The biggest question investors focused on earnings are trying to answer is how the gap between small cap and large cap firms’ margins will be closed. Either large cap firms will have their margins fall off the peak or small cap firms will see their margins rise to the 2013 peak. It’s possible that the gap can stay large, but the trend in small cap margins has been down which is an unsuitable divergence. Eventually that will impact larger firms because when the small ones begin to lay-off workers that will hurt the consumer. Layoffs from smaller firms also increases the slack in the labor force which can allow larger firms to give their employees smaller raises. While that’s a possibility, the economy would erode which would hurt more than the dampening wage inflation helps. Recessions still have large impacts on profits even though wage inflation is lowered. At the least, if you’re bullish on the earnings growth, you must expect small cap margins to stabilize.

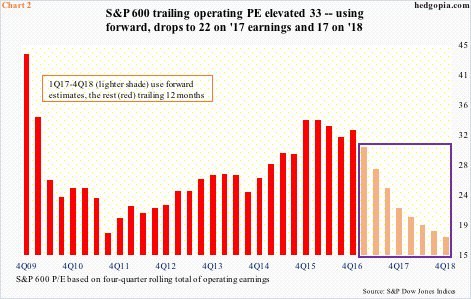

The consensus clearly believes small cap margins will rebound. As you can see from the chart below, the S&P 600’s trailing operating PE is at 33. Remember, operating earnings excludes taxes and interest, so the real price to earnings multiple is higher. When you move out to the future the price to earnings multiple drops to 22 using 2017 forward earnings and falls to 17 using 2018 earnings estimates. This price to earnings multiple falls to around the same level it was at in 2011 which is when earnings started to rise following the recession, but stocks hadn’t caught up with the improvements. That was a great time to buy stocks.

This brings the difference in opinions to the forefront. Even though trailing earnings are high, bulls believe now could be one of the best times to ever hold stocks. The high earnings estimates check the bear thesis that stocks are expensive. It’s true that estimates are usually cut before the reporting period, but the bulls will point to the current quarter’s growth rate as a signal that the negative earnings drift has ended.

This difference in opinions won’t be resolved by doing the math on valuations. Everyone is aware that trailing multiples are high, so it won’t be the catalyst for a correction. The question is where the business cycle is headed in the future. If earnings can rebound, stocks might be cheap. By the time you realize stocks were cheap, they will have already rallied. In attempt to figure out where earnings are headed, let’s look at the restaurant sector’s March summary from Black Box intelligence.

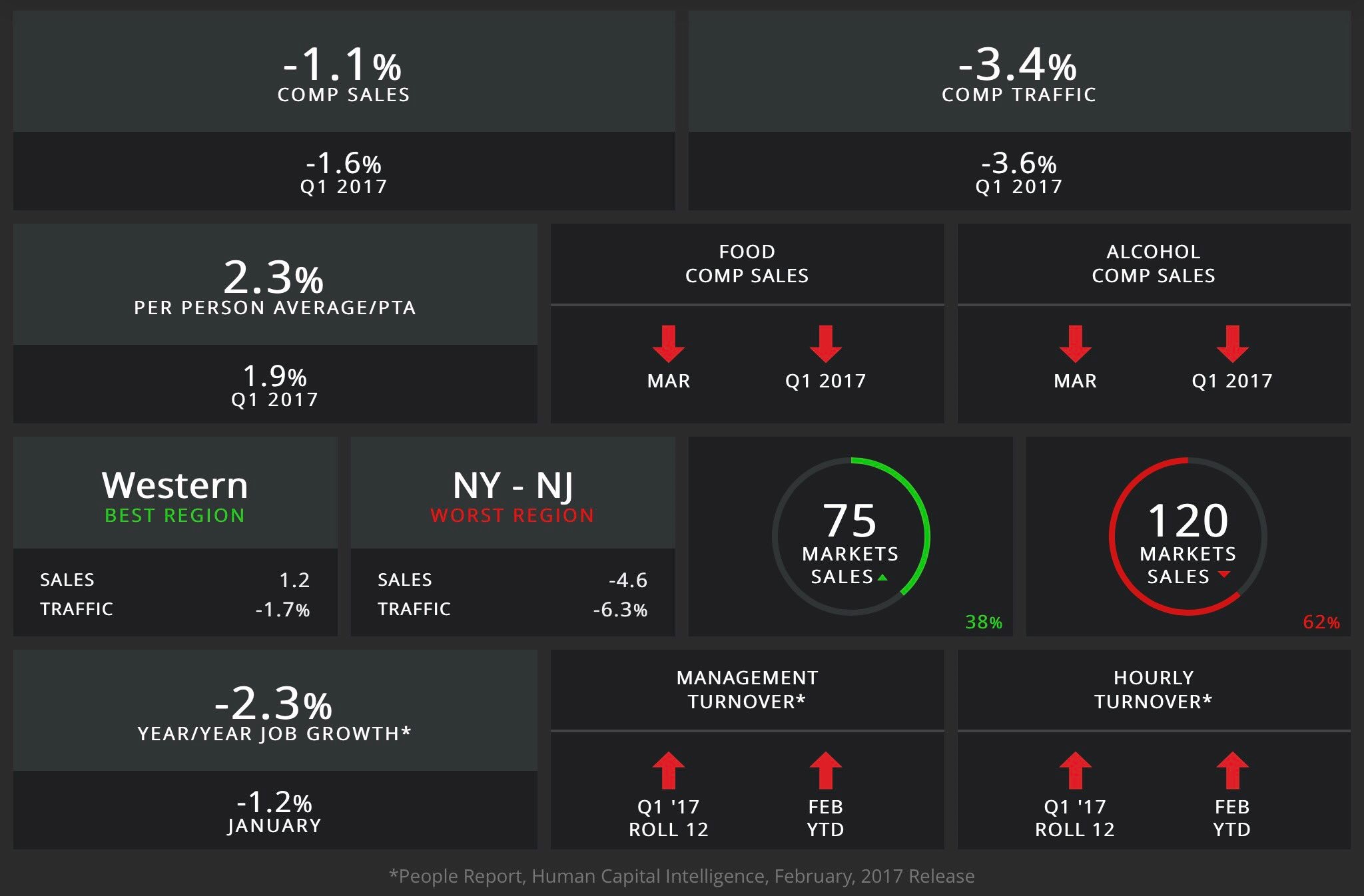

As you can see from the image below, Q1 was awful as sales fell 1.6% and traffic fell 3.6%. The March numbers were slightly better than the quarter’s results, but -1.1% sales comps and -3.4% traffic comps don’t provide much hope for a turnaround. Both food and alcohol were down. The one silver lining of this report is that the weakness seen in New York and New Jersey was caused by the weather. A winter storm is likely to show up in traffic declines more than sales since customers can’t travel to the restaurants during the storm. That’s what we see in the data as sales fell 4.6% and traffic fell 6.3% in March. It’s amazing to see that the best region (Western) had a 1.7% decline in traffic. That shows broad based weakness.

The restaurant sector weakness is significant for two reasons. The first is that restaurant sales act as a good indicator for the health of the consumer. Actual sales results matter much more than the inaccurate consumer sentiment surveys which are showing strength when there is none. It’s possible for a consumer to misrepresent his/her optimism level in a survey, but it’s not possible to spend disposable income that they don’t have at restaurants. That’s why restaurant sales are weak. In terms of secular trends, restaurants are riding a positive wave because consumers want to pay for experiences. Consumers are shirking brick and mortar retail because the shopping experience is better online. They feel restaurants offer the experience that makes it worth spending extra money opposed to making food at home. The fact that this secular trend isn’t enough to help restaurants tells you how weak the consumer is.

The jobs market is the second most important aspect of why this weakness is significant. Waiter and bartender jobs have been the fastest growing employment category in this recovery which is partially caused by the fact that many workers are taking on multiple jobs. Employee turnover is skyrocketing because the labor market is tightening and because if a worker has multiple jobs it’s easy to switch one of his/her jobs. 80% of restaurants had to offer higher base pay to attract workers. This increased pay is partially responsible for the -2.3% year over year job growth in February. 60% of restaurants had lower employee counts. The other factor is that restaurant openings are slowing.

The one place in the economy which may be feeling the effects of a tight employment market is the restaurant industry. That’s bad news because the one place where employees could count on a raise is slowing its job growth. It’s not surprising that different industries have different labor market slack. That’s what makes monetary and fiscal policy tough to gauge. There is no correct answer on where interest rates should be because the economy is dynamic. The weak hourly wage growth may be causing restaurant sales to slow. The good times for restaurant employees may be ending as the industry gets sucked down by overall economic weakness.

Conclusion

Analysts are expecting a rebound in small cap margins. That optimism must be supported by a strong economy or the estimates will have to come down. The weakness in the restaurant industry makes it seem like economic weakness is more likely than strength in the next few quarters. This is only one indicator so it must be taken with a grain of salt. However, the fact that the fastest area of employment growth is slowing is a red flag which can’t be ignored.