’t going to be a binary response by the markets. For example, a Biden win may certainly lead to higher deficits and more Federal Reserve monetization, but what if there’s a Republican Senate? Ultimately, it may take a week or so after the results are in to sift through the ashes and see how the market is responding.

The big take-away from this introduction has to be that it may be reasonable to hedge some of your risk, but how? Hopefully, this will be a definitive guide for your election day hedges.

Election Hedge Precursors

In a previous post I outlined some of the steps to hedging and some of the current limitations of a great hedging strategy called The Atomic Hedge. Because volatility is always changing, strategies need to be fluid. Since the volatility cat is effectively out of the bag, The Atomic Hedge isn’t the best approach in this environment. Don’t worry though, we got you covered.

In that post I outlined the following first steps before a hedging strategy should be considered. Here are a couple questions you’ll want to answer:

- Which instrument best reflects your portfolio risk?

- What is your beta-weighted portfolio delta?

- What percentage of your portfolio are you hedging?

Election Hedge Step 1

The first question comes down to what major market index or sector represents your portfolio the most. For example, a tech-heavy portfolio may decide to use the Nasdaq 100 index option, futures, or ETF as an instrument. Do you have a 2040 fund in your 401K? Then the S&P 500 index may be the best index option, futures, or ETF to hedge your risk.

Election Hedge Step 2

The second question will likely need to be answered by using a software. In our online classes we use the portfolio beta-weighting feature of TD Ameritrade’s thinkorswim software.

This type of tool can translate your holdings or simulated holdings into a delta using another product that you plan to use as a hedge. For example, this type of tool will estimate how much your portfolio will change with a $1 change in the SPDR® S&P 500® ETF Trust (NYSEARCA: SPY). Beta-weighting to the SPY represents the most common approach for most investors.

Election Hedge Step 3

The last question deals with how much protection you will need. The typical knee-jerk response to this question is 100%. If that’s the case, you don’t need to hedge, you need to sell and go to cash. If you’re plan is to remain long then you’ll hedge something less than 100%. A typical hedge is 30-40% of your beta-weighted delta.

Now that you know your instrument, your beta-weighted delta and the percentage of your hedge, you’re ready to pick your tool.

Election Hedge Tools

With any job there is a tool, and an election hedge is no different. This job has two possible tools to use:

- Futures

- Options

In this post, I’m going to outline both approaches. However, using futures requires you to have authorization and a funded futures account. That may take several days to setup and with the election happening tomorrow, it may be too late to quickly implement.

Election Hedge with Futures

This may not be your first election hedge choice if you’ve never traded or hedged with futures before.

Futures can be a great way to remove directional risk quickly and efficiently. However, if your portfolio is made up of a lot of option trades, it can get a little tricky. This is because futures are a hard delta hedge against the backdrop of a soft delta portfolio. This means that your portfolio delta of your option trades may change quickly and thus your hedging needs may change quickly change as well. Using futures in this instance may force you to be on your toes.

The process of hedging using futures is simple once you know how many deltas you need to remove. Depending on the number of deltas being hedged, you’ll use one of two futures products:

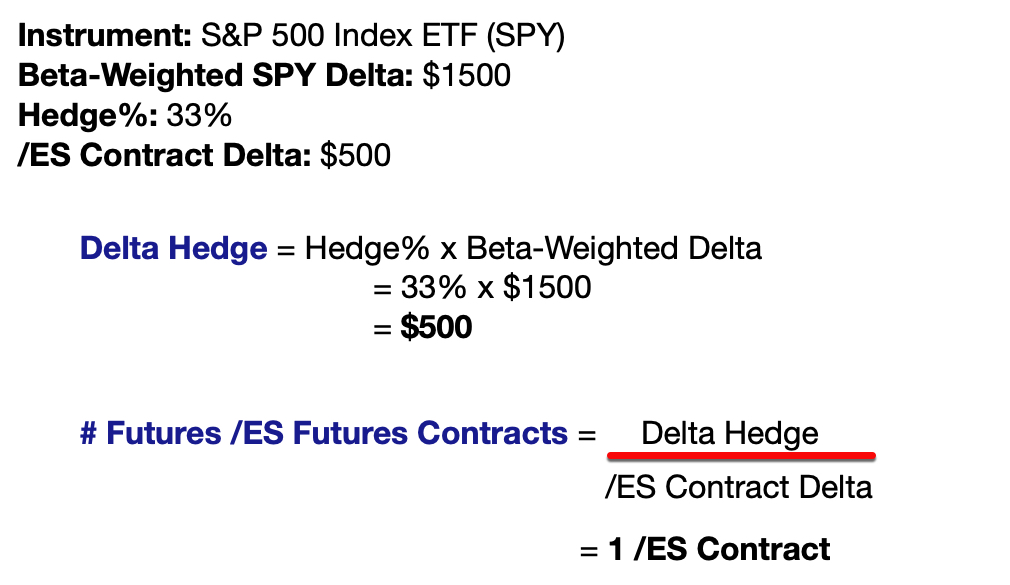

- E-mini S&P 500 Index Futures (Symbol: /ES)

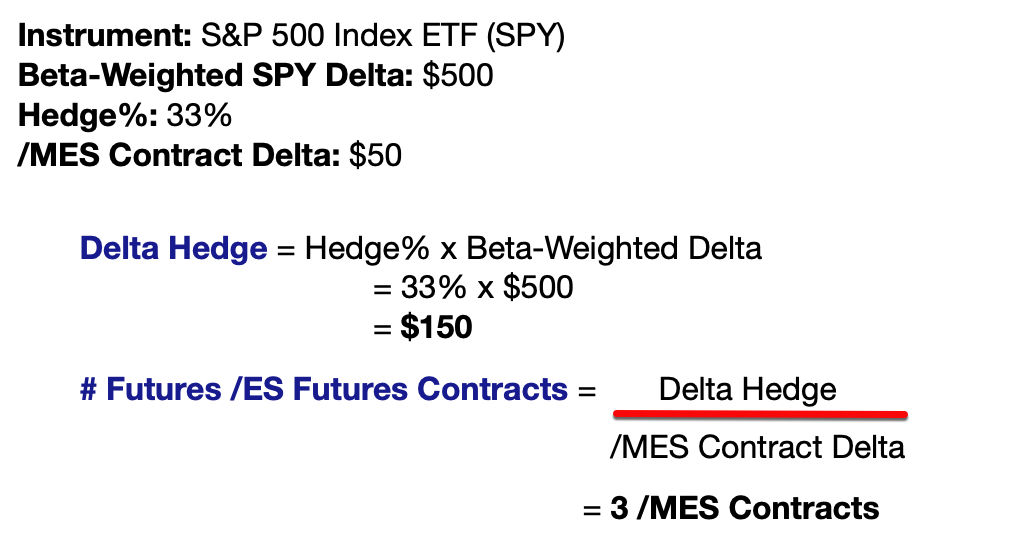

- Micro E-mini S&P 500 Index Futures (Symbol: /MES)

One /ES mini futures contract hedges 500 SPY deltas. Thus, selling one /ES futures contract lowers your SPY beta-weighted delta by $500. Because of the large incremental value, you would need to have a minimum hedging need of 500 SPY deltas to use it. Here’s an example:

One /MES micro futures contract hedges 50 SPY deltas. Thus, selling one /MES contract lowers your SPY beta-weighted delta by $50. Here’s an example:

You can see that the math is really straightforward once you’ve completed the first couple steps!

Futures provides a constant delta hedge. That means that if you’re hedging $150 SPY deltas, it will always hedge $150 SPY deltas. Once you’re through the period of concern, the hedge would need to be bought back to close.

Election Hedge with Options

For most investors, options may be the first and only choice when hedging. In an ideal world, hedging should come at zero out of pocket cost using The Atomic Hedge or other techniques that we teach at TheoTrade. However, we’re now in a high volatility environment and the technique has to be modified and will require some out of pocket cost.

If you were to choose an option contract that is most closely related to a futures contract, it would be a deep ITM long put. Since we’re talking an even that is taking place tomorrow, you may only need one to two weeks of protection. Here are a couple of rules for setting up this put option hedge:

- Pick an expiration with one to two weeks to expiration

- Pick an option with a -0.85 to -0.95 delta

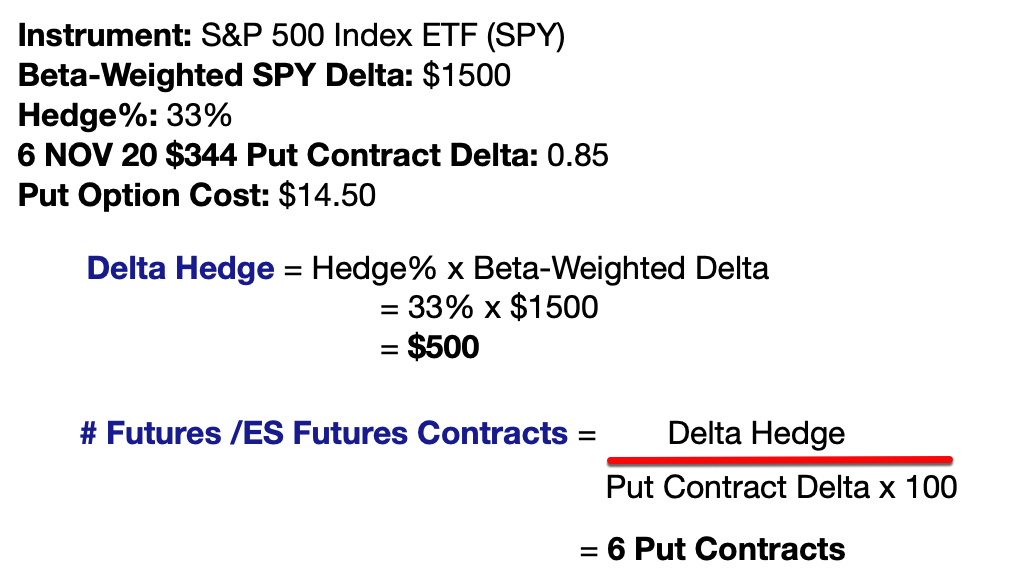

Things may not be resolved quickly after the election, but the option can be rolled to give you more time as you approach expiration. Here’s an example using this type of hedge:

Doing the math above leaves you with 5.88 6 NOV 20 $344 SPY put option contracts. You an make the choice whether you want to round up or down. This hedge costs $1450 per contract, but the option only has $1.05 or $105 per contract of extrinsic value that will be lost by expiration if the price remains the same. The rest of the value will be lost by a rise in the price of SPY, which is what you want to have happen. Hedges are hedges, and we’re not trying to make money on them.

The hedging power of the put contact will remain pretty firm since it is starting out with close to a -1.0 delta. However, with a significant rise in the price of SPY, the delta will diminish and go to zero if the option is OTM by expiration. However, that means that the price of the SPY has risen above $344 and your portfolio made money.

Conclusion

This powerful election hedge strategy can be great for those carrying a long stock portfolio into a high volatility, uncertain market climate. Hopefully this gave you a foundation for understanding some of the ways to hedge and the tools for doing the hedging.

Don Kaufman spent over an hour discussing the market and this hedging strategy this morning on TheoTrade for our subscribers. Learn from the best at TheoTrade!

Learn how to deal with uncertain markets by learning about the Vomma Zone.