Wednesday was a huge up day for stocks which extended some of the latest trends making the statistics look even more gaudy. As you can see from the chart below, the 10 day realized volatility of S&P 500 is at 2.57. This makes sense because none of the risks I talked about in August have occurred in September. Just because September is typically a risky month for stocks isn’t enough for stocks to move lower. The debt ceiling has been raised, there’s no more uncertainty about healthcare legislation, earnings growth looks solid in Q4 and beyond, and the dollar has been weak. There are also animal spirits which push stocks up just because they’ve been going higher. Momentum is supported by recency bias. Everyone wants to get involved when the stock market goes straight up without any bumps. It’s a more intriguing market than previous ones which have had better performance because there hasn’t been risk of stocks correcting right after you buy them. Investors who buy now will be in for a shock when stocks have a correction; they important factor now is that they are buying.

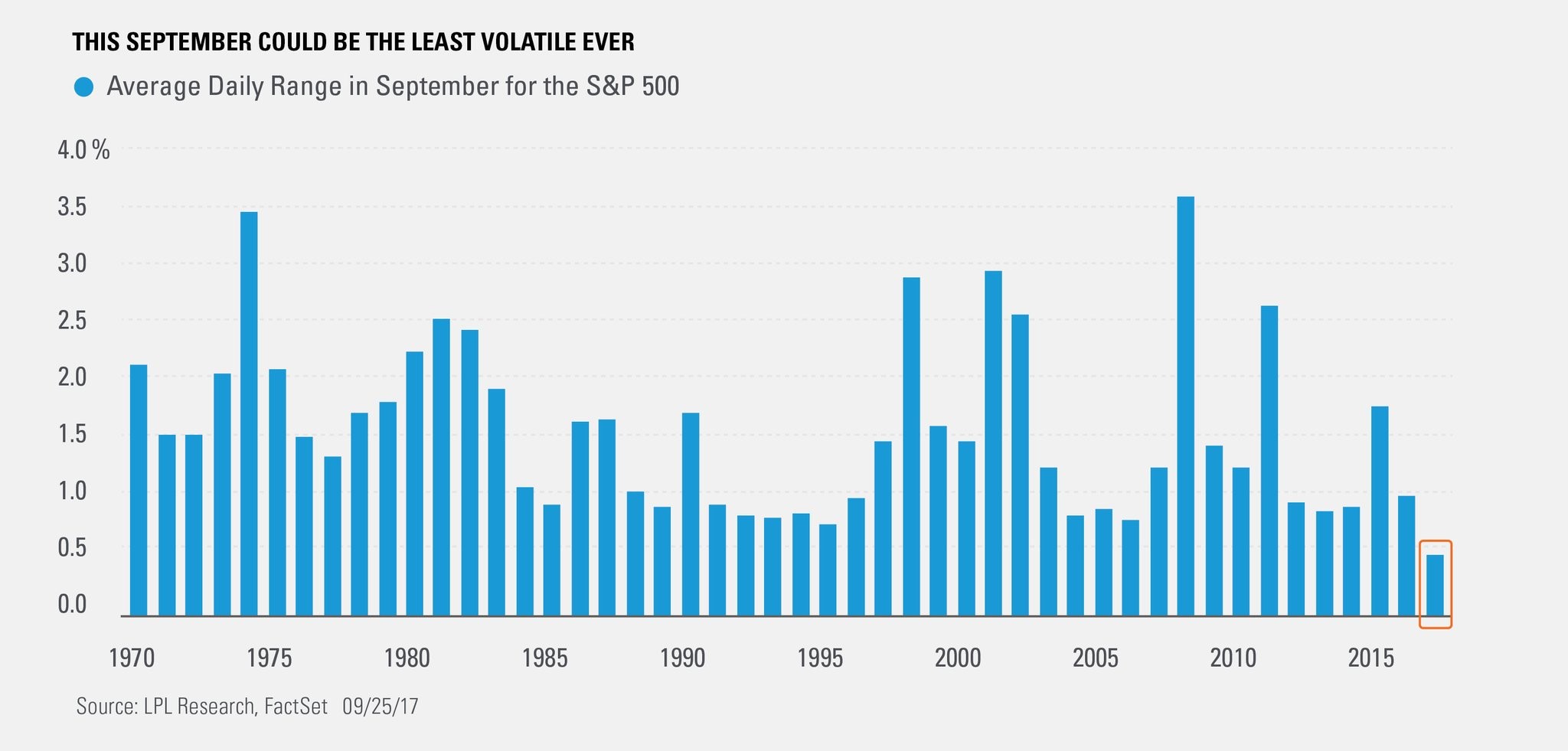

As you can see from the chart below, the average VIX daily range is the lowest for a September ever. This chart only goes back to 1970, but the 0.38% average daily move is the lowest since 1928. The S&P 500 hasn’t even been the best index in the past few weeks. The Russell 2000 is up 9.41% since August 21st. This is the strongest rally since the 20% one after the election. Those who claimed Russell 2000 weakness meant a correction was coming in the S&P 500 were grasping at straws. It depends why the Russell 2000 is down; if you make the case that the small caps underperforming means the overall market will fall, you’ll have many false indicators telling you to sell when you shouldn’t.

The catalyst for Wednesday’s rally was tax reform. As you can see from the chart below, the odds of corporate tax cuts passing by the end of 2017 have increased from 30% to 35%. Some of the details of President Trump’s plan were released today, so let’s review them. The individual tax brackets will be cut from 7 to 3. The rates will be 12%, 25%, and 35%. The current bottom rate is 10% and the top rate is 39.6%. The bottom rate payers would benefit from the standard deduction being doubled from $12,000 for individuals and to $24,000 for couples. The child tax credit will be increased and there will be a $500 credit for those who care for a child which isn’t theirs.

The estate tax and the alternative minimum tax will be repealed under this plan. The corporate tax rate will be cut to 20%. The pass through tax rate will be cut to 25%. Businesses will be allowed to write off all the costs of their capital investments for 5 years, but the ability to deduct interest expenses will be limited. This expensing change could spur more private fixed investment. It won’t necessarily fix the problem of why there’s not much productivity growth. The reason why I say that is because businesses would already be investing in new initiatives if it paid to become more productive. The reason why they don’t is because it isn’t advantageous to do so. Therefore, I expect any increase in fixed investment to only marginally improve productivity. Many critics of buybacks claim that the corporations are wasting their money, but the question is where should they put the capital. Each business has different places to put it, but low wage growth doesn’t encourage them to try to make workers more effective.

The framework of the tax proposal lets committees change it slightly. One example of this is adding a 4th tax bracket for the very rich. The other is deciding which tax breaks on businesses will be eliminated. The entire point of tax reform is supposed to be eliminating deductions and lowering the rate. That would make the tax code change revenue neutral, but make it simpler to file and make it fairer. Tax cuts could be pushed along with reform, but it looks like this plan is heavy on the tax cuts and light on the reform measures.

The final change which is a bit of a reform is moving towards a territorial system. This means U.S. foreign subsidiaries’ dividends won’t be taxed, but there will be a minimum tax on foreign profits. To make this change easier, there will be a one time repatriation tax holiday. The repatriation tax will have two rates. The higher one will be for liquid assets and the lower one will be for less liquid assets. This change might make the effects of the repatriation holiday different from the last time. The last time it was done, there was an influx of buybacks. This time probably will be different because the corporate interest rate is so low that it’s cheap to borrow against foreign profits to buyback stock. The tax on foreign profits doesn’t incentivize the money to be brought back to America because the money on the balance sheets has already been made. Once the holiday is over, the only difference will be slightly more taxes paid on overseas earnings. The key determining factor on how much cash is brought back is how low the holiday rate is for cash. The closer it is to 5%, the more will be brought back to America. The closer it is to 10%, the less will be brought back.

The only way for the tax system to permanently be set up for the money to flow back to America would be if the tax on foreign earnings is waived if it’s brought back. That would be different from the repatriation holiday, because the tax on foreign income earned is a new tax. This new tax could be a drag on long term earnings as it would hike the effective tax rate on multinational companies.