Stocks Recover - After Modest Fall

The stock market opened higher before plummeting in the late morning and recovering in the afternoon. From the peak early in the morning to the trough later in the day, the S&P 500 fell 1.72%. It felt like the market would finally roll over.

Traders on Twitter were gearing up for the bears to take control. However, the S&P 500 rallied 0.9% into the close to end the day only down 0.39%.

Some traders claimed weak economic data caused the big plummet in the morning, but I disagree because only the December construction spending report and the February motor vehicle sales reports came out.

They weren’t good. But I think the main reason stocks fell is because they are way overbought. The CNN fear and greed index started the day at 72 and closed at 66 which is still greed.

Don’t get me wrong, economic growth is still slowing. However, I don’t think those two reports could catalyze anyone to change their viewpoint on the economy.

Stocks Recover - ‘Risk On’ & ‘Risk Off’ Trades Are Real

Nasdaq was down 0.23% and Russell 2000 was down 0.89%.

Worst 2 sectors on Monday were healthcare and the financials which fell 1.34% and 0.62%. Best 2 sectors were materials and real estate which increased 0.44% and 0.41%. Utilities were up 0.21% because the ‘risk off’ trade took hold.

Not everyone agrees that the ‘risk on’ and ‘risk off’ trades are real. The argument against them is that each asset is priced based on a myriad of different factors. They say there is no way the market can act so simply.

There is no doubt, pricing assets is complex. However, the correlations hold. I follow what the market tells me.

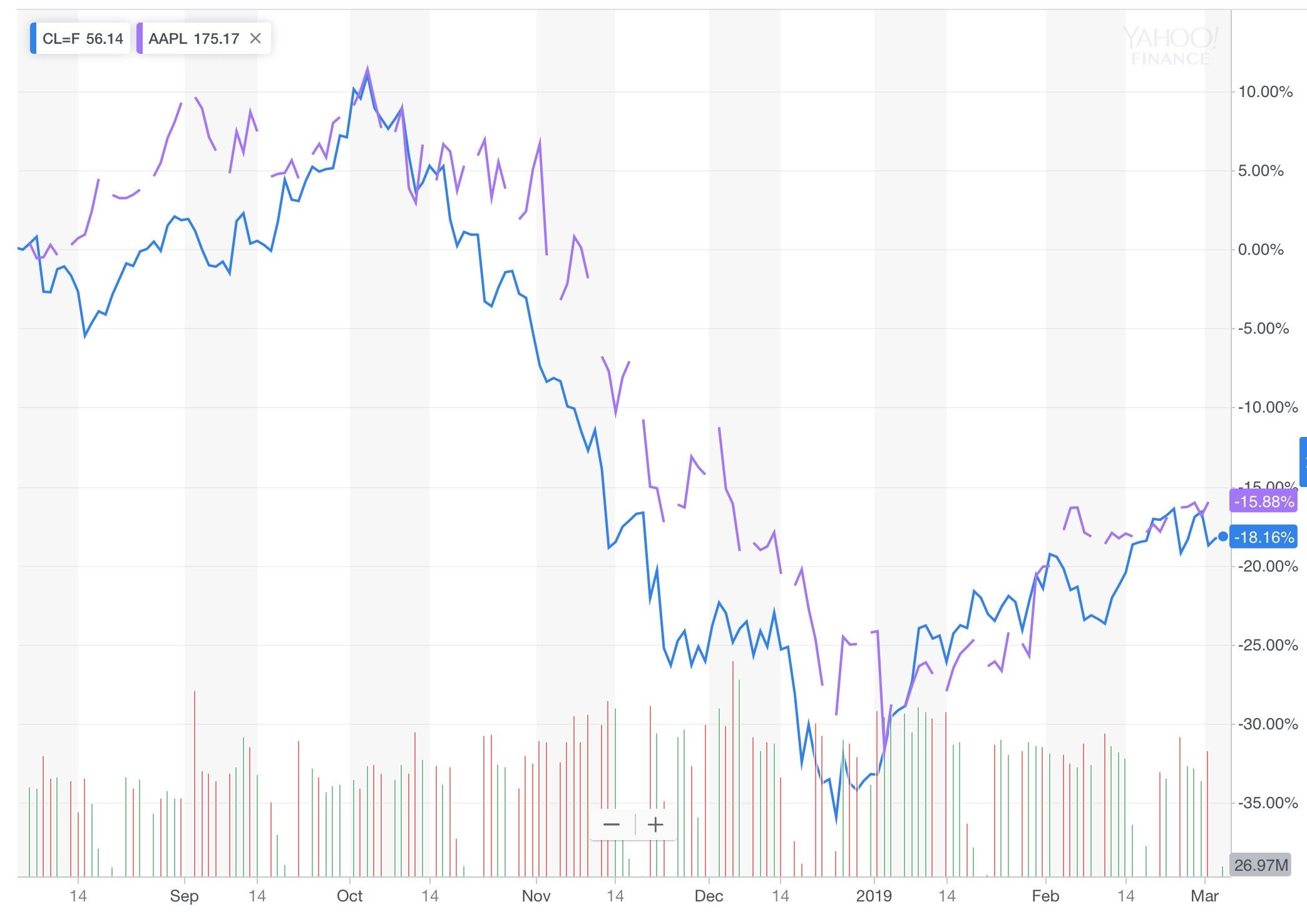

As you can see from the chart below, oil futures and Apple stock have been very highly correlated in the past 6 months.

Oil has been correlated with stocks this entire cycle. Low oil prices hurt the manufacturing sector and signal the economy is weak because demand is weak. High prices signal demand is strong. Eventually, when oil gets too high, inflation becomes a problem.

Stocks Recover - Boeing Dominates The Dow

The Dow’s total return to start the year is the best since at least 1987. The market doesn’t need an excuse to have a modest pullback.

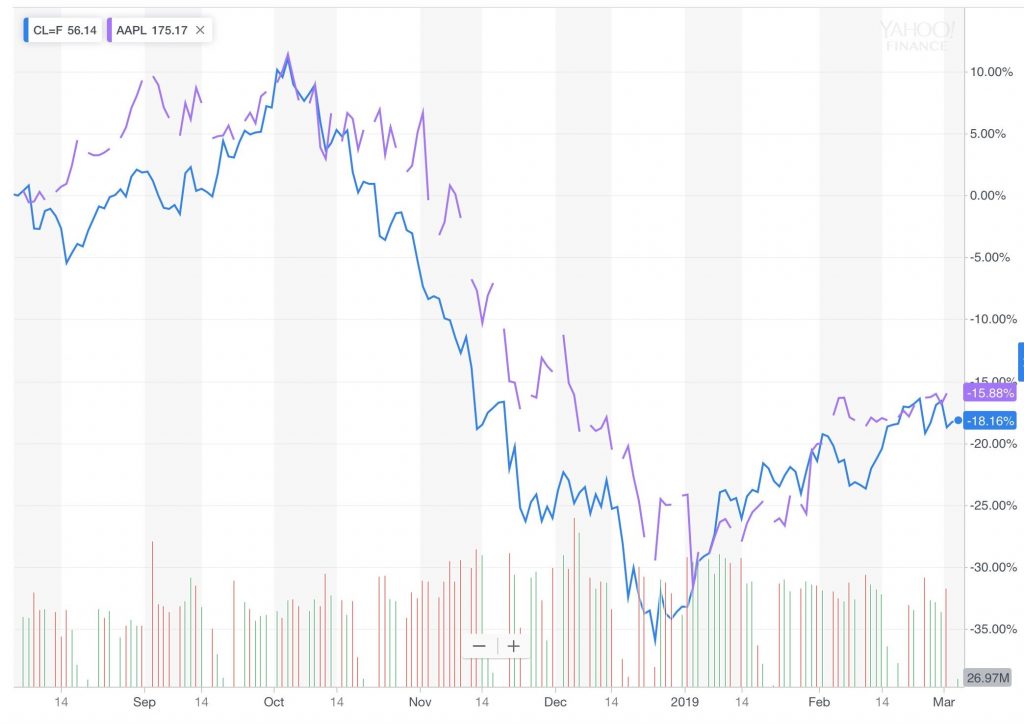

Boeing is controlling the Dow just like how the big internet names control the Nasdaq and S&P 500. The Dow is price weighted, so Boeing’s $433 price per share has a big influence on it.

As you can see from the chart below, up until March 1st, Boeing caused the Dow to increase 812 points which is 30% of the gains. Boeing’s rally to start the year is the best for any Dow stock since Microsoft in 2001. Interestingly, Boeing’s 1.76% decline on Monday was in tune with the Dow’s decline.

Stocks Recover - Biggest VIX Decline Ever

On Monday, the VIX increased 7.81% to 14.63 because of the decline in the morning. However, the VIX had a historic decline in the first 2 months of the year.

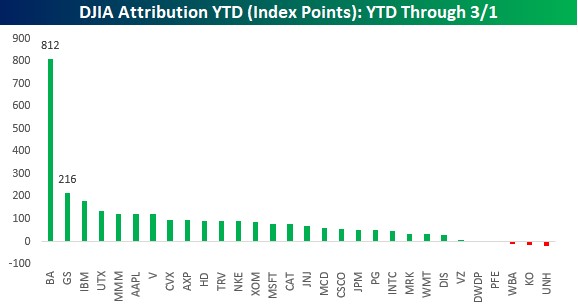

As you can see in the table below, in the past 10 weeks, the VIX fell 54.9% which was the largest decline ever.

This was larger than the 53.5% decline after Brexit. VIX went from being in the 93rd percentile to the 25th percentile of historical readings. This has been one of the quickest snapback rallies ever which is why the VIX has had its quickest drop.

We will be able to rank this snapback rally after it passes the September record high. Theoretically, we are still in a bear market.

Stocks Recover - Consumer Confidence Rebound Moderates

Preliminary University of Michigan consumer confidence reading showed a sharp increase in February. Mostly because the government shutdown ended.

However, the final reading was lower than the preliminary index. Specifically, the index was up 2.6 points from January to 93.8. However, it fell from the mid-month flash reading of 95.5.

Current conditions index was 108.5 which is 8 points from the December level. Expectations index was 84.4 which is almost 3 points from the December reading. It’s not a surprise expectations got back to where they were quicker.

1 year inflation estimates fell 0.1% to 2.6% and 5 year inflation estimates fell 0.3% to 2.3%. This is in line with the decline in the ISM prices index. Inflation isn’t a problem anymore.

Fed won’t hike rates in March, nor will they hike the rest of the year. There is now a 98.7% chance the Fed doesn’t hike in March and 92.8% chance the Fed does nothing by the end of the year.

As you can see from the chart below, the index of households’ financial situation compared to a year ago fell.

That means only a net 6% have had their financial situation improve in the past year. Since real wage growth has accelerated and the labor market is still strong, I think this index is too pessimistic.

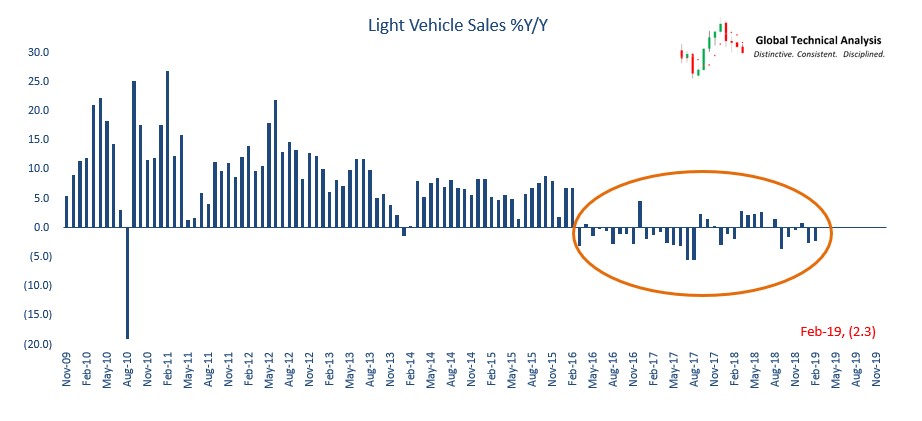

Stocks Recover - Weak Motor Vehicle Sales Report

As I mentioned earlier, the February motor vehicle sales report was weak. Total vehicle sales were 16.5 million which missed estimates for 16.9 million and the low end of the estimate range which was 16.7 million.

As you can see from the chart below, light vehicle sales were down 2.3% year over year. Sales were revised 0.1 million higher to 16.7 million in January which is below the 2018 average of 17.2 million. Domestic sales fell from 12.9 million in January to 12.7 million in February.

Stocks Recover - Conclusion

Stocks took a breather after rallying relentlessly this year. Personally, I don’t think that the S&P 500 falling below the 2,800 level is a death knell for the stock market. I also don’t think the stock market will sell off after a trade deal is announced.

Many investors, including myself don’t see a massive rally either. Something that is priced in shouldn’t cause a reaction.

The economy continues to prove the slowdown isn’t over as evidenced by the weak motor vehicle sales report. Consistent sales growth stopped in early 2016.