Just as I forecasted, the tech stock selloff ended Wednesday as the Nasdaq rose 0.73%. The S&P 500, Russell 2000, and the Dow Jones Industrial Average all hit an all-time closing high. The ECB’s $60 billion in bond buying per month combined with investors putting money into ETFs with a “buy the dip” strategy means the market has an endless bid. It was reported on CNBC that only 10% of the trading in the stock market is regular stock picking. 60% of trading is passive and quantitative which is double what it was a decade ago. This means passive and quantitative strategies have yet to dominate the market in a downturn. It will be interesting see how this alters the selling. It could become indiscriminate.

The positive aspect of this change is if you do your own research, it could be easier to find diamonds in the rough. The problem is in order to have the stocks reach their intrinsic value, this trend in passive investing would have to reverse. The way you analyze stocks in the meantime must be based on how the robots do it. Instead riding the waves of big hedge fund whales who do fundamental research, investors must follow the stocks the quants like. This trend in passive investing will continue until a change in the market causes this strategy to do poorly. It could be increasingly dangerous if there’s no major correction in the next few years because then everyone will be passively investing.

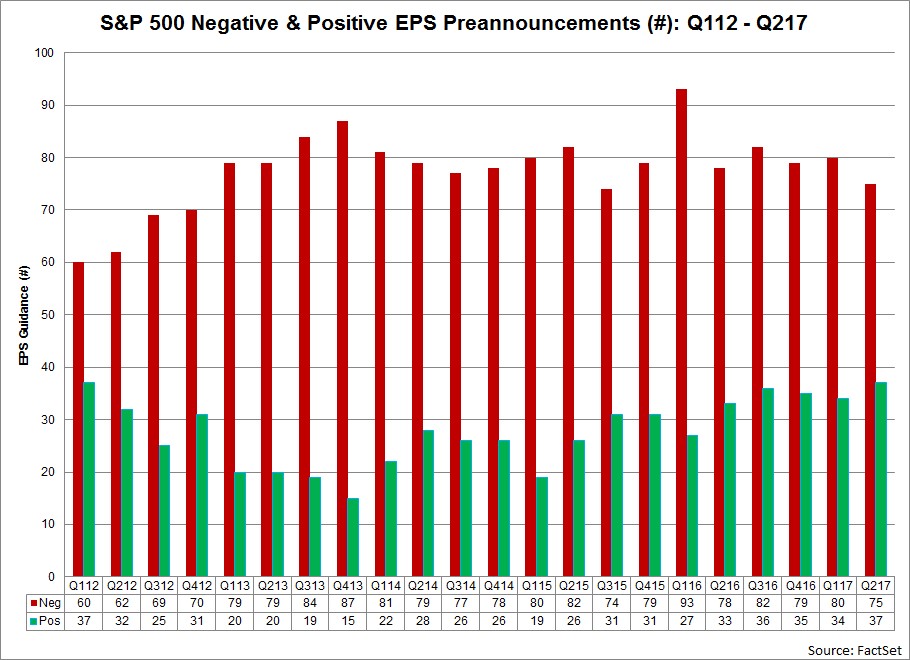

Even though the market may act wonky in the intermediate term due to these changes, I still think valuing stocks based on their future earnings makes sense. Therefore, let’s look at the latest stats on the bottom up S&P 500 earnings reports. As you can see from the chart below, there were 37 firms which had positive EPS preannouncements between Q1 and Q2. This is the highest number of positive preannouncements since Q1 2012. It was 9 higher than the peak of earnings season in Q3 2014. Clearly this past quarter was great. We’re now just tallying the score sheet to see how good it was.

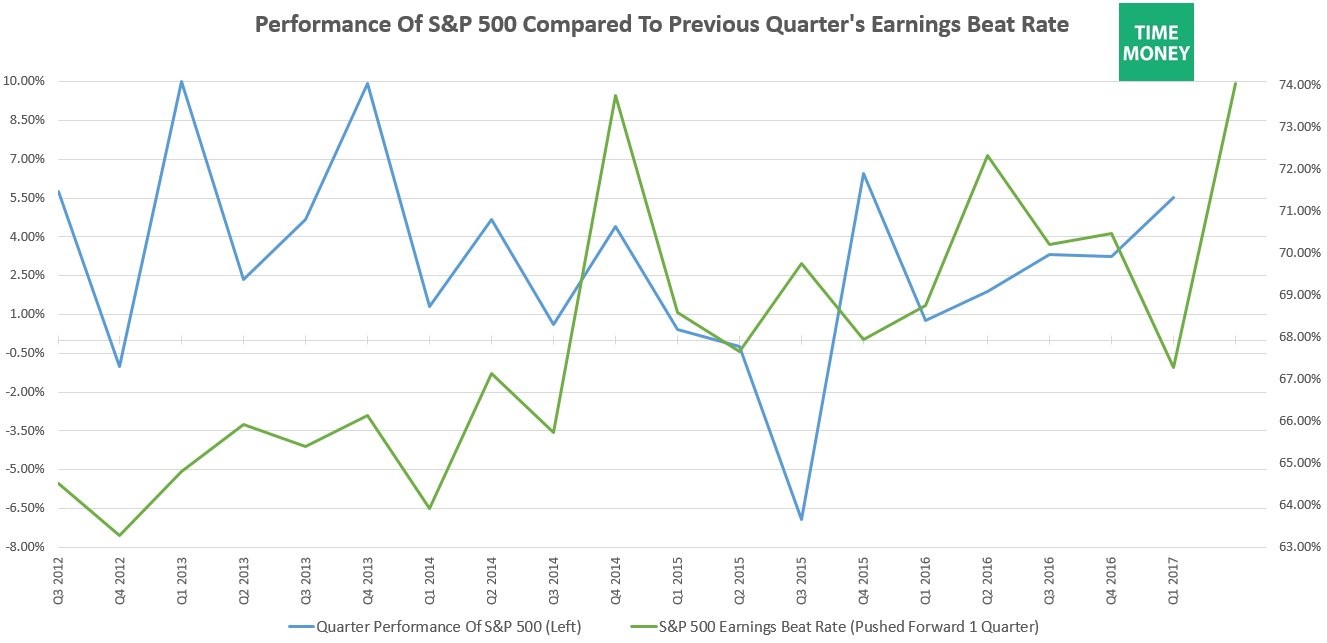

While earnings beats should be great, they haven’t led to stock outperformance. The chart below shows the earnings beat rate pushed forward compared to performance of the S&P 500. The earnings beat rate must be pushed forward because firms report their quarters in the next quarter. Even this isn’t perfect because of the timing of reports. Even with this imperfection, I find it interesting that there is a slightly negative correlation to how stocks perform versus the earnings beat rate. This historical relationship will probably be broken this quarter as the 74% earnings beat rate will coincide with an up market. The best reason for this lack of correlation is likely because earnings beats are only part of the equation. It depends what they’re beating. Estimates can be manipulated by analysts. You must watch for this when a company you follow reports. Ask yourself if a stock should go up to a new all-time high if the estimates it beat were lowered from 4 weeks ago.

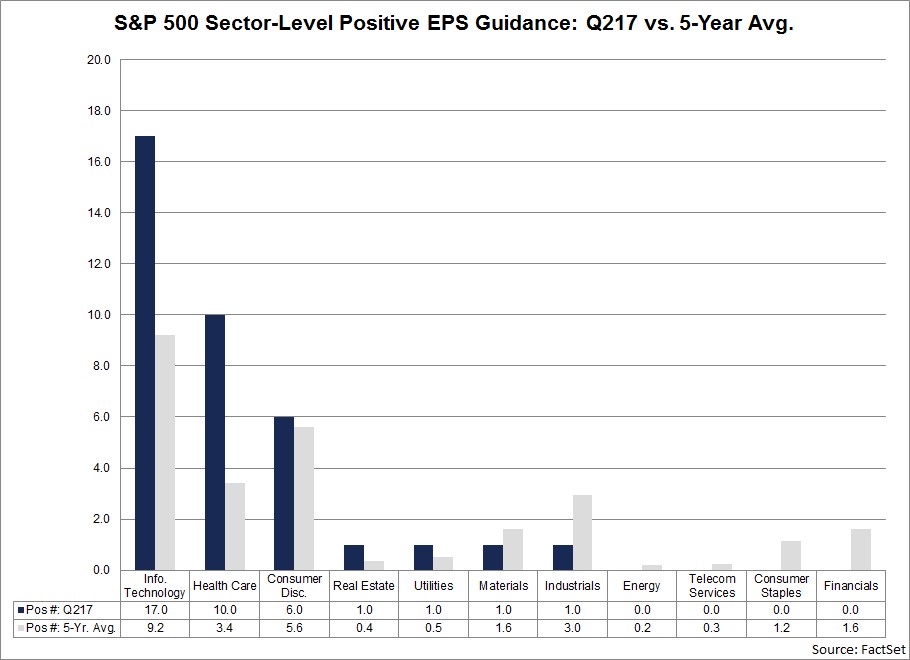

The chart below breaks down the sector level performance of firms’ guidance. Guidance is another important aspect to reports which the earnings beat rate stat doesn’t cover. Information technology had a 17.0% rate of firms with positive guidance which was much higher than the 9.2% 5-year average. This is part of the reason why I didn’t expect the latest technology selloff to continue. NVIDIA stock got overheated, but an overbought market isn’t what causes speculation to end. There needs to be a change in the earnings trend. After all this market has gone through climbing the wall of worry, I wouldn’t expect stocks to fall after a great quarter.

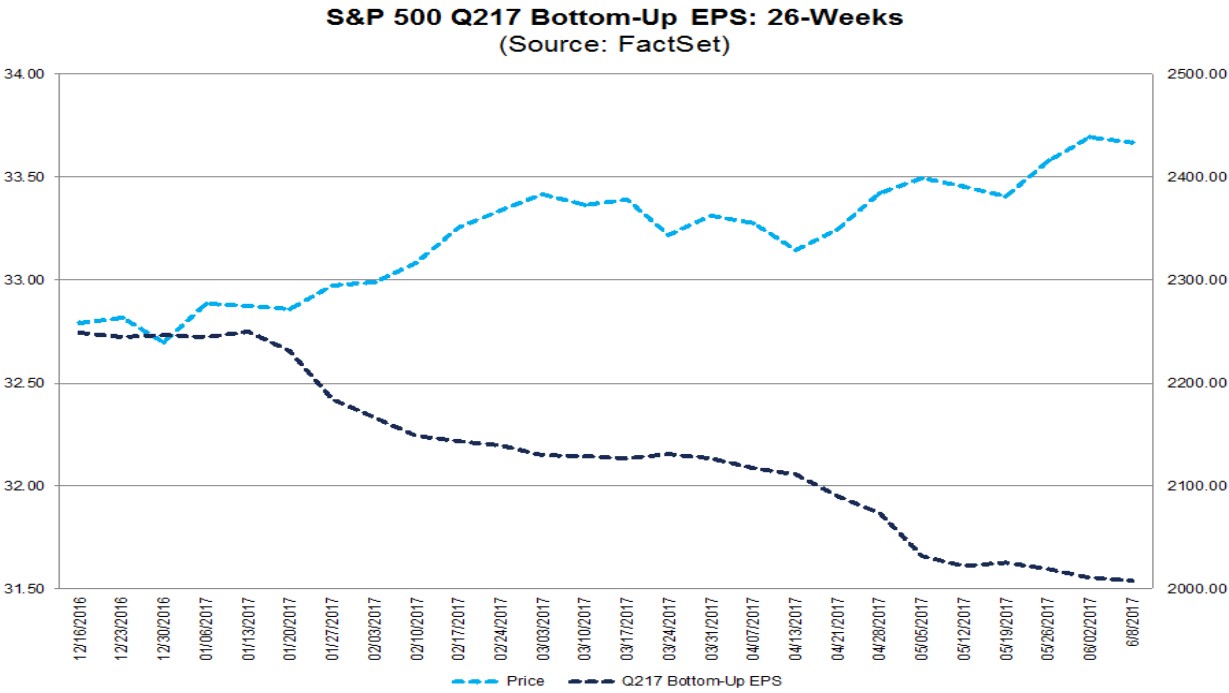

The latest earnings forecasts have come down recently for Q2 bottom up earnings, but not enough to stall this rally. As you can see, bottom up estimates have fallen by a few pennies while stocks power higher. On March 31st, Q2 earnings were expected to grow 8.7% and now they’re expected to grow just 6.6%. My prediction that earnings growth would stall after Q1 is coming true. However, it’s also worth noting that the as reported growth figures will be higher. Full year earnings are expected to grow 9.9% which is down from estimates a few months ago, but is still above my estimate for 5%-7% growth. It’s still too early to conclude if that prediction was right or wrong. I am much more bearish on 2018 earnings, because of the margin ceiling and the tough comparisons they will face in the beginning of the year. It’s difficult to grasp how the market will react to 2018 earnings growth which is half of expectations because this entire bull market has been built off lowered estimates.

Final Thoughts On The Fed

As this is my last article before the Wednesday Fed meeting, I will give my final perspective before the release. As you can see in the chart below, the Citi G10 inflation surprise index is declining along with the Chinese inflation surprise index which is liking falling because China has pulled back on its stimulus. This sharp decline has occurred since the last Fed meeting which furthers my expectation for a dovish Fed and a boost in stock prices. My analysis that inflation was slowing was more of a prediction which ended up being accurate. I was surprised to see the Fed ignore the evidence to support my prediction. Now that the results have come through, I don’t think the Fed has wiggle room to stay hawkish.

Conclusion

While the earnings beat rate may not forecast stock performance, the positive guidance from tech stocks is preventing a larger selloff. I’m expecting stocks to do well until earnings season which starts in a few weeks. The ECB’s bond buying program and the great earnings reports from the big 5 tech stock have allowed the Fed to raise rates despite the weak GDP growth in Q1. Now with inflation declining I don’t see the need to raise rates 3 times this year. I will cover the Fed’s decision in my next article.