Crazy Day On Wall Street

2018 has been nothing like 2017 as the market has whipsawed in the past few days. The Dow ended up 2.33% and the S&P 500 was up 1.74%. The S&P 500 was down to 2,624 at the lows and closed at 2,695. The Dow had a 1,167 point trading range. The Dow rose at least 2% and fell at least 2% from the previous close for the first time since December 5th, 2008. The VIX collapsed down 20.04% to 29.84. When the VIX was at 37 yesterday, it implied a 2% move everyday for the next month. Interestingly, after the short volatility trades were blown out last night, the long volatility trades fell today. The XIV will be closed by Credit Suisse on February 21st. Google shows it was down 72.58% on Tuesday to $7.35. The SVXY was down 82.79% to $12.24. The total blow up of these ETNs cost investors almost $3 billion.

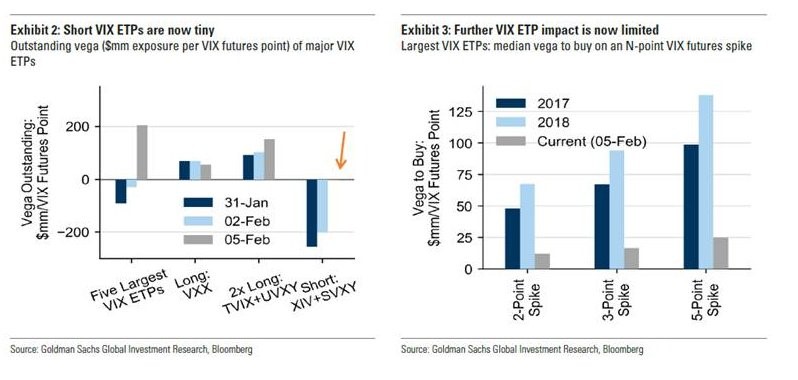

The charts below show the outstanding exposure per VIX futures point of the major VIX ETPs. As you can see, the exposure has been eliminated. It appears the effect on the market is over. Many were worried on Monday night about a crash in the market because the futures indicated the Dow would fall 1,200 points. The market opened down less than that and recovered in an up and down fashion. Some participants believe this was the stock market searching for and finding a short term bottom. On Monday night, I was short term bullish on stocks which paid off quicker than I expected. I’m now more neutral because of this huge rebound. I’m guessing the VIX will fall in the next few days as normalcy returns.

The rising interest rates will be a problem down the road, but won’t cause a crash like we saw in the past few days. This crash was more like the flash crash than the previous fundamental corrections and bear markets. It’s amazing to see asset prices fluctuate so quickly on no news. It’s unfortunate that many brokerage firms like Fidelity have had intermittent outages recently. There was no reason to panic. You should have raised cash in January when the market was going up in a straight line.

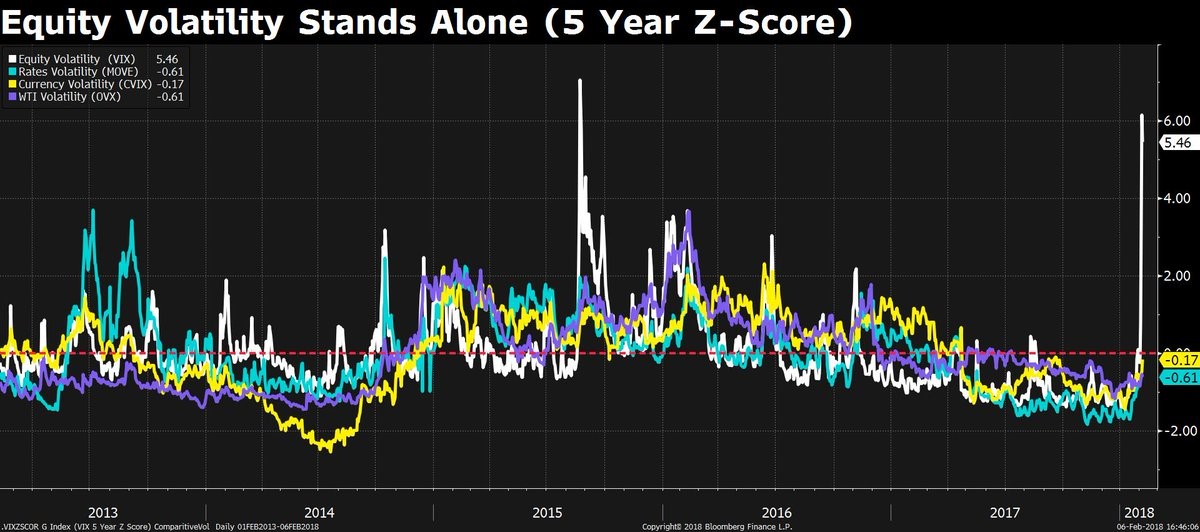

The chart below shows the volatility in the stock market didn’t impact the other markets. As you can see, the VIX skyrocketed while the rates, currency, and oil volatility stayed in place. If this was a correction driven by fundamentals, they’d be moving in tandem.

Government Won’t Shut Down

It looks like Senate minority leader Chuck Schumer and Senate majority leader Mitch McConnell are very close to coming to an agreement to prevent a government shutdown which would occur on Thursday if nothing is done. They are working on a 2 year deal. The House GOP appropriators unveiled a short term continuing resolution which would fund the military at increased levels until September 30th. The rest of the government would operate under 2017 level spending until March 23rd. This plan doesn’t include a solution to DACA which is being worked on separately. I will be updating readers on the latest movements of these proceedings this week. Even though Trump said he’d love to shut down the government if the Democrats don’t agree with his immigration plan, the deal without immigration will likely proceed. Stocks should appreciate this news. This could have ended badly this week if no deal was made. The market didn’t need another thing to worry about after the recent crazy action.

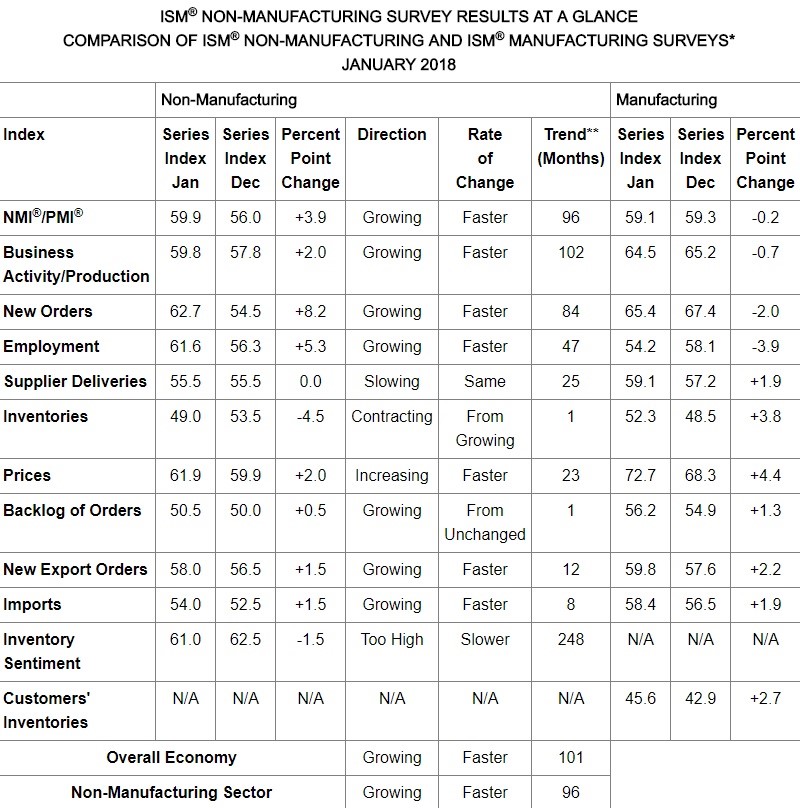

Very Good ISM Report & Not So Good Markit Report

On the same day, the Markit services PMI was disappointing while the ISM services PMI was good. This makes figuring out where the economy is going difficult. One thing that was not difficult was realizing the 5.4% estimate for Q1 GDP by the Atlanta Fed was ridiculous. It came back down to reality today as the estimate fell to 4%. Getting back to the services sector, the Markit PMI fell from 53.7 to 53.3. This was the weakest report since April 2017. On the bright side, the new business index increased to the highest point since September 2017 and the backlog index increased to the highest point since March 2015. The overall PMI is consistent with 2.0%-2.5% GDP growth in 2018. That is probably going to be slightly too pessimistic, but it’s too early to tell where GDP growth will end up. We don’t even know for sure how quick the economy grew in Q4 2017.

On the other hand, the ISM services report was great. The PMI was 59.9 which was 3.9 points above last month and 2.7 points above the 12 month average. It was the highest report in at least the past 12 months. As you can see from the table below, every segment is accelerating except inventory sentiment and supplier deliveries. The all important new orders index was up 8.2 points which shows the economy is on a tear and will likely continue. The price index was up 2 points, further signaling core inflation is about to increase above 2% this year. This report is consistent with a 4% GDP growth rate. I think the actual result will be in between what the Markit and ISM reports have shown.

An information company said, "Executive management [is] excited about tax breaks for CapEx purchases in [the] new tax bill." This supports the notion that GDP growth in 2018 will be the highest of this expansion as companies invest in their businesses. A public administration company said, "Business activity is low due to the continued partial funding [of] bills passed (continuing resolutions)." This challenge looks like might be fixed this week. Congressional members are tired of funding the government for a few weeks. The lack of a shut down is a step in the right direction. If there is bipartisan agreement on immigration and this latest continuing resolution, I don’t see why a long term plan on the budget can’t be agreed upon. This affects a small segment of the economy, but it’s still important to have a somewhat functioning government for obvious reasons.