Permanent Isn’t Actually Forever

Some people are discussing permanent job loss. That’s mostly ridiculous. There won’t be a permanent increase in the unemployment rate. Permanent means forever. That’s wrong. This unemployment rate will fall back near where it troughed at in early 2020.

People are misusing the term as they seem to be suggesting a long period of high unemployment might occur. That’s possible, but not what permanent means. There are always some economists who claim the labor market will never go back to normal. Throughout the last expansion there were people saying the unemployment rate was structurally high. That was a dramatic miscalculation as the rate fell to the lowest in decades.

With all that being said, there will be changes to the labor market. For instance, some jobs will be gone forever. That’s always the case though because of technology. We don’t have telegrams anymore and many manufacturing jobs are gone, but that hasn’t prevented the economy from getting to full employment.

Secondly, many older people won’t ever get their jobs back. Older people might not come back to work right away because the situation is the most dangerous for them. If they are out of the labor market for a few years in their 60s, chances are they won’t come back. That’s a sad end to a career.

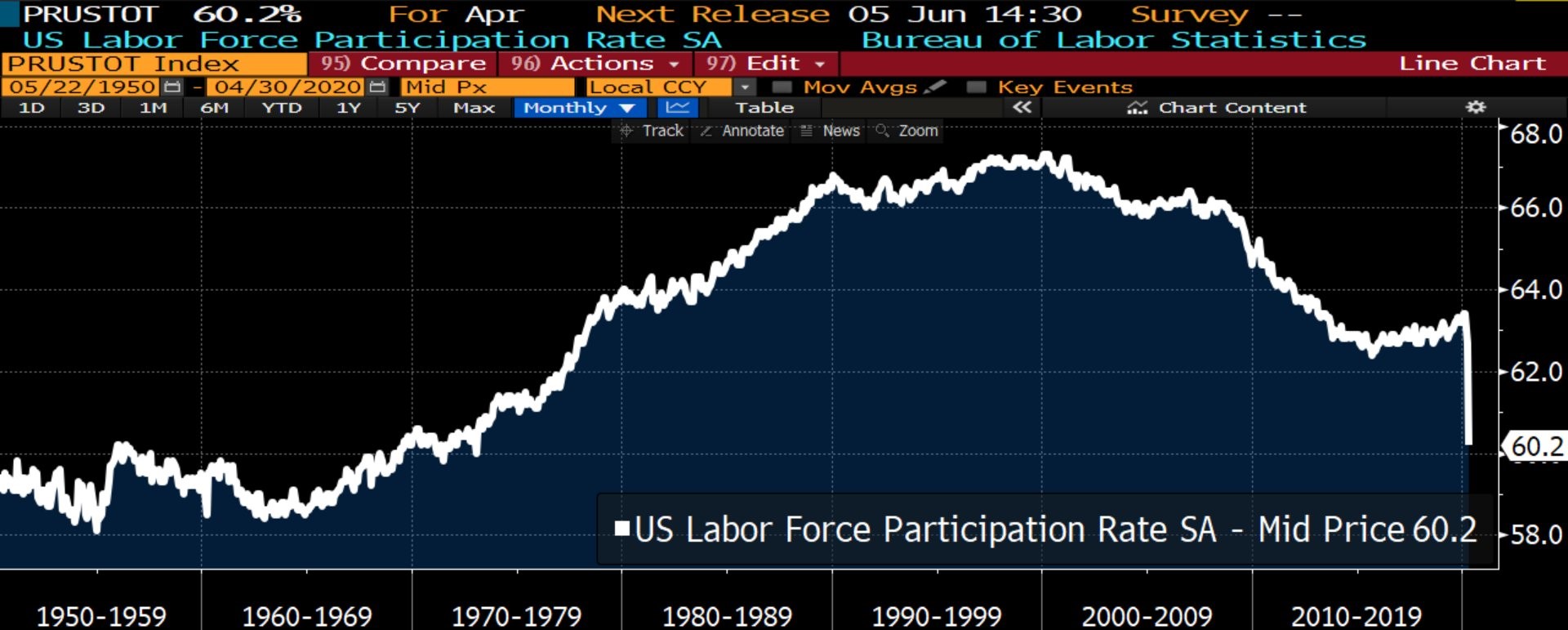

Finally, the labor force participation rate might never get back to where it was at the end of this cycle. It is in a long term downtrend that was interrupted by the extreme demand for labor in the last few years of this expansion. We won’t say this rate will be down forever because we can’t predict demographics. Right now, we are seeing an aging population, but that can change if immigration expands.

The Data Is Ugly

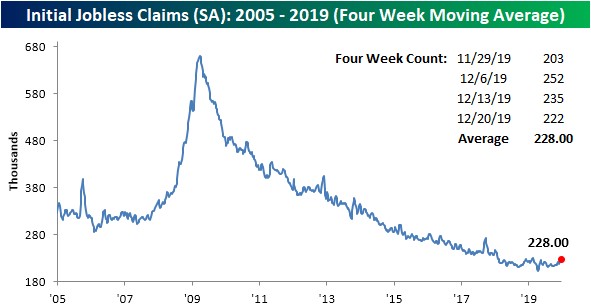

Jobless claims report was too high because Connecticut had a fat finger mistake and said they had 10 times the number of initial claims they actually did. The economy is so bad, people may not have realized it was wrong because we’ve seen previously impossible numbers throughout this recession.

Maybe there is legitimately no one double checking these numbers; if there is someone, that person failed miserably. Specifically, the number of initial claims in the prior report was revised down from 2.981 million to 2.687 million. That means claims fell 489,000 which is very good. At that rate, we could get close to normal in June.

Unfortunately, in this report claims barely fell which was a disaster. The data is ugly. Claims only fell 249,000 to 2.438 million which was above estimates for 2.375 million. If weekly initial claims continue to fall at that rate, we will still be seeing 1.442 million claims per week in 4 weeks. That’s terrible. You’re talking about an economy with an above 20% unemployment rate seeing more claims per week than have ever occurred (before this recession).

We can’t say for certain that we will see the highest unemployment rate ever. But the June report will likely be higher than the May report by a point or two. We will know if this is the worst labor market ever once the May report comes out in a couple weeks.

Making matters worse, there was a 2.2 million increase in claims under the PUA program which is mostly self-employed workers. Government calculates them separately. Most of those were from Massachusetts which signals they processed their backlog. The backlogs for initial claims are mostly gone.

They will likely be completely gone in a couple weeks. Will that be enough to drive claims below 1 million per week in June? We're hoping for that, but many are less confident now that we got this terrible report.

Finally, continued claims increased 2.525 million to 25.1 million in the week of May 9th. When continued claims stop increasing, it means the recession is over. This recession started in March and won’t be over in May. It could end in July if there isn’t a 2nd wave of COVID-19 cases.

A problem is the early recovery will be worse than most recessions because the peak of this recession will see above 20% unemployment. It seemed we were close to a decline in continued claims last week because they only increased 171,000. That’s nothing when you’re looking at an over 20 million base.

However, the spike in this report signals we are a few weeks away from a decline. Because of this spike, it's probably better to see 3 weeks of declines before we can dub the recession over. It’s really easy for the number of continued claims to fall because so many people are unemployed. It’s like how it’s easy for a student to raise its average if it is failing a class.

If the student gets a C, its average will rise even though that’s a fair score. That’s not usually discussed by the main stream media because it sells negativity. While this report was bad, it's good to always open to a recovery since many states are reopening. Even if some people get their jobs back, the labor market will improve from the worst it has been since the Great Depression.

Conclusion

This is the worst labor market since the Great Depression if we’re lucky. The stock market basically ignored the jobless claims report. It only fell because it was overheated on Wednesday. The stock market could be in for a rude awakening if we see the recovery going slower than expected.

It will be quicker than most recoveries because we have so must room for improvement. However, that’s only on a rate of change basis. We could be 6 months into the recovery and still have an unemployment rate above 10% which was the peak of the last recession. An early recovery will look like a recession.

1 Comment

Mac162

May 27, 2020I disagree with John Galt's statement, "This unemployment rate will fall back near where it troughed at in early 2020." Today's current unemployment percentage was last seen in the mid 1970's. There were less people in the America in the 1970's than now. This made it easier to find jobs for the unemployed in the 1970's. Also, in the 1970's there were not 8,000,000+ work visas (e.g., H1A and H1B visas) taking high paying jobs away from American workers. Also, there are many more college graduates flooding the white collar job market than in the 1970's.

The stock market has disregarded bad second quarter results because of the covid-19 virus. Investors are trying to bid stock prices up to their pre-covid-19 levels because the investors have their life savings in the stock market. Investors' have convinced themselves that companies are still worth the same as pre-covid-19. This is false. Companies are not worth the same amount as pre-covid-19. Today most companies have crushing debt and little if any revenue.

Additionally, Stock Funds are bracing for a smaller but inevitable dump of second quarter IRA and 401K money.

By ignoring the terrible second quarter companies' results, and not factoring in the loss of jobs by the big and small companies going bankrupt will create another stock bubble waiting to pop. I am not an alarmist, but investors need to understand the true worth of companies they are investing their life savings in.

Also, I believe small companies, which provide employment to 90+% of American workers, will be hit the hardest. Most small companies normally run on a shoe string budget, and they often rely on overseas companies to supply raw materials or finished products. The worldwide two+ months of work stoppage will force many of the small businesses under because of lack of raw materials or finished products, lack of re-startup funds, or lack of customers. The failure of many small and large companies to restart their business will take away a large portion of the jobs they provided.

The next six to twelve months will be the crucible determining if America survives the covid-19 virus aftermath.