Will The Swiss Buy More Stocks?

An interesting dynamic at play is what will happen when the ECB and the Fed start to reverse course and taper and unwind respectively. We’ve discussed this many times in articles. The new wrinkle to this mix is what the Swiss Central bank will do especially if stocks start going south. As you can see in the chart below, the Swiss Central Bank has now bought $84 billion in U.S. stocks. I don’t see any reason why the SNB can’t buy more stocks in 2018.

The global central banks made up for the Fed when it stopped purchasing bonds. The central bankers got together and did coordinated liquidity injections when the economy was about to go into a recession in 2016. Will the Swiss Central Bank act as a backup plan in case things go awry? We don’t know the answer to this question, but I wouldn’t be surprised to see a tick up in the bank’s purchases. It’s tough to decide what to do with this information. The SNB buying stocks is clearly bullish, but anyone who pays close attention to what the central bankers are doing is probably hedged or doesn’t own stocks at all.

Apartment Rents and Housing Prices Are Too High

Whether housing is in a bubble is a topic we have discussed. My point has always been that housing isn’t in a bubble because there hasn’t been a bonanza of subprime loans given out with little money down and no documentation. This activity which boosted valuations in the early 2000s market is why I consider that a bubble. The one aspect that is similar now is that rates are artificially low, making housing more affordable. When I say artificial, I mean that the Fed has rates below the Taylor Rule. When you look at the shadow Fed Funds rate, the rate is even more artificial since it went into the negatives.

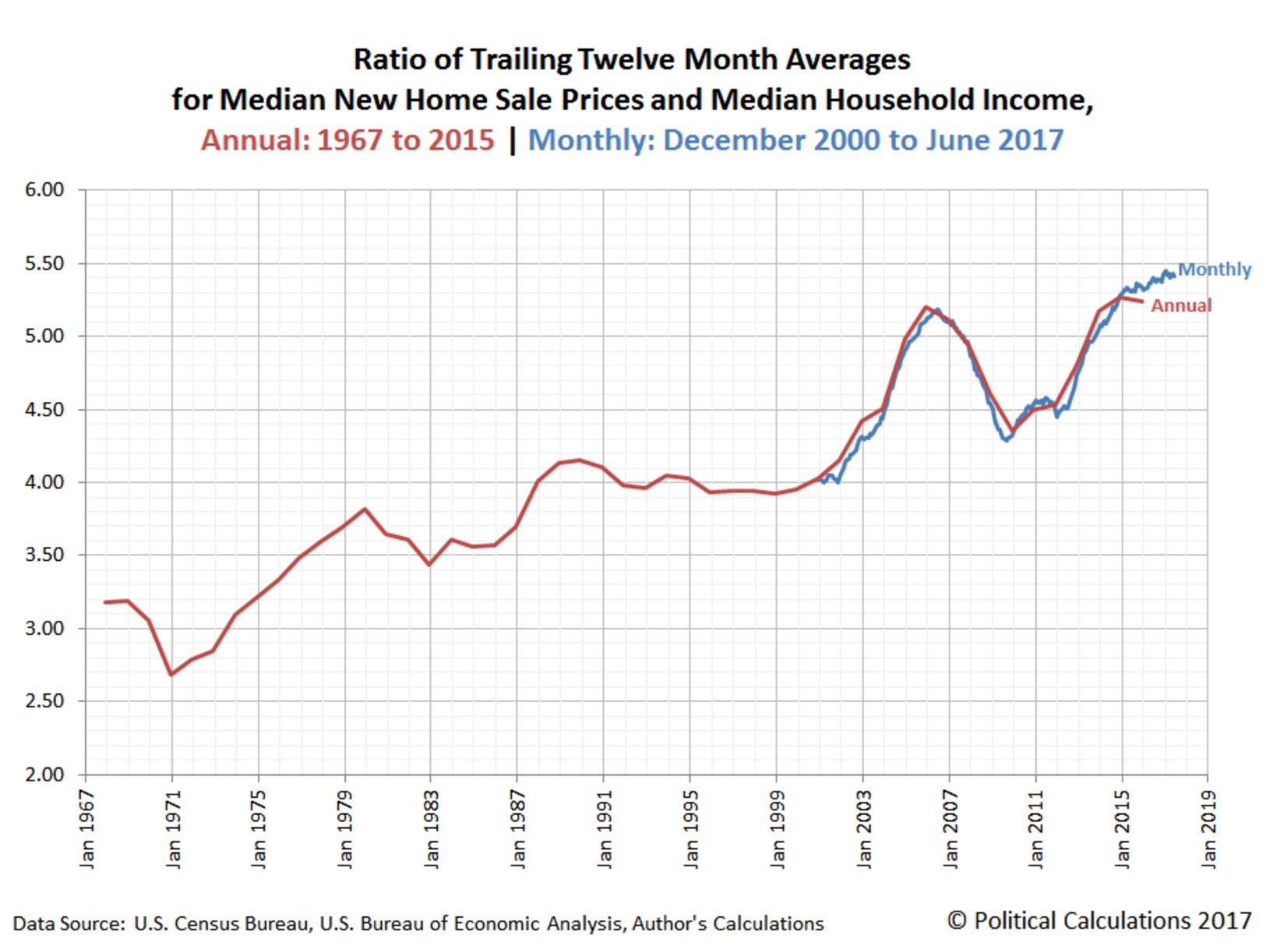

The chart below is the ratio of median new home sales to median household income. I don’t deny the fact that housing is expensive. Both rent and housing expenses are one of the few costs which have hurt the consumer in the past few years. Clearly wages haven’t caught up because this chart adjusts for that. Whether this is technically a bubble won’t be reviewed when housing prices fall because it will hurt the economy. However, you will notice the low default rates because more qualified buyers own houses in this cycle. That will prevent the cascading downward effect on prices like what happened in 2008.

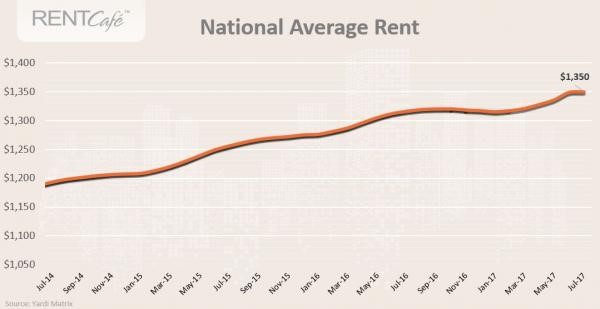

As I have mentioned, rent expenses are high. They have reached the highest percentage of GDP ever. That might be why the national average recently stopped rising as you can see in the chart below. Even with rising hourly wages, people can’t afford to pay these high rents. Millennials are more likely to live in cities. Their wages will likely be lower than what their parents made during their working careers. Rising rent expenses don’t jive with that trend. One reason why rent and housing costs have been increasing in some of the major cities like San Francisco is because there are zoning restrictions on where you can build a house or apartment building. This means it isn’t a free market.

Zoning requirements affect some areas, but as a whole, there has been a burst of apartment buildings which will create a hangover effect. This effect is when too many complexes are built, pressuring rents. This year, the number of apartment buildings built is up 21% from last year. Many builders aren’t great at foreseeing the problems they cause to the supply and demand balance when they build a new apartment building. There needs to be a price signal, where rents fall, to stop the onset of this new supply. This reminds me of the oil market. Many frackers continued to drill for oil even though the market was in oversupply. It took a huge price shock to slow production. Oil drillers only know how to drill; they aren’t economics experts. Home builders only know how to build houses; they can’t predict rent prices.

New Earnings Paradigm- Stocks Always Fall

In a previous article, I showed how stocks were going down whether they missed, met, or beat earnings expectations. That was a change in the trend because stocks were falling less when they missed estimates than in the recent past. Before this latest quarter, some prognosticators were blaming ETFs for the increased volatility during earnings. Just as this trend was mentioned, it disappeared, showing that ETFs had nothing to do with the volatility, since ETFs are still popular and the volatility is gone.

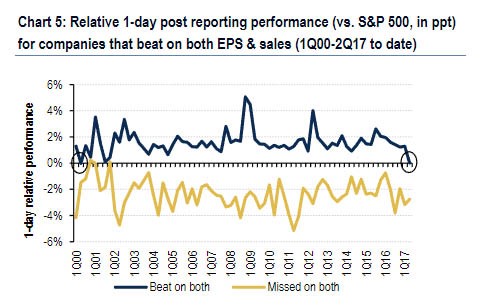

The more shocking story this quarter isn’t the lack of volatility from firms who miss estimates; it’s the lack of gains from winners. As you can see in the chart below, this new reaction is very rare. The last time stocks which beat sales and EPS had their stocks fall relative to the S&P 500 was Q2 2000 before the tech bubble burst. That is a disconcerting stat. I wouldn’t go as far as saying the market is about to crash in the next few years though. This stat shows us that optimistic performances were already priced in. The whisper numbers are particularly higher than the analysts’ expectations this quarter. For stocks to fall like in 2000, firms must start missing estimates. I don’t see that happening because the weak dollar will be a tailwind for multinational firms. It’s not like stocks already priced in tax cuts and they didn’t occur. The market has lowered its implied chance tax cuts will be passed without missing a beat.

Conclusion

We don’t even know what the taper and unwind will do to stocks. Adding to that uncertainty is what the SNB will do. This only makes the next 12 months of trading even more interesting. I think America could step in and stop the SNB from manipulating the stock market if it wanted to. The issue is no one has a problem when assets are manipulated higher, but then when the manipulation pushes assets lower, people get mad. If the SNB decided to sell some of it stocks like the Fed, it would put extra pressure on equities.