Ask analysts about crude’s rather dramatic rebound off of the January lows to nearly $50 and you’ll probably get a variety of answers referencing any number of data points that purportedly signal a shift in the supply/demand picture.

Barclays, for instance, sees the market swinging to a supply deficit in 2017.

But the reality heading into next month’s OPEC meeting is that the fundamental backdrop is decidedly bearish. We got a reality check to that effect on Sunday when Rokneddin Javadi (Iran’s Deputy Oil Minister) told reporters the country had no plans to join any kind of negotiated production freeze.

"Under the present circumstances, the government and the Oil Ministry have not issued any policy or plan to the National Iranian Oil Company (NIOC) towards halting the increase in the production and exports of oil," Javadi told the Iranian media. "Currently, Iran's crude oil exports, excluding gas condensates, have reached 2 million barrels per day [and will] reach 2.2 million barrels by the middle of summer,” he added.

As a reminder, there’s been on-again, off-again talk this year around whether the Iranians would be willing to turn off the spigots once production ramped to pre-sanction levels. The Saudis surprised the market in April when Deputy Crown Prince Mohammed bin Salman effectively pulled rank on long-time market heavyweight Ali al-Naimi in refusing to participate in any kind of production freeze unless Tehran agreed to participate as well. Effectively, the oil market has become yet another theatre for Saudi Arabia and Iran to wage their eternal sectarian feud.

Still, prices rallied as everyone appeared to think that from $27 per barrel, the only place to go was up. Now, the market finds itself in a rather precarious position: prices have rallied to $48 and there looks to be a perfect storm brewing. The Fed surprised the market last week by conveying an overwhelmingly hawkish message and on the supply front, there’s so much oil that floating storage is rising even as the arb makes it unprofitable. Here’s Morgan Stanley:

“Floating storage continues to grow despite outages and poor economics. According to Reuters reports, at least 40 supertankers laden with crude are anchored offshore Singapore as floating storage. In fact, according to Reuters, the volume stored offshore Singapore is up 10% WoW despite outages, to 47.7 mmb. The increase in floating oil comes despite disruptions in the Atlantic Basin and an out-of-the-money floating storage arb, suggesting markets are not as healthy as sentiment suggests. It also highlights the speculative nature of much of the oil bounce this year (recent disruptions aside).”

Speculative indeed. And the commentary gets still more bearish from there. Here’s another excerpt:

“Unprofitable storage arbs hide a growing debt-fueled offshore trade as traders search for places to store oil. We estimate the Brent 1M floating storage arb is -$0.48/bbl while 12M is -$6.11/bbl, implying no incentive to store oil on ships. Yet, banks are seeing a sharp uptick in interest to finance storage charters. This storage is not happening for profit. Rather, the market is looking for places to store oil. To profit, traders need to hope for oil prices to rise enough to pay for the new debt incurred for this storage.”

In other words: they’re knowingly implementing the floating storage play at a loss because there’s nowhere else to put the oil. There’s nothing bullish about that.

"Upward price momentum appears to be slowing as we feel that this late winter/spring bull move is in a very advanced stage with only about $3 to $4 a barrel remaining on the upside in referencing either WTI or Brent futures," Ritterbusch & Associates’ Jim Ritterbusch told Reuters on Monday.

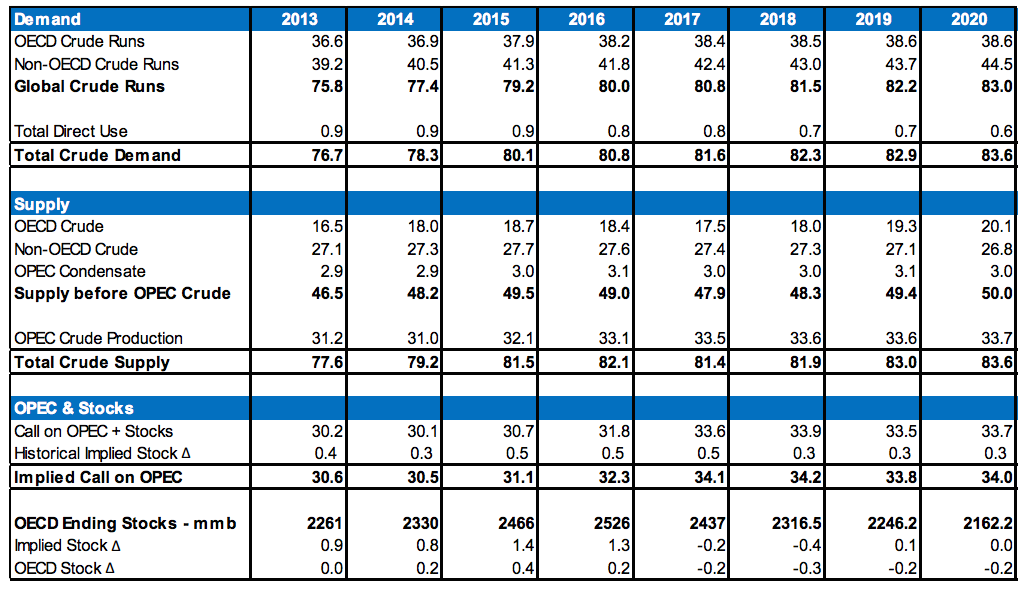

Apparently, it’s finally hitting home that Canadian wildfires and turmoil in Nigeria and Libya won’t be enough to balance this market. Here’s Morgan Stanley’s supply/demand outlook:

Meanwhile, Deutsche Bank is out with a fresh look at just how overextended this rally has become given the likelihood that the dollar moves higher on a hawkish Fed.

It’s difficult to see how crude moves much higher from here in the short- or medium-term, especially considering the outlook for the USD.

Of course the market can stay irrational longer than you can stay solvent, and when things have gotten so out of whack that the floating storage play is being put on at a loss, you have to wonder whether this is one of those times where you should just grab the popcorn and enjoy the show rather than try to guess where thing go next.