When Will COVID-19 Disruption End?

Friday had yet another record number of COVID-19 cases, but we are on the precipice of strong improvement by the end of July. Specifically, there were 74,987 new cases which is obviously terrible. There were 946 new deaths which pushed the 7 day average up from 761 to 775.

Good news is it isn’t spiking, but the bad news is it could still increase for the next 4 weeks. It might even get to 1,000 per day just on legacy cases (meaning the cases that have already been diagnosed).

Friday seemed like a terrible day for Arizona because there were 3,910 new cases, but it wasn’t because there are always spikes on Friday. Cases rose 2.9%, but they rose 3.7% the previous Friday. This is actually the 4th consecutive decline in growth on Friday. 7 day average fell to 3,090 which is the lowest since June 30th.

Further good news is there were only 682 hospitalizations in Orange County, California and 235 new ICU patients. There were 722 hospitalizations 2 days ago and 245 ICU patients yesterday. Bar and indoor restaurant closures on July 2nd are working which shouldn’t shock anyone.

Restrictions in the hotspots will cause more declines in the next 1-2 weeks. National headlines of record cases make this situation look worse than it is, just like how the national numbers looked better than the underlying trends about 3-4 weeks ago.

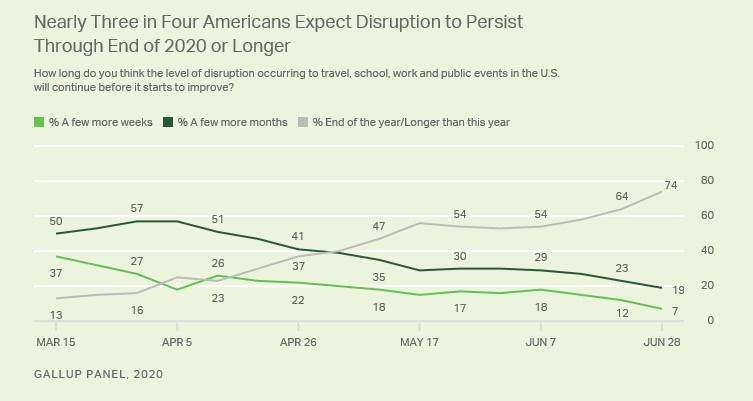

Restrictions will likely be lifted in August and September and national deaths will have a 2nd peak in August. New York is still continuing with its reopening plans as it still isn’t fully back to normal. The chart above shows the opinions Americans have had on the COVID-19 disruption since March 15th.

As you can see, Americans have gotten more pessimistic on the prospects of a quick return to normalcy. As of June 28th, only 7% said the level of disruption occurring in travel, school, work, and public events will end in a few weeks.

They would be even more pessimistic if they were asked today because the situation has gotten worse. 74% said they think the economic disruption will last until the end of this year or longer than this year. Americans are too pessimistic. New York was one of the earliest to be hit by the virus and it experienced by far the most deaths. Conditions have already started to improve there.

Economic conditions will get worse before they get better in the most recent hotspots. It won’t be completely back to normal by the end of the year, but there will be progress starting in August as new cases fall. We're more concerned with the Midwest than these hotspots because we need to see openings without cases spiking. We already know cases will fall in the hotspots because they are taking measures that have worked in other areas.

Consumer Spending Is Stuck In The Mud

Investors are starting to look past this virus. They believe a stimulus is coming and the hotspots will get the cases under control in the next couple weeks. From July 9th, the Russell 2000 small cap value index is up 7.6% which signals cyclical optimism. You can argue this is just an oversold rally. Only time will tell.

As you can see from the chart above, debit and credit card spending data shows growth has tapered off in the past few weeks. It’s dramatically different from the growth in retail sales which didn’t account for the weakness in the 2nd half of June. Investors measure uncertainty.

In March, we had no idea what the implications of COVID-19 would be. Now we know how the virus reacts to precautions and how consumers react to extra stimulus.

As long as the people in the south and west wear masks and social distance and the government passes another stimulus, consumer spending growth will likely ramp up this fall. Investors look too optimistic if you judge them by the S&P 500, but if you look at value stocks versus growth stocks, the movement towards pricing in a cyclical recovery has only just begun.

Amazon is on a 5 day losing streak in which it is down 7.4%. That’s not enough to price in a recovery. When Amazon is down 20%, it's safe to say that the stock market is optimistic about a recovery. By the time that happens, the 7 day average of national cases will likely have peaked.

Non-seasonally Adjusted Claims

Seasonally adjusted claims barely fell, but non-seasonally adjusted initial and continued claims actually increased in Thursday’s report. Merrill Lynch expects things to get worse as they are calling for initial claims to rise to 1.5 million in the week of July 18th (from 1.3 million).

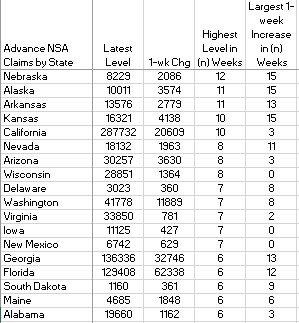

As you can see from the table below, Nebraska had the highest level of claims in 12 weeks and Kansas had its biggest increase in 15 weeks. Arizona, California, and Florida all had big increases, while claims in Texas fell even though it is also one of the major hotspots.

Consumer Confidence Falls

Preliminary July University of Michigan consumer sentiment index fell like expected. This disappointing result went against the record economic surprise index. It was the worst surprise on record. Sentiment index fell from 78.1 to 73.2 which missed estimates for an increase to 79 and the lowest estimate which was 76.

It's shocking that economists would expect an improvement since the Morning Consult and Bloomberg data showed sentiment getting worse. Current index fell from 87.1 to 84.2 and the expectations index fell from 72.3 to 66.2. This decline in expectations is correlated with the spike in COVID-19 cases. Sentiment index is only 1.4 points above the April low.

Commentary by the University of Michigan stated, “Unfortunately, declines are more likely in the months ahead as the coronavirus spreads and causes continued economic harm, social disruptions, and permanent scarring.” I disagree. I think the final July reading will be bad, but if COVID-19 cases start falling again starting in late July and a stimulus is passed, consumers will get more optimistic starting in either August or September. On the other hand, stocks could sell off after a stimulus is passed in a ‘sell the news’ trade.