Guide to Using the VIX Volatility Spread (VVS)

We had an open house yesterday at TheoTrade and it was great to have so many people join us. It’s nice to give people a look behind the curtain of what we do.

If you participated, you saw Don Kaufman walk through a trading strategy called the VIX Volatility Spread (VVS). His approach is based on capitalizing on a dramatic move higher in the index. If you’re familiar with the index you know that it rises as the market falls. This trade can be added at little to no cost. Also, this trading opportunity just opened up again after the VIX fell following Tuesday’s election.

What is the VIX

The Cboe Volatility Index (VIX) is an index that tracks the average 30-day implied volatility of the S&P 500 Index options. Implied volatility is significant in that it reflects traders’ expectations of future volatility in the index.

Because the VIX reflects future expected movement, you would expect it moves counter to the price of the SPX. Meaning, as the SPX is falling, volatility and expectations of future movement increase. This is a result of institutional investors buying puts to cut their directional risk when the market is falling. A surge in buying options causes the price of the options to increase and the implied volatility to surge.

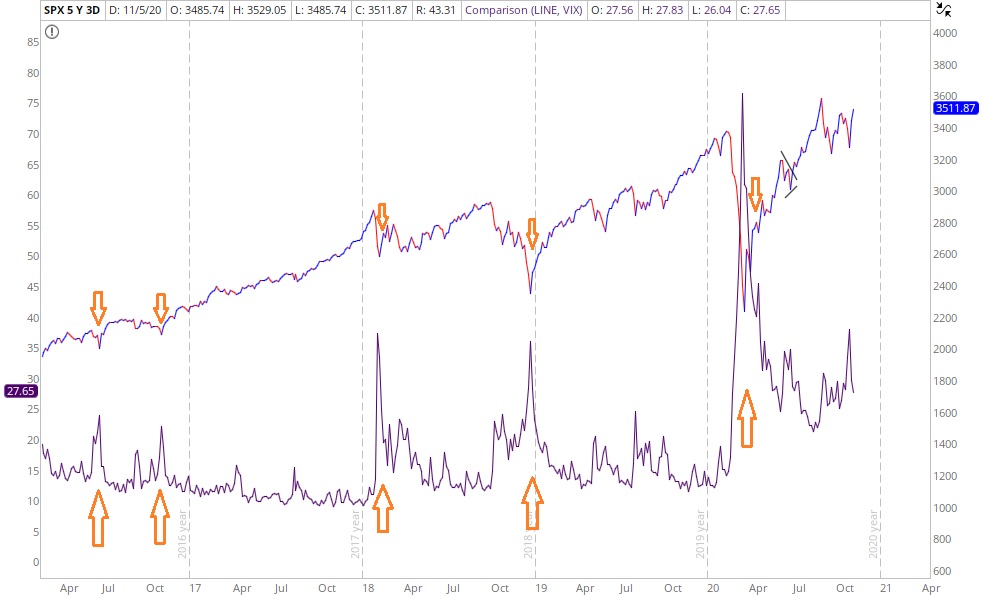

In the chart below you’ll see this strong negative correlation between the SPX (red & blue line) and the VIX (purple line).

VIX VVS Trade Setup

As you look at the range of the VIX since the sell-off in February and March, the VIX hasn’t really gotten any traction below 24%. The index traded for several weeks below that level in August but never closed below 21. This is significant since support and resistance levels can become significant for the VIX.

Yesterday, Don walked through a trade that intends to capitalize on the price holding support and rising in the coming months. Here’s the details of the VVS trade:

- Buy 20 JAN 21 $45 Call

- Sell 20 JAN 21 $70 Call

- Sell 20 JAN 21 $22 Put

- Buy 20 JAN 21 $17 Put

This trade incorporates four different strike prices and so should only be done on the most liquid of products. It also incorporates selling a put vertical to buy a call vertical. This trade was made this morning for a $0.05 credit.

This trade can be done for a credit even with uneven distances between the put and call strikes because of the positive vol skew of the VIX options.

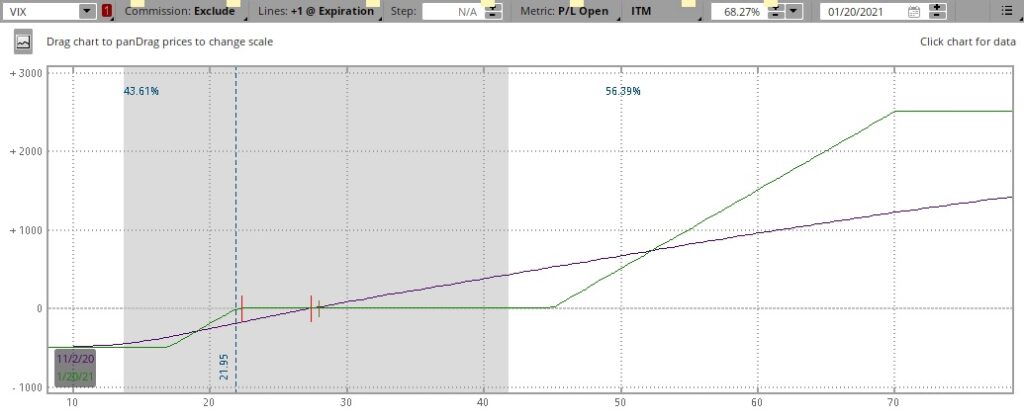

VIX VVS Risk Profile

As you’ll see in the VIX risk profile chart below, the max loss is achieved if the price closes below 17 at $495 per contract. It makes $5 per contract if the VIX closes at expiration between 22 and 45. The trade has a maximum gain of $2505 per contract if the VIX closes above 70 at expiration.

The VVS has a high probability of making money with the small credit, but has huge upside if things get unwieldy in the market. With a credit and only a margin requirement for the short vertical risk, this trade can be an efficient way to add negative delta as the market is falling. This creates a cheap hedge.

Conclusion

Whether you’re long the market or want a high probability approach to make money if the VIX rises sharply, the VIX Volatility Spread (VVS) may be your trade. Currently, we have two separate 3-hour classes on the setup and management this trade for our subscribers.

If you have interest in other hedging strategies her are links to recent posts on the Atomic Hedge, and using options and futures. As you probably guessed, we have 3-hour classes on these topics as well that outline the setup and management.

Wondering when to hedge? See how unlocking the Vomma Zone can help you better understand when volatility is about to rise.

Not a subscriber? Become a TheoTrade member.

1 Comment

Paul HILL

November 7, 2020Please help me on the VIX 20 Jan 21 Vol spread where BP will be reduced by $494 and held by the broker.

If for example Vix is between 22 and 45 at or soon before expiration the profile chart says there will be a $5 profit. In that case would the broker refund that $495 as well as the $5 ?