To Hedge or Not to Hedge

A lot of questions from our subscribers came in yesterday about how to hedge and whether they were too late to do it. It’s pretty typical for investors to think about hedging as the sell-off is occurring or after its over. One of the important points to make about hedging is to hedge earlier in the move. However, what do you do when your knee deep in positive delta and the selling may not be over yet?

It’s at these points in time when your options may become more limited and some approaches may get more expensive. Hopefully this post will help address an approach to using options as a hedge.

The ‘Atomic Hedge’

First rule of naming a strategy is to come up with something that’s both catch and descriptive. Don Kaufman did that in spades with the name of this strategy. An Atomic Hedge is a variation of a collar strategy that involves selling calls and buying puts, but with a twist.

The intent of this approach is to capitalize on the skew of the options market on products like the SPDR® S&P 500® ETF (NYSEARCA: SPY) and hedge portfolio level risk. As you begin considering what type of hedge to use or how much, there are a few steps to do first. Here’s are the beginning steps in this process:

- Product Selection

- Notional Value of Your Portfolio

- Translate the number of shares to options contracts

First Steps to the Hedge

These first few steps are important since you need to determine what instrument should be used as a hedge. For example, if you own a bunch of tech stocks, maybe a Nasdaq 100 product would be appropriate. If you’re mostly large cap stocks or funds, then an S&P 500 product would be appropriate.

Once you know what index or sector best reflects your holdings, the next step is to understand your directional risk. This is first understood by looking at the total portfolio value of your stock or equity fund holdings. The next step is to translate that into your benchmark index or sector.

Platforms like thinkorswim by TD Ameritrade have tools that will allow you to translate your portfolio delta into a product like the SPY. Using the beta-weighted portfolio delta can translate your portfolio risk in terms of the SPY. For example, if the SPY declines $1 you can estimate how much your portfolio will lose.

Cost of Hedging

Once you know your directional risk, you can now translate that into an option contract. For example, if your beta-weighted SPY delta is $500, a 0.30 delta put option will theoretically lower your directional risk by $30 to $470. This understanding allows you to know how many puts you would want to buy. It’s typical to hedge around 30-40% of your beta-weighted delta.

Buying puts can get expensive as a hedge. Also, as the market falls and the VIX rises, the cost of puts increase significantly. This is where the Atomic Hedge comes in. BY selling OTM call option premium, the credit can cover all or part of the put premium.

In a low volatility environment, before the sell-off begins, this can be easily done. However, the hedging dynamics change once the volatility cat is out of the proverbial bag.

The Atomic Hedge can always be entered at a Zero net cost to the hedger. In this strategy, an OTM call vertical spread is sold that will cover the OTM put that your purchasing. Since you’re using a call vertical to pay for the put, you’ll need to sell twice as many call spreads as put spreads. Usually buying a put and selling a call around a 0.30 delta is a good starting point.

Too Late to Hedge?

Now you have some remedial understanding of the Atomic Hedge, let’s take a look at how it changes once the VIX has risen sharply.

Here’s an example of an atomic hedge today on the SPY using the thinkorswim platform:

With a current SPY price of $329.24, the call spread is nearly $15 OTM and has a $14 spread width. The put option is just over $19 OTM.

Let’s take a look at the pricing of the same trade on October 13, just as the current sell-off was getting started.

The SPY closed at $350.13 that day and the put strike was $19 OTM. The short call was $15 OTM with a $16 spread. You may notice that the distance of the put and the strike width of the spread is pretty similar. The put option is the same distance because the rise in implied volatility has been offset by the time decay of the option. The call vertical has a tighter spread because the skew has risen and the lesser amount of time to expiration.

The wider spread of the Short call vertical also does something, it increases the amount of margin required for the trade. This happens because the strike width between the two call options is around $14 instead closer to $4 to $6 when the VIX is closer to 12.

While the pricing hasn’t changed much since October 13, the pricing is still difficult because of the relatively high VOX coming into the sell-off. The spread does its job, but it comes at a cost of more downside risk and removes more upside potential if the market rallies.

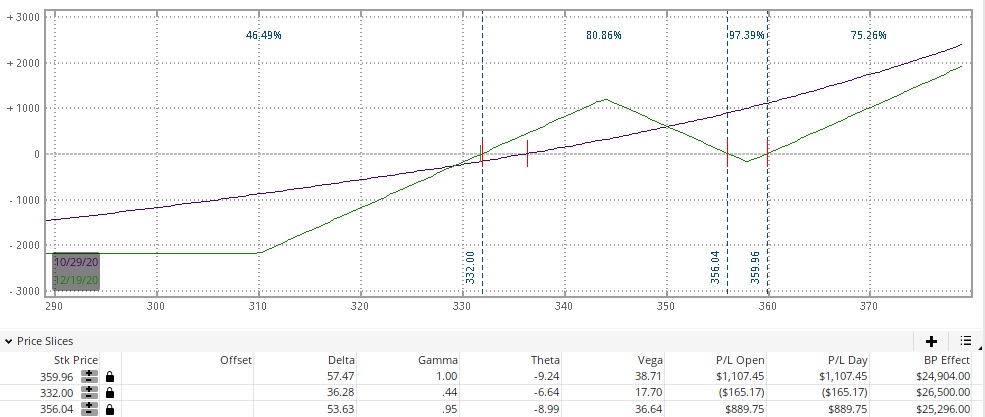

Hedge Optics

Looking at one-contract Atomic Hedge against 100 shares of the SPY yields the following P/L graph. It does it’s job by removing all of the risk for the SPY or a 100 beta-weighted delta’s, but it does it by brute force. The trade-off is the removal of a significant amount of upside in the event the market rallies significantly. The $14 range between $344 to $358 is a big trade-off.

That being said, while not ideal in the current environment, it may work for some investors.

Alternative Hedges

An alternative approach, that is more of a 1:1 hedge, is the Micro E-mini S&P 500 Index futures. Shorting the micros will remove 50 SPY deltas for every contract.

For example, if your beta-weighted SPY delta is 500 and you’re looking to lower that exposure by 50% or 250 SPY deltas, you could short five contracts of the micros. Using futures doesn’t remove all of your risk unless you increase the number of contracts. However, it’s a liquid market that allows you to dial up or down the risk.

Conclusion

The failure of the VIX to fall back to historical levels has made it more expensive to hedge with options. Either it’s increasing the cost or you’re sacrificing additional upside to get the protection you need. The Atomic Hedge is a way to hedge your risk in any market, but for some traders, the use of alternative strategies, like futures, may be preferable.

We have a three-hour course on this and other hedging strategies on TheoTrade. Subscribe today and get immediate access to our entire archive of classes and strategies.

Wondering when to hedge? See how unlocking the Vomma Zone can help you better understand when volatility is about to rise.