The latest statement by Paul Ryan, the Speaker of the House, was that tax reform could take longer to get done than healthcare reform. That’s an interesting way of putting it since healthcare reform still hasn’t gotten done. The first step of healthcare reform, which is voting on it in the House, wasn’t even completed. Paul Ryan stated that neither the Senate nor the President have completed a budget. As per usual, government isn’t functioning as quickly as the private sector. That’s not a political point because some would argue we don’t want government to pass important laws quickly. The point is that it was never a good idea to buy stocks based on the hope of fiscal stimulus before Trump was inaugurated. Usually the market likes to get ahead of results, but with government actions, caution is a better approach.

The members of the Fed who pushed the expectation of stimulus back to 2018 look to be correct in their assessment. I was wondering how the Fed would react to such a delay. It seems that it’s not affecting their outlook on rates yet. Once sentiment surveys weaken because of the lack of fiscal policy actions, the Fed will likely alter its tune. It’s possible that the stimulus plan may end up being crafted to get the economy out of the next recession.

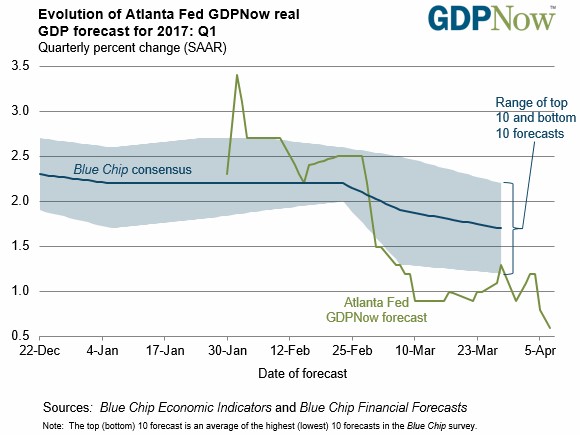

One argument that the next recession is coming soon comes from the Atlanta Fed’s GDP Now Forecast. The GDP Now forecast was revised lower by 0.6% in the last update. It’s now showing 0.6% growth expected in Q1. The NY Fed’s model is still differing as it expects 2.8% growth. As you can see in the chart below, the blue-chip consensus estimate is exactly in the middle of these two as it’s at 1.7% growth. There were a few reasons why the Atlanta Fed’s estimate was lowered. The ones I’ve previously covered were the weaker than expected BLS and ISM reports.

The reports I haven’t discussed which also contributed to the lower estimate were the light weight vehicle sales report and the wholesale trade data. All four of these reports caused the consumer spending growth estimate to fall from 1.2% to 0.6%. The estimate for real nonresidential equipment investment growth fell even further as it dropped from 9.7% to 5.6%. There is a chance that bullish investors are going to be able to support their narrative by blaming the bad weather in March. However, that would be biased analysis because the warm January and February helped growth. It wouldn’t be the first time a weak report was ignored as this has been the weakest recovery since 1949, yet the stock market is in its second longest bull market ever.

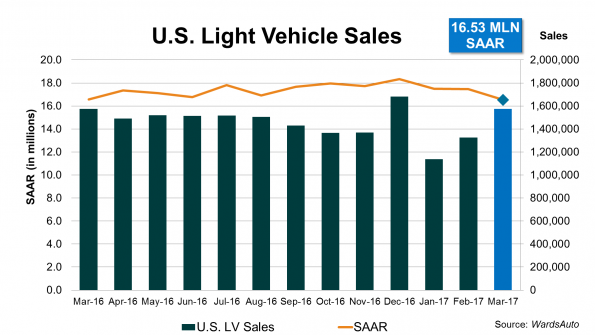

As I mentioned, the weaker than expected U.S. lightweight vehicle sales growth caused the drawdown in GDP expectations. Car sales have declined on a year over year basis for three months in a row. I expect this weakness to continue as the auto loan bubble bursts this year. The chart below shows the seasonally adjusted annual rate of sales was 16.53 million. This was the weakest sales rate since October 2014. One of the reasons for the weakness in sales is because the 13% incentive rate was below expectations. It’s also become tougher to get a car loan. That constriction in lending is only getting started as the labor market is still strong. Weakness in the labor market will further crimp auto loans which will hurt sales. This sales weakness is leading to a pile up of inventory which will hurt the auto firms’ profitability.

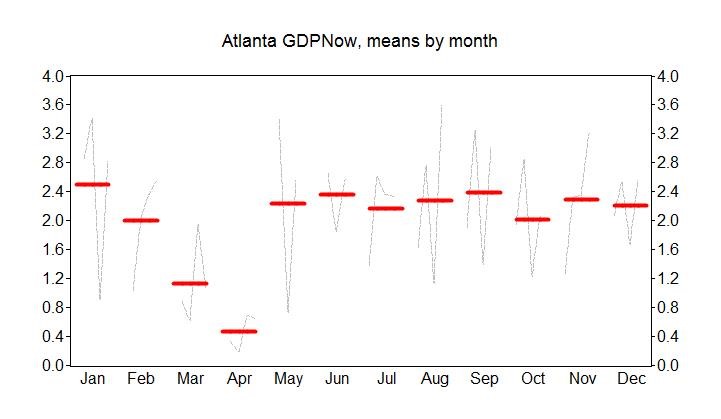

There is no counterpoint to the claim that these four data points, which caused the GDP Now forecast to move lower, were weaker than anticipated. However, the GDP Now forecast is much more than those four data points. Its decision on how it weights each report determines its output. The root mean squared forecast error is 1.17% at this point in the quarter. The chart below provides evidence that the model may have seasonal adjustment issues. This is particularly noteworthy now because the estimates are the lowest in April compared to the rest of the year. This doesn’t mean the model is too low this time, but it is food for thought.

The final point I will make is that despite the weakness in the data this week, stocks are only about 2% off their all-time high. It feels like nothing can crack this market. Bearing Asset Management described short sellers as living in the last of Dante’s circle of hell. I would argue that being net short has not only become difficult, it has become impossible. In the past few years, many have tried and failed to short the market based on weak fundamentals and valuations. The only way I know how to do analysis is to look at the economic reports, earnings reports, fiscal policy, and monetary policy, but I acknowledge it hasn’t worked.

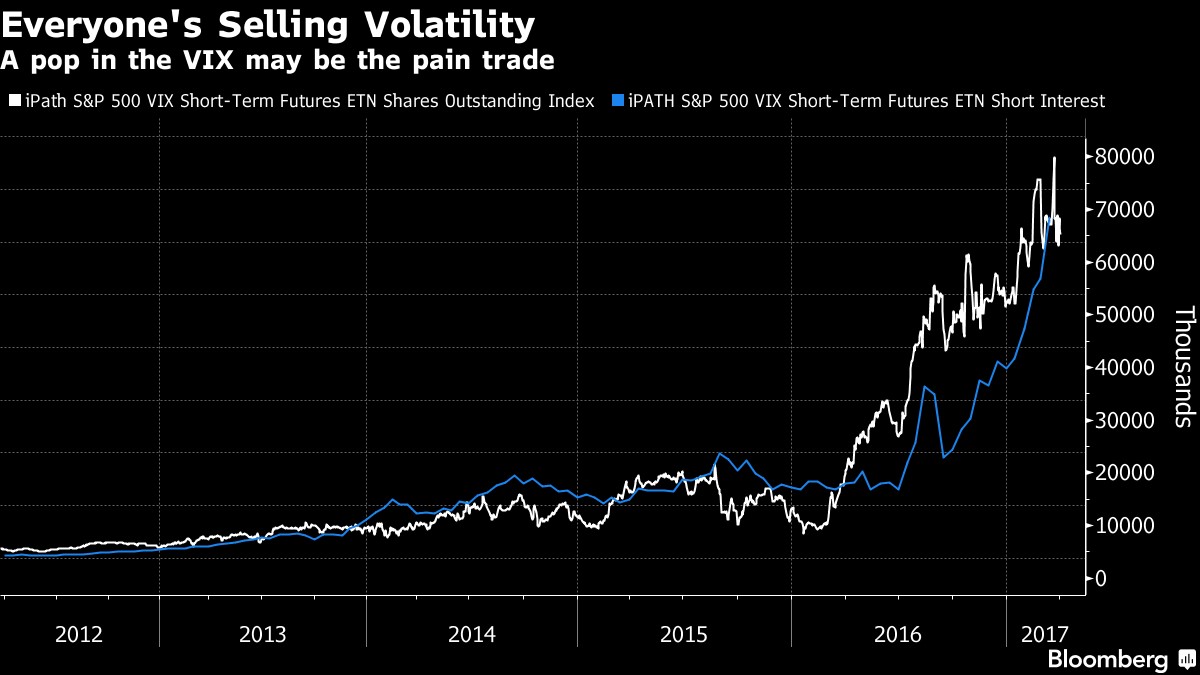

The chart below summarizes my point. It has become a very popular position to sell the VIX. Eventually the traders who are picking up pennies in from of the oncoming train will get run over, but for now it looks great as the profits keep rolling in.

Conclusion

The economic data has weakened for the month of March partially because of the winter storm. This weakness must continue in April to stop the stock market from rallying to new heights. However, it appears an outright recession is needed to catalyze a correction. Although the Atlanta Fed is projecting 0.6% growth, I highly doubt a negative print will occur because the April numbers tend to be too negative. I’m expecting to see growth of between 1.0% and 1.5% because the growth the survey data is showing is not being met with strong growth in new orders and domestic investment. The bankruptcies in retail also will hurt the growth rate. Retailers don’t go bankrupt at a high rate when the economy is strong. The advanced estimate for GDP growth will be released on April 28th which is in three weeks.