Tariffs - Redbook Sales Growth Weakens Slightly

Before getting into Tariffs, let's review Redbook. Redbook same store sales growth reading in the week of June 22nd was more interesting than usual. On Tuesday the consumer confidence report came out.

Investors want to know if the decline in consumer confidence actually means consumers are spending less. Remember, in the Dallas Fed report, a firm stated that it wasn’t seeing weakness. But it was preparing for it.

Similarly, consumers might be expecting the worst on trade, but not actually changing their spending habits. Inflation is falling even with the tariffs. However, that’s because of the decline in demand. If the economy was seeing accelerated growth, inflation would be increasing. It would be topped off by the tariffs.

Redbook same store sales growth rate fell from 5.4% to 5%. Sales aren’t falling off a cliff. But this report didn’t exactly calm investors worried about the consumer. There was a big decline in confidence. Also, we got a modest dip in same store sales growth.

Actual retail sales reading could show greater weakness than Redbook. Which is why it won’t calm many investors.

Consumer Confidence Craters In June

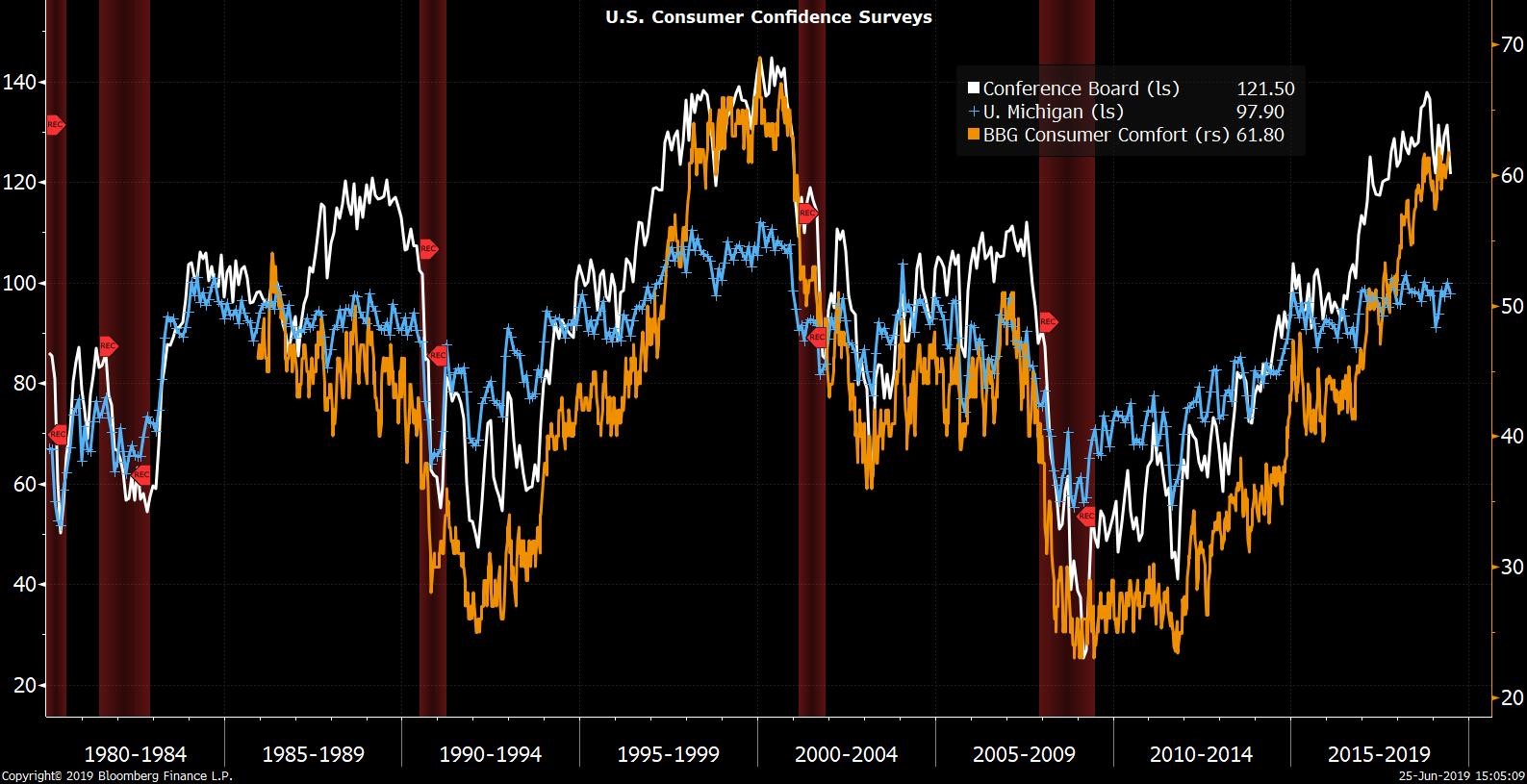

Tariffs - Specifically, the June Conference Board consumer confidence index fell to its lowest level since September 2017. It went from 131.3 to 121.5 which was its sharpest monthly decline since late last year.

Even worse, the May reading was revised down from 134.1 and the June reading missed the low end of the consensus range which was 128.8. June consensus was 132 which means economists had expected a modest decline from the initial May reading.

As you can see from the chart below, the Conference Board index has seen a bigger decline from its recent peak than the University of Michigan survey and the Bloomberg Consumer Comfort survey.

The present situation index fell from 170.7 to 162.6 which is a pretty big drop. It signals that consumers may have held back on purchases instead of just getting negative on the future.

Tariffs - Will we finally see a major effect on the economy as a result of the tariffs?

We will find out in the June retail sales report which comes out on July 16th. Unsurprisingly, the expectations index took a huge dive as it went from 105 to 94.1.

The cutoff date for this survey was July 14th. There haven’t been any major positive or negative news stories on trade in the past few weeks. So the consumer is up to date on the trade news as of this survey.

Consumers are very worried about the trade war and rightly so based on the latest negotiations. Good news is this negative report might entice President Trump to negotiate with a more open mind at the G-20 summit. He doesn’t want to see the economy fall into a recession.

Details Of June Conference Board Index

Tariffs - Present situation index fell because consumers were less optimistic on the business environment and labor market conditions. Specifically, the percentage of consumers saying business conditions are good fell from 38.4% to 36.7%.

Positive news is the percentage of them saying conditions are bad fell from 11.7% to 10.9%. Percentage saying jobs are plentiful fell from 45.3% to 44%. Obviously, that doesn’t look that bad.

This June consumer confidence report was the case of an indicator going from great to good which some fear is a sign of more weakness to come.

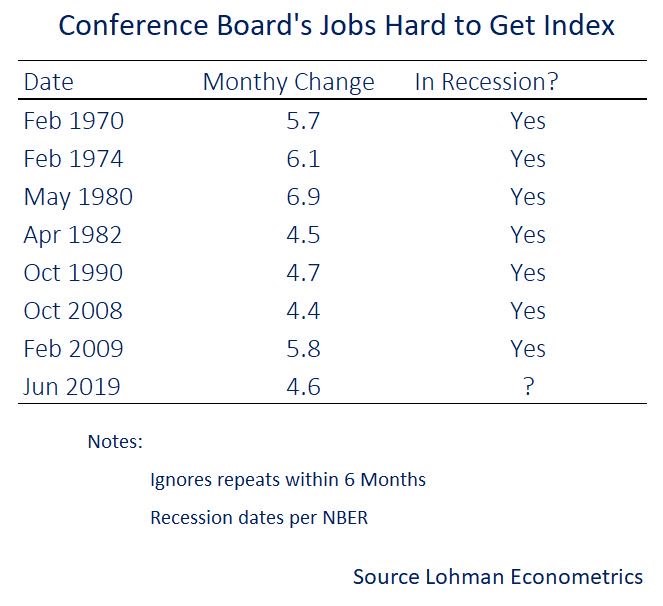

One of the worst parts of this report was that the percentage of consumers saying jobs are hard to get increased from 11.8% to 16.4%.

The table below reviews the monthly changes to this index. It ignores the repeats within 6 months to unclutter the data.

Every single monthly drop was in a recession.

Tariffs - I don’t have the data on this survey going back to 1970. But I’m guessing the percentage saying jobs are hard to get was higher in those periods. This is the case of a report going from great to good.

It’s still a good reading and doesn’t mean the economy is in a recession. This just shows how bad the decline was. However, it’s only one month of data. It doesn’t mean there’s a trend. The situation can quickly change if there’s a trade deal.

Percentage of consumers expecting business conditions to improve in the next 6 months fell from 21.4% to 18.1%.

Tariffs - The percentage expecting business conditions to worsen increased from 8.8% to 13.1%. In other words, the net percentage seeing business conditions improving fell from 12.6% to just 5%. That’s a significant drop.

Finally, looking at the labor market, percentage expecting more jobs in the next 6 months fell from 18.4% to 17.3%. Percentage expecting fewer jobs increased from 13% to 14.8%. Many economists view the survey results on the labor market to be the most important. It’s what consumers know best.

Consumers pay the closest attention to their job prospects. It determines their financial wellbeing. They can be fickle when it comes to making purchases. But when it comes to their job prospects, the situation is more serious.

Tariffs - 2.1% GDP Growth Now Expected In Q2

Tariffs - Consumer confidence reading probably won’t affect many GDP estimates because it’s a soft data report. Soft data has been hurt more than hard data by this trade war. It has made businesses and consumers nervous.

It’s likely that the biggest effect of the trade war will the decline in sentiment unless it becomes an all-out war. That’s what most are fearful of.

This point explains why the updated CNBC rapid recap of Q2 GDP growth projections shows the average estimate is at 2% and the median of 11 estimates is at 2.1%. Both are up from 1.9%. This isn’t a significant change.

But it shows the economy likely isn’t in a recession like many fear. Humans tend to jump to conclusions rather than wait for the facts to change. Investors are especially this way. The only way to make money is to get in ahead of the trend change.

They need to short now before data consistent with a recession comes out.