Stocks Rally - Big Monday Rally

There are often big rallies within corrections and bear markets. Monday was an example of this as tech led the market higher.

S&P 500 was up 1.55%, Nasdaq was up 2.06%, and Russell 2000 was up 1.16%. This was an oversold rally as the CNN fear and greed index increased from 9 to 17. It still signals “extreme fear” as it has for most of the past 6 weeks.

One more rally will get it out of the “extreme fear” category. VIX fell 12.17% to 18.90.

Personally, I don’t think stocks are an automatic buy when this index shows “extreme fear”. This business cycle is near its end. I see almost no risk of a recession in the next 6 months. But there should be a recession in the next 1-2 years.

There isn’t much upside in the near term. And there’s a lot of potential downside in the intermediate term. My outlook can change if stocks fall. But it’s not going to change because of a 10% decline from the all-time high.

Stocks Rally - Potential Bad News: Trade

Even though the stock market increased on Monday, great news didn’t come out. In fact, a couple of negative headlines came out.

The first was that President Trump stated it was “highly unlikely” that he would delay the proposed increase in tariffs on China on January 1st. Furthermore, he suggested he could put a 10% tariff on iPhones and laptops imported from China. These statements came 4 days before the summit with President Xi.

On face value, these statements aren’t good because obviously we don’t want to see additional tariffs. We want them all eliminated.

The question is if he is posturing or really believes there won’t be an imminent deal. There are two possibilities which aren’t terrible.

First is that President Trump is acting like he needs an amazing proposal to make the American public believe the deal he makes is great. That would mean a deal is close.

The second possibility is President Trump is trying to get President Xi to change his proposition. It could also be both as Trump wants the American public to like the deal. And he wants Xi to improve his offer.

Personally, I don’t expect a deal to be made in the next week. But there may be positive reports after this summit. Both sides need a deal.

The tariffs aren’t the catalyst for the weakness in China and America. But they will make bad situations worse in 2019. Since China is doing a stimulus next year, you would think the country would be highly motivated to make a deal. It wants growth to improve.

And U.S. economic growth is starting to slow. Meaning, America also should be motivated to make a deal. We should expect a deal by Q1 2019.

Stocks Rally - Other Bad News: GM Layoffs

The second bad news event that came out was that GM announced layoffs of 14,700 workers to cut costs. Generally, auto firms don’t start firing workers when the economy is great. This will impact 8% of GM’s workers.

As you can see from the table below, it will impact workers in Detroit, Ohio, Maryland, and Canada. This is the 7th largest round of job cuts in the auto industry since 2001.

As you can see, the others on this list were leading up to recessions, during recessions, or right after recessions. GM stock increased 4.79% on the news. Vut it has underperformed this year as it is down 9.93%. Ford stock is doing even worse as it is down 25.75% year to date.

These layoffs by GM will cause jobless claims to spike further. This is another sign the labor market is about to weaken. I am highlighting these layoffs because they are the beginning of the end of this expansion.

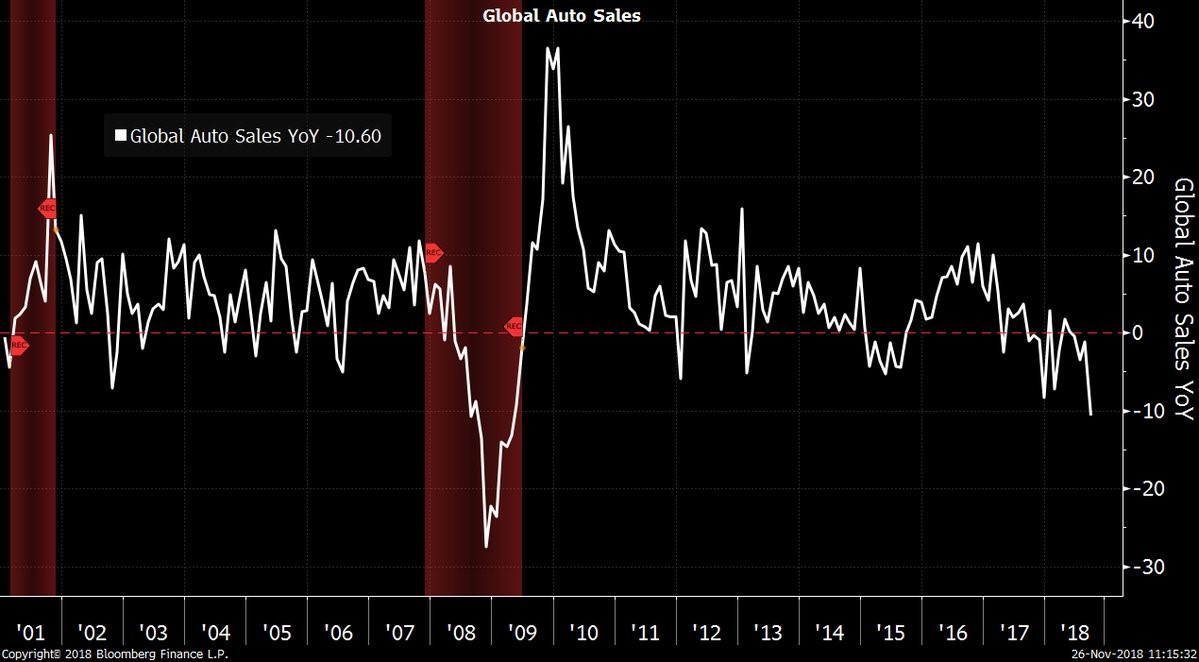

As you can see in the chart below, global auto sales are down 10.6% year over year. That’s the worst decline since the financial crisis. If vehicle sales weaken in America next year, that will increase the velocity of the slowdown.

Stocks Rally - Big Tech Stocks Outperform

Momentum tech stocks rallied while consumer staples underperformed. For example, Facebook stock increased 3.53% and General Mills fell 2.28%. Unfortunately for the FAANG names, I think this is a temporary bounce.

There isn’t concrete evidence of a recession, so we probably aren’t going to have a huge crash in the near term. That means these momentum names will have a few oversold bounces before the worst part of this potential bear market starts.

Best sectors on Monday were technology and consumer discretionary which increased 2.25% and 2.59%. Worst sectors were real estate and consumer staples which increased 0.20% and 0.04%.

Stocks Rally - The Coming Yield Curve Inversion

The yield curve has been steady in the past few weeks. And the difference between the 10 year yield and 2 year yield is 24 basis points. I think the Fed is about to finally invert the curve. Its rate hikes will increase short maturity treasury yields. Also, slowing growth will decrease long maturity treasury yields.

Despite the current slowdown, there is a 79.2% chance of a hike in December. The data suggests the Fed shouldn’t hike rates. But the Fed’s hawkish reaction to the economy suggests the Fed will hike into a slowdown. I may have been wrong to suggest if stocks fall below their recent low, the Fed won’t hike rates.

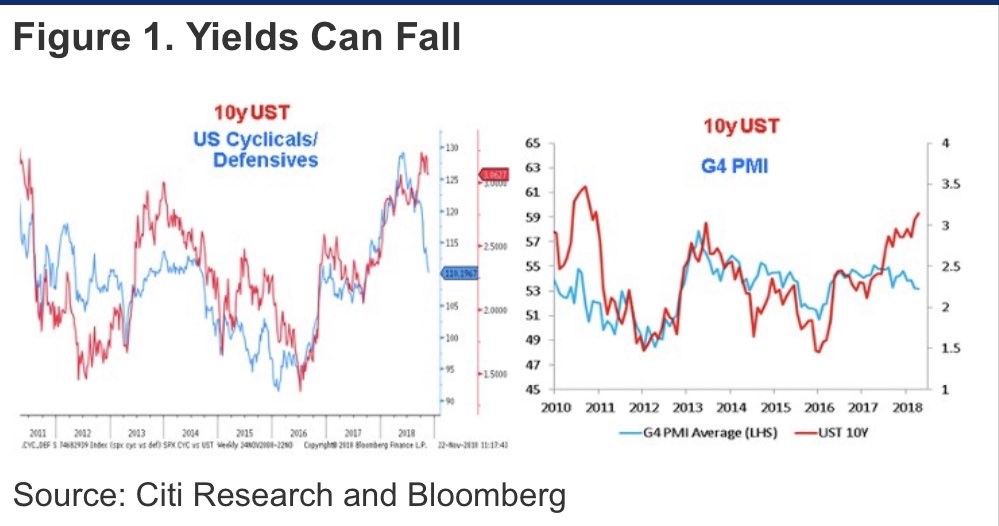

As you can see from the chart on the left, the ratio between cyclicals and defensive stocks suggests the 10 year yield will fall.

The curve could invert if the 10 year yield falls below 3%. The chart on the right shows the 10 year yield should also fall based on the recent decline in the G4 PMI average.

Breakeven inflation rate has been driving the 10 year yield lower. But the burst in real yields has prevented it from falling below 3%.