Jobless Claims Rise Slightly

Headlines at the stock market’s open said stocks were falling on a bad jobless claims report. After the stock market rallied, they needed to change their headlines. Given the recent decline in stocks, it's doubtful that this weak reading was enough to cause a decline.

Then again, stocks can move for any reason in the near term. It’s tough to make sense of week to week moves. That being said, the people who thought the rally in late March and early April was just noise missed out on one of the greatest gains in market history.

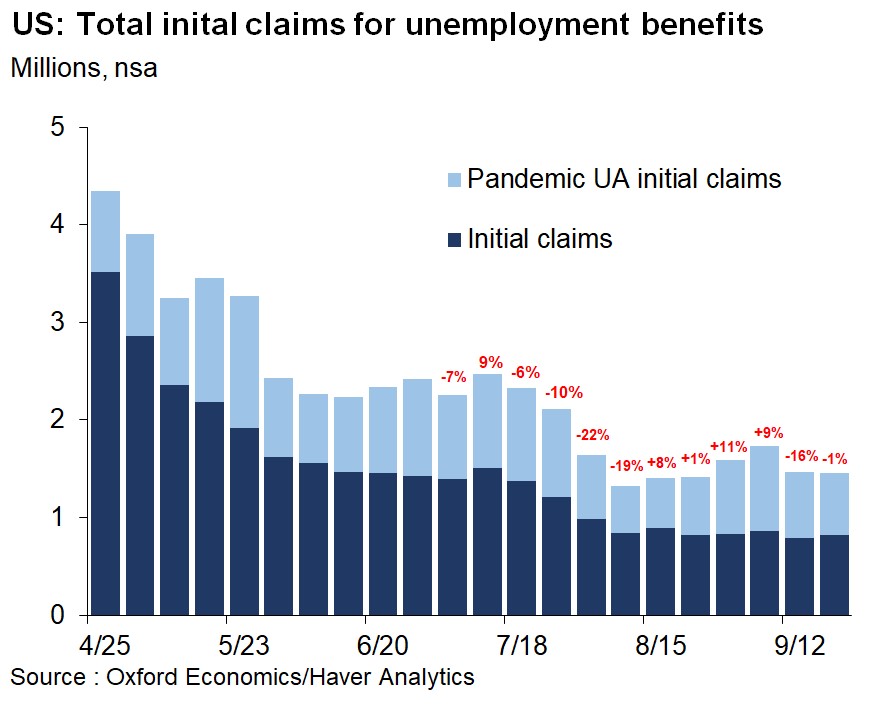

Specifically, there were 870,000 seasonally adjusted claims in the week of September 19th which was up 4,000 from the prior week. That actually was 10,000 below expectations. This is seasonally a weak time for the labor market which is why non-seasonally adjusted claims were up from 796,000 to 825,000 which is still below where they were 2 weeks ago.

It seems like initial claims are plateauing which makes sense because a lot of the labor market that can survive in this new environment has already recovered. Parts like leisure and hospitality that are doing badly, won’t suddenly start bringing workers back until COVID-19 is at bay.

As you can see from the chart above, NSA initial claims and PUAs actually fell 1% because of the decline in PUAs. PUAs were down 45,000 to 630,000. That’s the lowest total in 4 weeks. PUAs in California have normalized as the fraud and data issues are being rectified.

On the other hand, Arizona’s data makes no sense as there were 204,499 initial PUA claims. That’s about 1/3rd of the total even though Arizona is a small state. Good news is continued claims fell from 12.747 million to 12.58 million. That was the BLS’s survey week.

Details Of The Claims Report

If you’re just looking at continued claims from the past 2 months, claims from survey week to survey week fell 2.9 million in August and 1.6 million in September, signaling a slowdown in job creation which is to be expected. It’s impossible for there to be over 1 million jobs created each month indefinitely.

High frequency data suggests there will be 600,000 jobs created in September which is solid. We’re still waiting for a COVID-19 treatment to save the leisure and hospitality sector, bringing millions of jobs back in that industry.

Next 2 weeks of jobless claims need to have a massive asterisk next to them because California is not accepting claims to improve its process. This is a dreadful idea. Only good thing is that at least we are far from the worst of the recession. At the worst of the pandemic, there were many issues in other states such as Florida which was a complete disaster.

There were people waiting outside in crowds to submit claims when it was strongly advised that large gatherings shouldn’t occur. This could have a minor impact on national spending. If you own a company that’s mainly in California and sells to middle income people, it’ll probably see an impact.

A potential upcoming problem is people running out of benefits because their 26 weeks are exhausted. Continued claims are definitely going to fall. But that obviously should be taken lightly because of the people running out of benefits. This is unlike any other recession because almost all the job losses happened in a few weeks.

As you can see from the chart above, 895,000 claims exhausted their benefits in August. That number will explode in September and October. Claims are going to shift to pandemic programs and state extended benefits which is important because people still need the money to survive. You can’t just ignore these people and say the labor market is back to normal when millions leave continued claims in October.

PUA and PEUC claims expire in December. At least that gives the economy a little more time to get back to normal. Since there will be so much data on vaccines and treatments released in October, we could be looking at a much improved labor market by the end of the fall as businesses anticipate a return to normalcy.

If you’re a business that hears a vaccine was effective and will be fast tracked so people get it by March, you might want to start looking for candidates in November and December. On the other hand, firms might not have the cash to hire people until demand picks up.

COVID-19 Testing Spikes Strongly

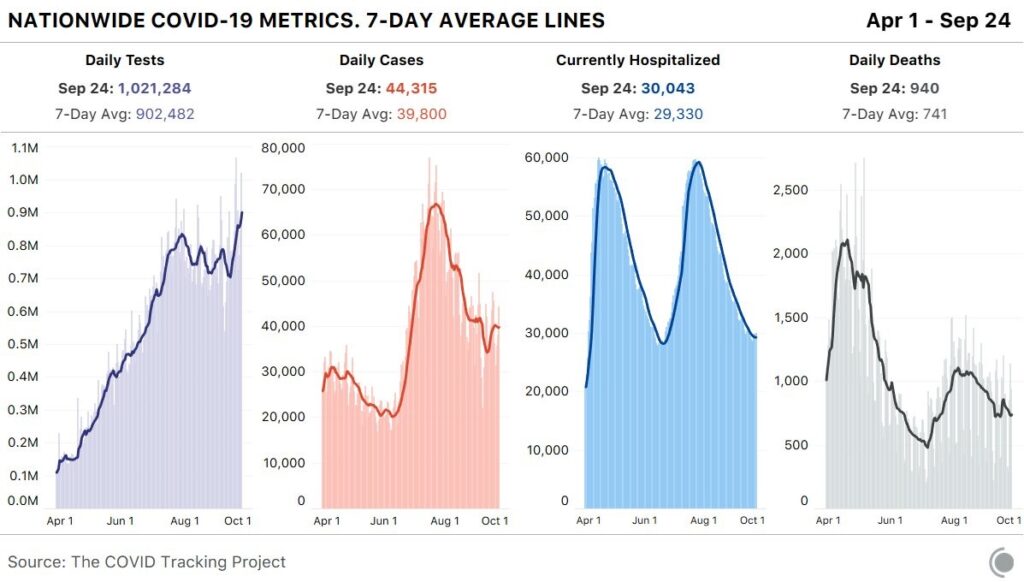

Data on COVID-19 was a mixed bag. Best part of it was the spike in testing likely because of antigen testing (the Abbott test). As you can see from the chart below, there were 1.02 million tests which was the 2nd most ever and above the 7 day average of 902,000.

Interestingly, the 7 day average of tests has increased sharply in the past few days, while new cases have fallen slightly which means the positive rate fell. Positive rate is about 5% which is near the low since we first started testing.

On the negative side, there were 940 deaths which is above the 7 day average of 741. You can see we have gotten back to where we were when deaths artificially fell because of Labor Day. This decline is more sustainable. Further bad news, hospitalizations have moderately increased recently.

You can see the rate of decline in the 7 day average has fallen as if it is bottoming. That makes sense because cases increased moderately earlier in September. That increase was related to Labor Day data leaving the moving average and the spike in testing. Therefore, it's unlikely that we will see much of an increase in hospitalizations. It will stabilize though.

It’s notable that as testing increases, we will get more positive tests from asymptomatic people which means deaths and hospitalizations won’t increase following increases in cases. The only way to end the spread is to quarantine asymptomatic people who test positive.