S&P 500 Ends Its Winning Streak

S&P 500 ended its winning streak by nearly the slimmest of margins as it fell just 4 basis points on Wednesday. Only thing this does is end the winning streak. That’s one less argument the bears have that stocks are overbought. They still are overbought though.

CNN fear and greed index actually increased 2 points to 87 which is well into extreme greed territory. It’s interesting that the index was up since the VIX was up 0.29 to 12.58. This VIX has been up 2 days in a row. Some investors get skittish when the stock market is overbought. And the VIX increases without significant declines in the market.

If a pullback does occur, I will be slightly more optimistic on 2020’s returns. However, stocks usually don’t fall near Christmas. I don’t see a catalyst to send stocks lower since the Fed is done meeting for the year and phase 1 of the trade deal is done.

Some are calling the deal merely a truce. Normally I agree with that notion. But trade still is not a negative catalyst. That is, unless talks break down or China is found to have not been buying enough American agricultural products which would cause America to raise tariffs again.

Stocks Ignore Impeachment & Biden Leads The Primary Ahead Of The Debate

We saw stocks completely ignore the Trump impeachment which isn’t a shock. It's highly unlikely President Trump will be removed from office with the GOP controlling the Senate. I’d argue a single poll on either the Democratic primary or the general election matters more to stocks than the impeachment. Which is why I cover the former more than the latter.

A betting market shows there is a only 9% chance of Trump being removed from office. That’s down from 23% on October 22nd. Odds fell because no Republicans in the House voted to impeach him.

There were 3 primary national polls released on Wednesday. Biden was ahead of Sanders by 7, 10, and 16 points. Let’s see if Thursday’s debate shakes up the race. Sanders has had modest momentum, Warren has been floundering, Buttigieg has lost momentum, and Biden is just hanging on to his lead.

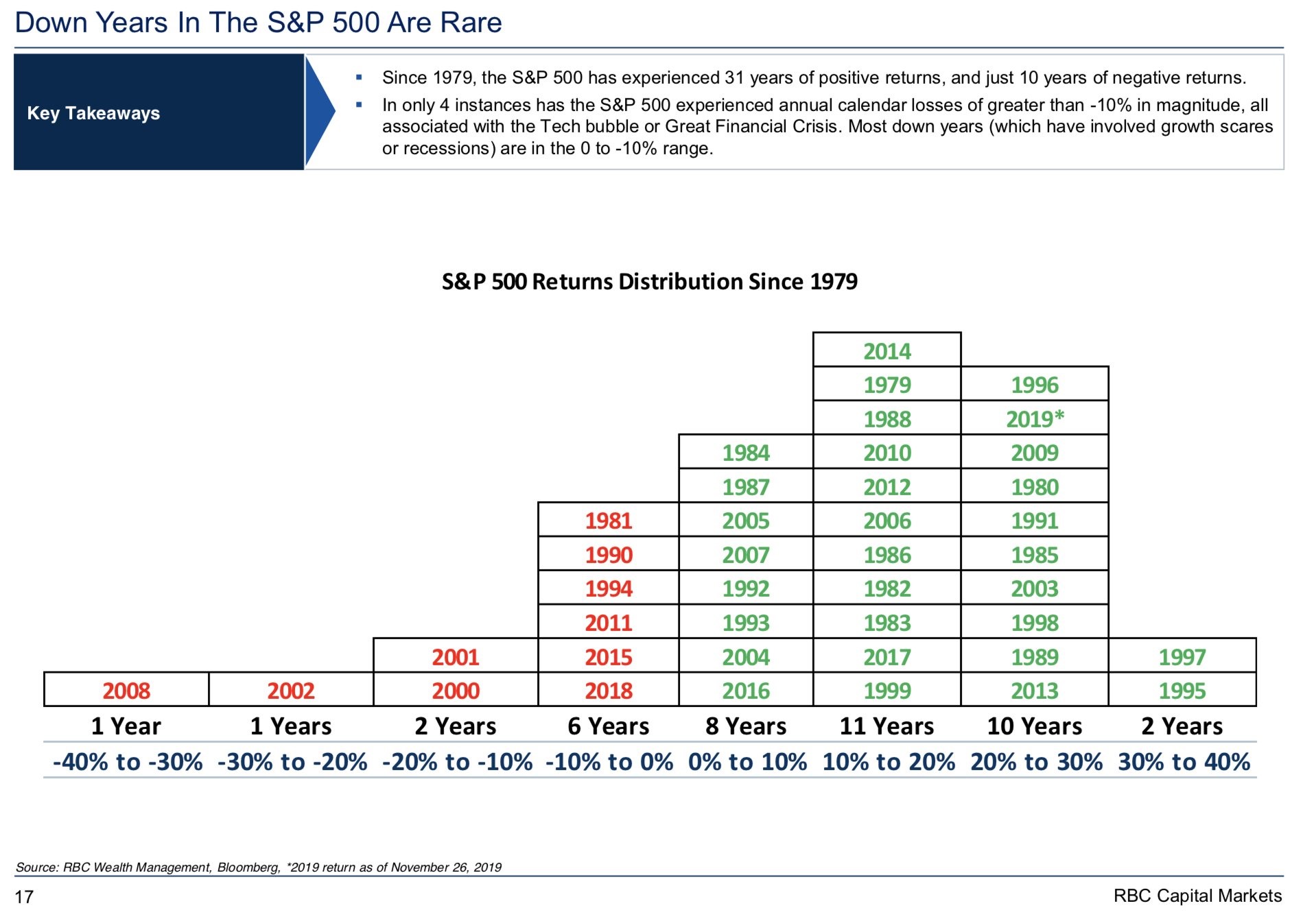

Down Years Are Rare

It’s common to hear people in finance tell non-finance people how rare this year has been. That’s great advice because if you’re saving money, you don’t want to rely on high returns to meet your goals. It’s best to assume slightly lower than average returns, so you’re safe no matter what.

Assuming 6% annual gains isn’t a bad idea. If you need 27% gains per year to meet your goals, you won’t reach them unless you start aggressively investing on your own or find a very talented fund manager.

With that being said, you might be surprised to find out that gains of 20% or more have actually been more common than down years since 1979. There have been 10 years where the S&P 500 gave investors returns of 20% to 30%.

In 2 years the market was up 30% to 40%. There were only 10 years where the market fell. It only fell 20% or more twice. Worst 4 years since 1979 were all in the last decade which is why it had the worst Sharpe ratio ever. This decade was very strong, but it only had 2 of the best 12 years.

This contextualizes why I’m calling for below average gains rather than a decline. The stock market is expensive and the election might be a negative catalyst for stocks. However, I see positive earnings growth and a Fed that won’t be cutting rates. Negative factors aren’t strong enough to make me think stocks will fall. Although, I wouldn’t be surprised if stocks are down for a lot of the year.

Review Of Wednesday’s Action In Markets

Nasdaq was up 5 basis points and the Russell 2000 was up 0.25%. Russell 2000 has been on a strong run in the past few days. It’s rallying along with the steepening of the yield curve because it has a high weighting of financials.

Since October 8th, the index is up 12.8%. It’s up 3.7% since December 3rd. It’s only down 4.5% from its record high in August 2018. If all it takes is the yield curve steepening for the index to rally, it will make a new record high in Q1 2020.

My best long idea for 2019 was the KBW regional bank index which is up 23.96%. That’s a great return, but it’s below the S&P 500’s return. My best short idea was a massive mistake as Yeti stock is up 110.58%. Luckily, I mentioned taking that short off early in the year.

Interesting, the financials actually fell 0.48% on Wednesday. Though the small banks have driven the Russell 2000 higher recently and the financials have helped the S&P 500, that wasn’t the case on Wednesday. Worst sector was the industrials which fell 0.5%.

Best sectors were the utilities and real estate which rose 0.44% and 1.33%. The 10 year yield has recently been increasing as it’s now at 1.91%. It still can’t get above 1.94%. I think it will in the next few weeks. I’ll get into my 2020 predictions next week. But it’s safe to say I think the 10 year yield will move higher in 2020. Yields should rise because the economy is recovering. Specifically, nominal GDP growth will improve soon.

2 year yield is at 1.62% which puts it 29 basis points below the 10 year yield. In the past 3 weeks, the curve has steepened quickly. As you can see from the chart above, the 10 year yield was only 14 basis points above the 2 year yield at the end of November.

Difference between the two yields is about to be the highest since November 2018 if it gets to 31 basis points. Any inversion was very brief. It only lasted 3 days. We were waiting for an inversion for years. That was very anticlimactic!

Fed’s decisions in 2020 will likely be anticlimactic as well since there is only a 45.9% chance of a rate cut. As I’ve been saying for over a month, there won’t be any movement in the Fed funds rate next year.