Worst Week - Another Down Day For Stocks

Suddenly in the Worst Week of 2019, stocks are in a losing streak as the S&P 500 fell again on Friday. It’s now down 5 straight days since it reached its record high on July 26th. It is down 3.1% in this losing streak.

This decline is mostly related to President Trump’s tariff announcement on Thursday. A 3.1% decline in the S&P 500 and 3.9% decline in the Nasdaq made this the worst week of 2019 for both indexes.

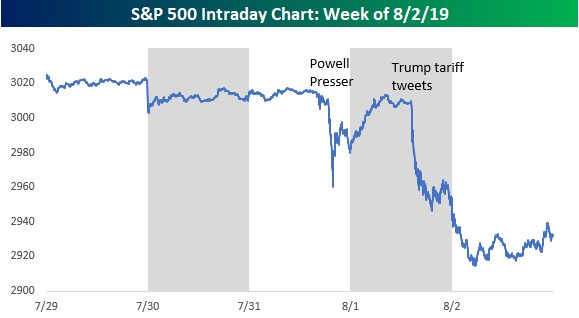

The chart below shows the intraday action. There was volatility related to the Fed meeting, but stocks regained those losses on Thursday morning. President Trump’s tariff tweets quickly reversed Thursday’s gains. It’s almost as if the rate cut gave Trump the confidence to issue new tariffs.

He is highly motivated to make a deal in the next few months as he gears up for his 2020 re-election bid.

Specifics On Friday’s Action

Worst Week - The stock market may have sold off on Friday because of trade tensions. And not due to the BLS labor report. BLS labor report came in as expected.

On Friday S&P 500 fell 0.73%, Nasdaq fell 1.32%, and Russell 2000 fell 1.10%. Even though stocks were down sharply, the VIX actually fell 1.46% to 17.61. You sometimes see the VIX fall on down days if the VIX starts out elevated and stocks fall slightly. However, that wasn’t the case on Friday making this an odd movement.

CNN fear and greed index fell 7 points to 36 which means it is near extreme fear.

Worst Week - There certainly is no short of pundits calling for a recession.

While the global economy is in a manufacturing recession, China is weakening. And the American manufacturing sector is near contraction, I’m not willing to call for a recession in America yet. The only part of the CNN index that’s in the greed category or higher is the net new 52 week highs and lows on the NYSE It is showing extreme greed.

Decline in the VIX prevented the CNN index from falling further as the volatility category is neutral.

The exact sectors you’d expect to rally on a ‘risk off’ day did. Utilities, real estate, and consumer staples were up 0.05%, 0.76%, and 0.12%. Energy and tech were the biggest losers as they fell 1.35% and 1.68%.

Tech is hurt the most by the tariffs. Last quarter Apple saw an improvement in its Chinese sales growth. Now with these new tariffs, Apple might take another step back. Apple stock is down 4.23% in the past 3 days after spiking on its solid earnings announcement.

Semiconductor industry has been cratering in the past couple weeks. It hit an all-time high on July 24th after rallying 25.67% in less than 2 months. Since then it is down 8.22%.

New Trade Deal With EU

Worst Week - Many times, President Trump has simultaneously issued new tariffs while making strides in trade negations with other countries. His goal might be to strengthen America’s position versus the nation he is taxing.

The President announced the Chinese tariff on Thursday. Then on Friday he announced a deal with the EU that lowers trade barriers in Europe and expands market access for American farmers and ranchers.

Office of the U.S. Trade Representative stated this deal will increase U.S. beef exports to Europe from $150 million to $420 million. President Trump joked about taxing European autos at a 25% rate. That would be the most devastating tariff levied under his administration. It’s good to see that’s not a high risk.

Worst Week - Yet Another Big Rally In Treasuries

The treasury market loves the new tariffs because it increases the odds of rate cuts and an economic slowdown. 10 year yield fell 5 basis points on Friday to 1.85%. People who claim the stock market is overheated are missing the elephant in the room as that is the government bond market. I’m not saying the 10 year yield will increase soon. I’m just commenting on its remarkable run.

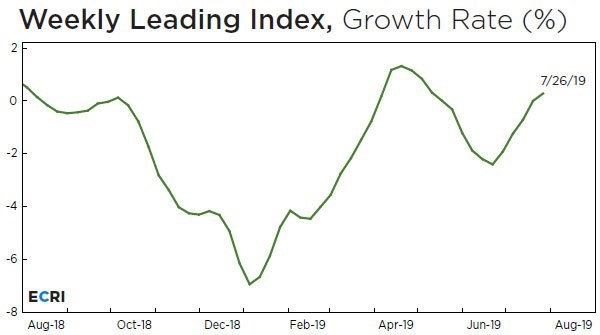

Based on the ECRI leading index’s improvement, I see nominal yearly GDP growth starting to improve in Q4. That means the 10 year yield might stop declining. We need to see more economic improvement and more growth in the ECRI leading index before shorting the long bond.

As you can see from the chart below, the leading index’s growth rate in the week of July 26th improved from 0% to 0.3%. That’s not exactly a huge vote of confidence that the economy will be strong in the first half of 2020. Yearly growth should be very strong just because of the easier comps.

Investors expect this index to show weakness in the next reading because of the decline in stocks this past week.

2 year yield fell 2 basis points to 1.71% which means the difference between it and the 10 year yield fell 3 basis points to 14 basis points. If investors continue to get more bearish on the economy, the curve will invert.

There isn’t much room for the 2 year yield to fall as the Fed is saying it isn’t starting another cut cycle. Ironically, if there is a recession and the Fed is forced to cut rates more, the curve may not invert.

Worst Week - Fed Expected To Cut In September

There is now a 100% chance the Fed will cut rates in September which is a huge reversal from where it was right after the Wednesday Fed meeting.

Fed would wreak havoc on markets if guides for no cut in September. The yield curve would invert. And the stock market would fall at least another 5% in short order.

With that in mind, James Bullard is speaking on Tuesday. That should be very interesting. He’s a dove, so he shouldn’t spook the market. However, he did clarify Clarida’s dovish statement before the July meeting, stating there would only be one cut.

Many pundits are saying the Fed should have cut rates 50 basis points in July because stocks fell. However, the 25 basis point cut would have been enough for markets if it wasn’t for Trump’s tariff announcement on Thursday.