Strong Last Hour Rally

Thursday was a throwback to the last bull market in which the stock market always seemed to rally at the end of the day. There is a famous Twitter account that is named after the 3:30 PM rallies. In the past few months, we’ve been noticing spikes in the AM futures market. We saw 3AM rallies instead.

On Thursday, the S&P 500 had its best last hour gain since April 17th. From the low early in the morning, the market rose about 2% which was impressive. At first it looked like the market would challenge the low from 2 weeks ago. Then it looked like a boring day of consolidation. Then near the close the market spiked on the news Houston hospitals have plenty of spare ICU capacity. My issue with that rally is the news didn’t make this recent spike in cases go away. Furthermore, Texas and Florida are halting their reopening plans.

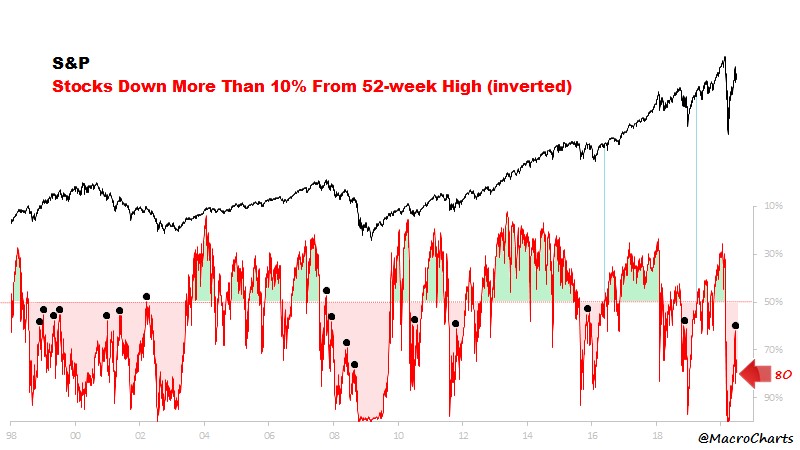

Bad Breadth

We’ve seen conflicting reports of the market’s breadth. Personally, I don’t use it as an indicator, but I do like to know it anyway. If the market is up a lot, but the breadth is bad, there are probably good opportunities available under the surface.

As you can see from the chart below, currently 80% of stocks are more than 10% away from their 52 week high. At the recent spike, it got to about 60%. This makes sense because the FAAMNG names are 24% of the market and they are driving it higher. It seems like these companies have gotten too large just like the nifty 50 stocks in the 1960s and 1970s.

Usually, when a group gets a name like the FANG acronym, it’s a signal of long term gains, with a big bust at the end. Gains have been very strong in the past 7 years. We may be near the end, but some investors are actually way more bearish on the story stocks than these giants.

Buffett Gets No Respect

Latest news headlines are telling us Warren Buffett is done as an investor just like in the late 1990s. This time is different because he is now being criticized for not buying the dip and selling the airlines. He’s not being criticized for missing the tech rally because 20% of Berkshire is in Apple. Berkshire is likely undervalued, but it may not be a good idea to buy it as a contrarian play on tech because Buffett owns so much Apple.

As you can see from the chart below, Berkshire has the same market cap as Shopify, Zoom, Spotify, Square, and Tesla combined. In this group, many investors are very bearish on Shopify and Zoom. This group of 5 names had $33 million in income in the past year, while Berkshire had $10 billion. Obviously, these growth stocks are being valued on the future. Personally, I am confident most won’t achieve great profits, and would rather buy Berkshire. But it’s not close to my favorite stock.

Sentiment Metrics

CNN fear and greed index is at 49 which is neutral. NAAIM investor positioning index fell from 88.25 to 76.57 which means managers aren’t as bullish. If we had access to the July Bank of America fund manager survey, it would likely show these managers heavily invested in the big internet names. Plus, they would probably say it’s the most crowded trade.

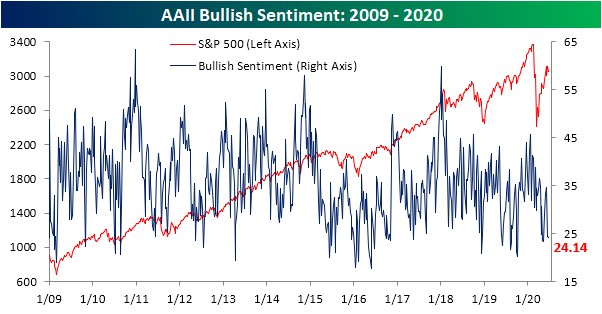

AAII sentiment index is very interesting. Percentage of bulls has fallen for 2 straight weeks as you can see from the chart below. Last time this happened was in January. That’s important because that was the right time to be bearish. It turns out, this indicator isn’t always a great fade.

Specifically, bulls fell 0.2% to 24.1% which is 13.9% below average. It’s very strange to see all these bears with the market doing so well. Obviously, it’s only up 1.3% in June, but it has had a great run since the March bottom. There’s no euphoria in this poll. Percentage of bears rose 1.1 to 48.9% which is 18.4% above average. A 50% threshold is important. Investors became optimistic when it had 3 straight readings above 50% during the bear market.

Nike Loses Money

Nike lost money unexpectedly. It's not surprising that analysts expected it to make money in the middle of a pandemic. In Q4 it lost 51 cents which was below last year’s 61 cent gain. It had $6.31 billion in revenues which was down 38% from last year. Analysts oddly expected a 7 cent profit and $7.32 billion in sales. The stock fell 3.93% after hours on this news.

That’s not good for the rest of earnings season because firms are going to mostly report dreadful results. A potential positive spin is that most other firms won’t have analysts as optimistic as Nike did.

Sales in North America fell 46%, while sales in China were only down 3% because stores reopened quicker. Apparel revenue fell 42% and sports equipment revenue fell 53%. Sports will be likely helped by people wanting to spend more time outside after being cooped up indoors.

However, it will be hurt by the lack of organized summer functions for kids. Margins crashed from 45.5% last year to 37.3%. That’s because when a firm loses revenue and has a lot of fixed costs, it hurts margins. Nike doesn’t want to eliminate fixed costs for a one-time event.

Inventories were up 31% which is obviously terrible for margins. Almost all stores in China were reopened and 85% of stores in North America were opened again. Online sales were up triple digits as you’d expect. Nike expects fiscal 2021 revenues to be flat to up. That’s conservative guidance which makes sense in these times.

Obviously, some improvement is baked in because the stores have mostly reopened. Personally, I won’t invest in Nike because it has a 37.42 PE ratio which is near its one year high. In the past 5 years, the firm has had 33% sales growth and 35.15% in EPS (in total)