The bears are waiting for a catalyst for stocks to crash, but they’ve been waiting for quite a while with nothing to show for it, but losses. Valuation has not been shown to work as a sell signal. The fundamentals of the economy and corporate earnings haven’t been able to move the market lower even though, as I will explain in this article, they look ominous. Political risk has been ignored as well. If anything, it has sent stocks higher. Finally, monetary policy tightening, which was once a thorn in the bulls’ sides, has also been put to rest as far as being a potential catalyst for a correction.

The next potential catalyst on this list is a fiscal policy mistake. I quantify a large tariff on any trade partners a mistake. This is exactly what Trump is proposing. The latest reports are that he’s expecting to put a 20% tax on Mexican products to pay for the border wall. Ignoring the immigration policy, this tax will hurt the consumer. There’s only two options. Either the production will come to America at a more expensive price or the tax will be paid on the Mexican products. Trump wants the production to come to America, but it’s not that easy to change long term production plans for a tariff which may be in place for only 4 years if Trump doesn’t win re-election. This means the consumer will pay more for imported goods and there won’t be any more jobs to show for it.

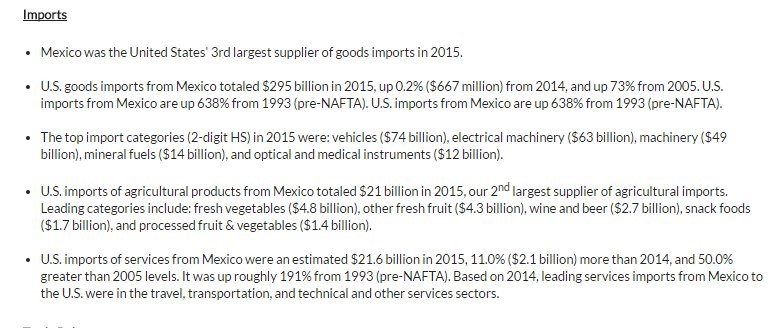

At best, a tariff subsidizes American production and at worst, it is a pure tax with no benefit to anyone. While I am in favor of a consumption tax instead of an income tax, this is being employed to bring jobs back, which it won’t. The screenshot below shows the goods America imports from Mexico. Mexico is a major trading partner with America. It’s the third biggest supplier of imported goods. This tariff will make imported cars, electrical machinery, machinery, mineral fuels, optical and medical instruments, agricultural products, and services more expensive to the American consumer.

The big question now is what policies are next. Specifically, most investors will want to know what the tariff on China will be, if there is one. Clues to what the tariff on China will be may come from whether you think Trump only put the tariff on because of the wall or whether he used it as an excuse. If he put it in place to pay for the wall, then this policy doesn’t have implications for China. If he used paying for the wall as an excuse and he really did it to try to bring American jobs back from overseas, then it means a similar tariff will be put on Chinese goods. I think the answer is the latter because he has discussed tariffs with other nations which don’t border America.

Trump spoke tough on China for currency manipulation, its ignoring of American intellectual property rights, not letting American firms compete in China, and for its dumping of products such as steel in America. Considering his rhetoric was tougher on China than any other nation, I expect it to happen at some point. The initiation of a tariff on China could be a catalyst for stocks to fall as American discretionary spending will fall by the amount of the tariff.

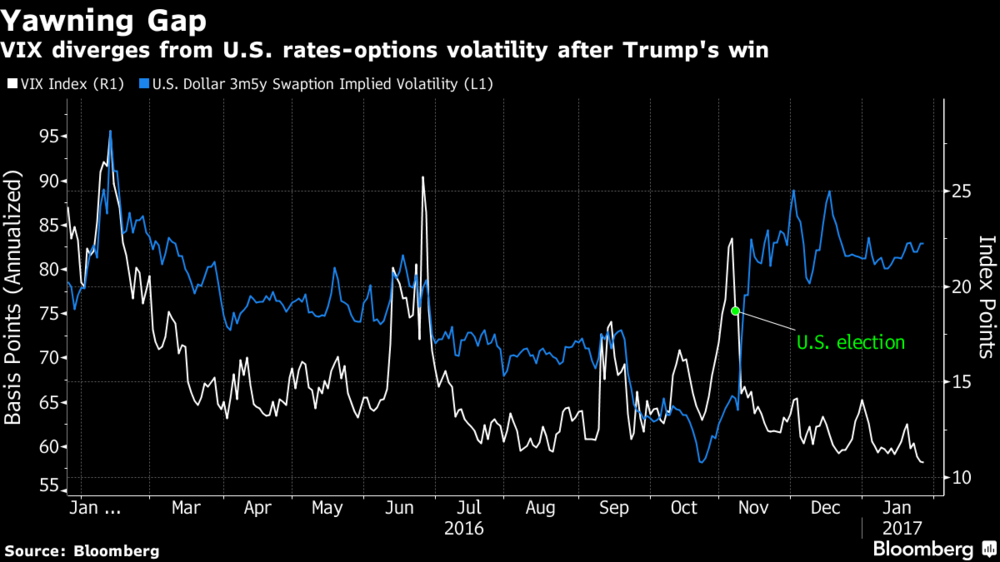

As I mentioned, I will continue to look at fundamental analysis even if it hasn’t shown to move stock prices. The chart below shows the VIX, which is a measure of stock market volatility, with the swaption implied volatility, which measures the uncertainty surrounding Federal Reserve policy. The stock market is going higher and ignoring any of the increased uncertainties surrounding what the Fed will do. Considering the increase in inflation causes me to give a higher chance of a rate hike this year than last year, I agree with this index’s increase. In the past, when rate hikes were discussed, stocks sold off. Now they ignore any risk of rates going higher which would provide higher competition for stocks.

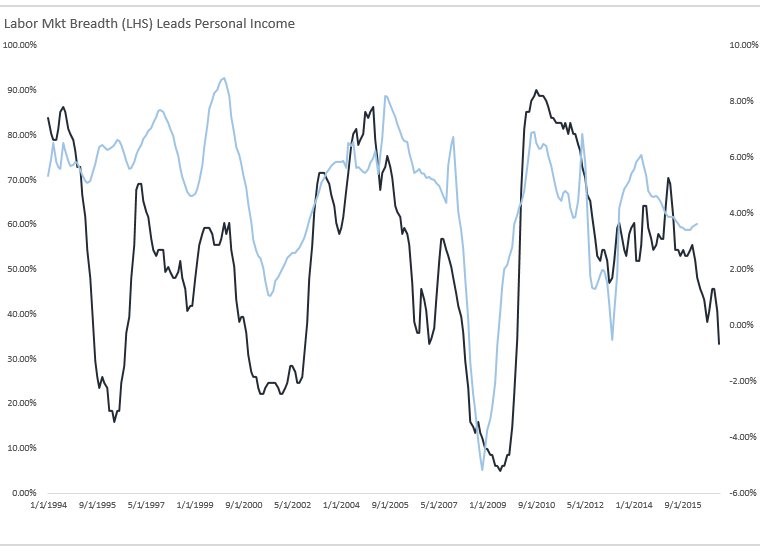

The chart below gives you a unique picture of the labor market. It shows the labor market breadth in comparison to the personal income growth. It has been a leading indicator for income growth and it has recently been declining. The labor market is off its peak, but there hasn’t been a big down shift just yet. The way I look at the market, we are testing a new approach where we see how much the wealth effect from the stock market going up can maintain strength in the labor market. The Fed claims it is lowering rates to help the labor market, but its main effect has been cheap debt used to buyback stocks and make acquisitions. It’s not a direct action which leads to job growth.

The Fed has maintained the pedal to the metal which makes it a grand experiment to see when a high stock market will no longer be able to help keep the labor market afloat. This is a question a first-year economics student may ask: “what would happen if the Fed kept interest rates low forever?” The caveat of my perspective may be playing out if the Fed extends this recovery a couple more years. In arguing against this policy, I start out by saying it causes unintended consequences and end by saying it won’t produce much growth in the short term. My second point may be wrong. Maybe the benefit of short term growth is higher than I anticipated. The depth of the recession will then determine if the first part of my hypothesis is accurate.

Conclusion

The tariff on Mexico will hurt the American consumer. A negative future catalyst for the market is talks about a Chinese tariff being put in place. I was wrong. I didn’t think high tariffs would be implemented. This only supports my bearish view on the market. On another note, the VIX isn’t pricing in monetary policy risk. Stocks used to care about rate hikes, but now they don’t. Finally, the Fed’s policy may have helped keep the labor market strong for an extended period of time, but once it ends, the burst will be bigger than recessions in the past because of this massive debt build up.