Weak Retail Sales

November retail sales report was weak. This goes against the strong consumer sentiment index and the solid real wage growth. It also goes atainst the Gallup poll that asked how much consumers would spend. Finally, it contradicts Costco’s great same store sales growth, and the low unemployment rate.

Personally, I think this weakness occurred because of the late Thanksgiving which pushed Cyber Monday to December. This report is seasonally adjusted, but that doesn’t make it perfect. Since Cyber Monday is becoming more important with the growth in online sales as a percentage of all retail, the adjustment could have been wrong.

Unfortunately, we need to wait for the December report to determine the impact of the late Thanksgiving. That will give us a revision to the November report and show if December sales growth was helped by the late Thanksgiving.

Because of the easy comp, December sales growth will spike no matter what. That will make it tougher to see the impact. That’s potentially 2 reasons for retail sales growth to be very strong. Therefore, expectations for the report are high.

Specifics Of The Weak Report

Headline monthly retail sales growth was 0.2% which missed estimates for 0.5% and the low end of the estimate range which was 0.3%. October report was revised up one tick to 0.4%. Across the board, the data missed the low end of the expected range. At least, the October readings were pushed higher.

Monthly growth without autos was 0.1% which missed estimates for 0.4%. It missed the low end of the expected range by a tick. October reading was revised up 0.1% to 0.3%. Excluding autos and gas sales growth was 0% which missed estimates for 0.4% and the low end of the consensus range by two ticks.

Revision was up 1 tick again as growth was 0.2% in October. Yearly gas prices faced much easier comps as was shown in the CPI report. Finally, monthly control group sales growth fell from 0.3% to 0.1% which missed estimates for 0.4% and the low end of the estimate range by a tick.

Since headline inflation increased because of energy prices and this was a weak retail sales report, if you ignore the timing of Thanksgiving, it’s no surprise yearly real retail sales growth fell. It fell from 1.45% to 1.28% which was the weakest reading since May. In the last slowdown, growth troughed at 0.81% and in this slowdown growth troughed at -0.53% last December. Many were expecting growth to improve, so this was a big disappointment if the reading is accurate.

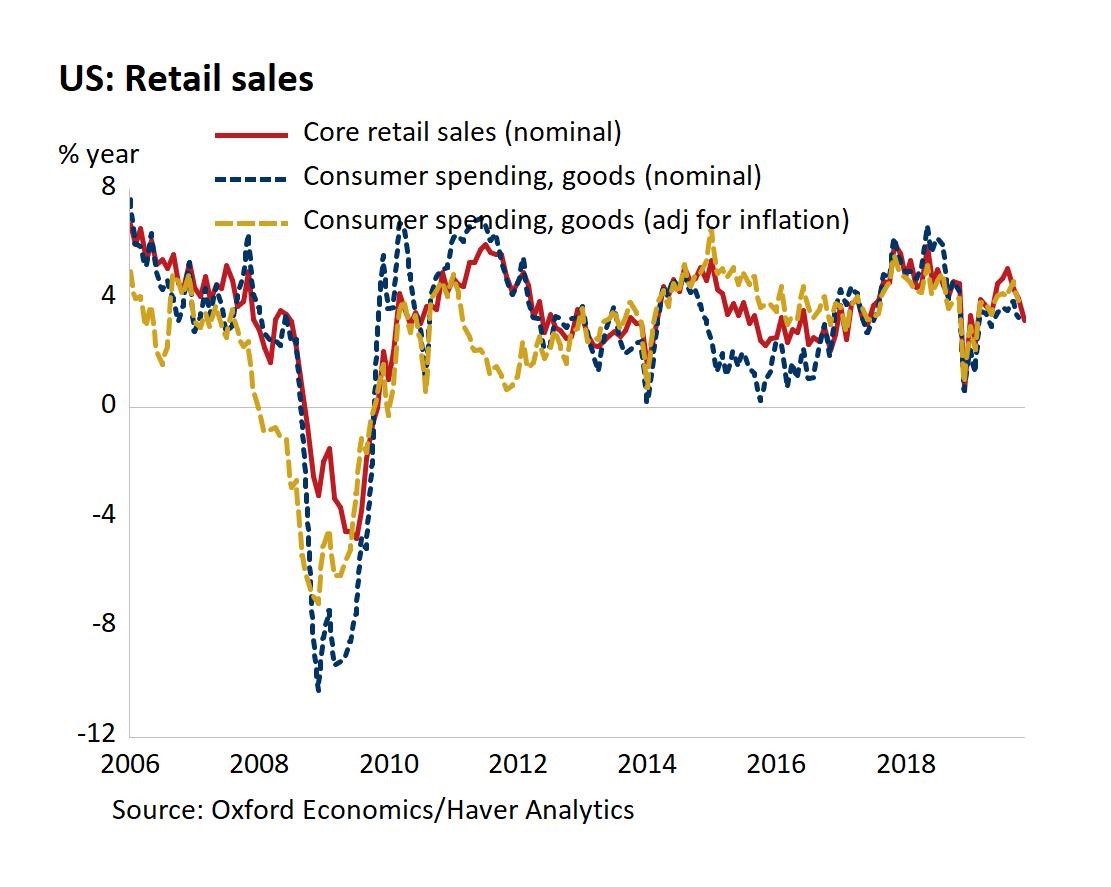

You can see in the chart below that retail sales, real retail sales, and core sales growth were all weak. Yearly nominal retail sales and retail sales excluding food services growth improved very slightly, but their 2 year growth stacks fell. Overall retail sales growth increased from 3.2% to 3.3%, but the comp got easier by 0.7%. Excluding food services growth went from 3% to 3.1%, but the comp was 0.5% easier.

Yearly Online Sales Growth Fell?!?

Yearly control group sales growth fell from 3.99% to 3.17%. Unlike what was expected based on the motor vehicle sales report, motor vehicle and parts yearly growth fell slightly. It went from 5.19% to 4.88%. As expected, sales growth at gas stations improved because the comp got much easier.

Yearly growth went from -4.3% to 0.54%. If this report was weakened by Cyber Monday being in December instead of November, you’d expect yearly online sales growth to fall significantly. That’s what occurred.

Based on the Adobe Analytics data, I was expecting yearly online sales growth to increase, but it fell significantly. That doesn’t make sense to me. Obviously, I could be wrong; this data might have been perfectly adjusted for the seasonal change. To me, it seems wrong.

Specifically, monthly growth fell from 1.4% to 0.82% and yearly growth fell from 13.69% to 11.5%. If online sales growth was +14%, this would have been a very good report. Yearly restaurant sales growth was fine as it increased 1 basis point to 5.07%. But general merchandise sales growth fell from 0.36% to -0.13%. And I was expecting general merchandise sales growth to be weak because sales growth on Thanksgiving and Black Friday combined was negative.

Updates GDP Forecasts

Obviously, this retail sales report put a damper on GDP growth estimates since expectations were for the consumer to combat weak business investment growth. However, even though this report missed estimates, the declines in Q4 growth estimates weren’t that large. Oxford Economics lowered its estimate for PCE growth by 0.2%.

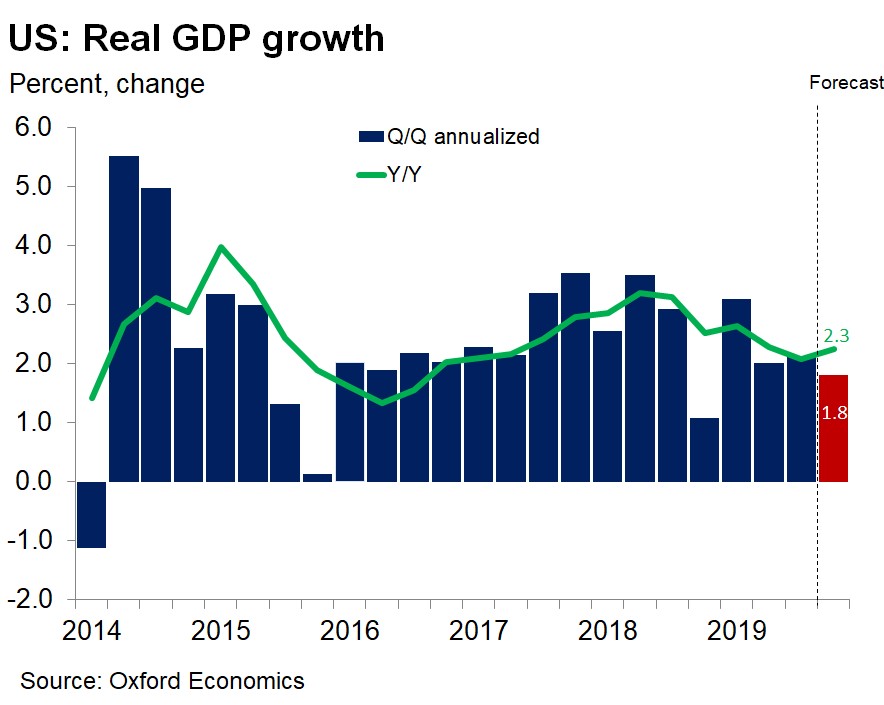

As you can see from the chart below, it lowered its GDP growth estimate one tenth to 1.8%. Yearly growth is expected to increase to 2.3%.

Goldman Sachs lowered its Q4 estimate one tick to 1.8% as well. Atlanta Fed Nowcast was unchanged at 2% from December 13th because the decline in the real PCE growth estimate was offset by the increases in the estimates for real government spending growth, real private inventory investment, and real net exports.

St. Louis Fed nowcast is 2.04%. It’s not great for the most optimistic estimate to be just over 2%. NY Fed Nowcast increased 0.11% to 0.69%. Retail sales report helped it. That just shows how negative the implied estimates were. Q1 estimate increased to 0.82% from 0.66%. That’s still very weak as the Fed sees long term growth being 1.9%.

Conclusion

November retail sales report was weak even though nominal yearly growth improved slightly. Personally, I think the report was hampered by the late Thanksgiving, but we shall see. Estimates for real Q4 PCE growth only fell modestly since they weren’t that enthusiastic to begin with. That pushed Q4 GDP growth estimates slightly lower.

Since I see either the November report being revised higher or the December report accelerating significantly, I’m more optimistic on real Q4 consumption and GDP growth. And I see real growth coming in near 2% which is above 2 of the 3 nowcasts and the median estimate on Wall Street which is 1.8%.