This is yet another one of those days where everything can pretty much be explained in one chart. Here it is:

Bank of England governor Mark Carney gave his second speech since the Brexit vote on Thursday and all but assured the market that more BoE easing is in the cards. “The economic outlook has deteriorated and some monetary policy easing will likely be needed over the summer,” Carney said. Needless to say, that sent the pound a plungin’, UK stocks soaring, Gilts rising, and likely gave US stocks the excuse they needed to continue what, as of Thursday morning, has turned into a colossal three-day rally.

Notably, UK stocks are actually back to pre-Brexit levels!

But wait, there’s more. Believe it or not, after today’s Carney-inspired 2.3% move to the upside, the FTSE is now at its highest level since before China devalued the yuan while the pound is plumping depths not seen in… well, not seen in a long, long time.

Here’s a sample of some of the chatter via Bloomberg:

-

GBP/USD reverses earlier gains, dropping 138 pips to 1.3295 day low within 3 minutes

-

Algo names sold upon the headline in size, trader in London says

-

Short sterling strip rallies 4-6 ticks, led by whites

-

GBP OIS markets price 98% chance of a 25bps rate cut in Aug.

-

OIS pricing 57% chance of 25bp ease to 0.25% for July 14 meeting vs 34% yesterday;

-

Prices chance of 50bps of cuts, 22%, beginning Aug., 39% chance of 50bps or more easing by yearend

-

Now pricing small chance, 1.4%, of negative rates beginning in Sept., 8.4% chance by year-end

So there you go folks. Central banks to the rescue. Again. At least they haven’t lost their ability to move markets in the short-term.

Note also that this is precisely what we said here on Wednesday. To wit: “It’s starting to look like we’re reverting back to the old ‘bad news is good news’ dynamic vis-a-vis markets and central banks. That is, the Brexit plunge pretty much guarantees further stimulus.”

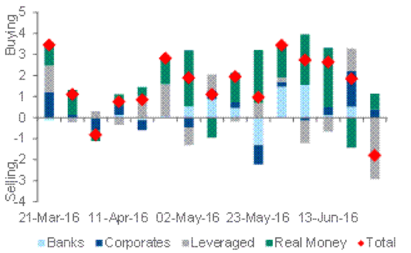

Here’s something to consider on the pound from Citi:

“We saw aggressive GBP selling by leveraged/hedge funds on last Friday and Monday (enough to trigger our cut off on flows), but this wasn't followed through by Real Money or other clients. Real Money actually turned out to be a GBP buyer last Friday (we assume the GBP move triggered rebalancing of sorts) and only a mild GBP seller on Monday.

“It is too early to call how the long-term capital will behave, but we suspect there will be more selling to come. Real Money has been net-GBP buyers since March, but the referendum shifts significantly the growth and investment outlook. With the UK still holding large twin deficits (and unlikely to find enough inflows to balance them), it unlikely this client type is comfortable with the level of exposure or the exchange rate.”

The bank’s conclusion: “BoE cut & Brexit should do it” in terms of triggering real money selling.

Of course through it all, Carney was careful to stick to what has become the universal central bank scapegoat: fiscal policy (i.e. inept lawmakers). “Monetary policy cannot fully offset the economic implications of a large negative shock,” he said. “The future potential of this economy and its implication for jobs, wages and wealth are not the gifts of monetary policy makers. These will be driven by much bigger decisions; by bigger plans that are being formulated by others.”

Apparently someone forgot to tell Carney that now might not be the best time to remind the British electorate that politicians are often bad at their jobs.