Stocks - Another Day With Wild Swings

Wild swings in the stock market where big losses turn into gains aren’t necessarily positive. They signal the heightened volatility environment is continuing rather than that stocks are ready to rally.

Monday was another day with big swings as the S&P 500 fell 1.83% in the morning before rallying to close up 0.18%. This is a hugely important technical level.

The low on the day was about 4 points above the February closing low this year. Since stocks closed up, they also didn’t break the November low.

Nasdaq rallied 0.74% and Russell 2000 fell 0.34%. Microsoft and Facebook were up 2.6% and 3.2%. VIX fell 2.54% to 22.64. CNN fear and greed index fell from 11 to 9.

This index tells traders to buy stocks when it is in the single digits in this new market where volatility reigns supreme. This index hit 8 earlier in the day, making it a great signal to buy stocks during the morning for a trade.

The next big news event which will move markets is the Fed meeting next Wednesday.

Stocks - Big Internet Rallies While The Financials & Energy Fall

Tech and communication services were the winners on the day as they increased 1.43% and 0.75%.

I wouldn’t use this outperformance as a reason to buy the big internet names for a trade. The worst sectors were energy and the financials which fell 1.62% and 1.4%. Energy fell because oil prices fell 3.1% to $51. The oil market closes at 2:30 PM.

Since the stock market rallied in the afternoon, the close cut off a potential recovery in oil prices. Oil traders are still worried about the slowdown in global growth.

Oil might rally next year because of the Saudi and Canadian cuts. Saudis are cutting 900,000 barrels per day. A big uncertainty is on the demand side.

Weakness in the financials explains the decline in the Russell 2000 as it has a lot of banks. KBW regional bank index fell 1.97%. Banks are hurt by the flattening yield curve, declining rates, and the economic slowdown.

Stocks - Fed Still Expected To Hike Next Week

S&P 500 flirted with the level I said the Fed might back off from its December hike. But it never closed below that level.

The 10 year yield is at 2.85% and the 2 year yield is at 2.72%, meaning the gap between the two is 13 basis points. The yield curve has been catalyzing equity volatility.

If the curve inverts in the next few weeks, I wouldn’t be surprised to see the S&P 500 break the February lows. A low 10 year yield shows us that despite the rally off the lows in stocks, investors still aren’t optimistic about the 2019 economy.

Chance of a rate hike on December 19th is 73.2%. This will be a 20 basis point hike because rates are too close to the top end of the Fed’s range.

The big uncertainty is about 2019 guidance. I expect the Fed to suggest there won’t be any rate hikes in the beginning of 2019. But that it wants 1-2 hikes by the end of the year. I don’t think it will follow through on that guidance.

The Fed can’t go from saying there will be 3 hikes to 0 hikes in a few months. That’s too rapid of a change. It would cause uncertainty.

Stocks - Valuations Have Become Cheap

The stock market is at a very interesting point because it is falling while the expansion will likely continue for over one year.

Usually, you don’t see stocks fall sharply outside of a recession. Plus, strong earnings growth has brought down PE multiples.

If you’re bearish on stocks, you need to be very certain economic weakness is coming. If it isn’t, stocks will soar higher because they have gotten so much cheaper this year.

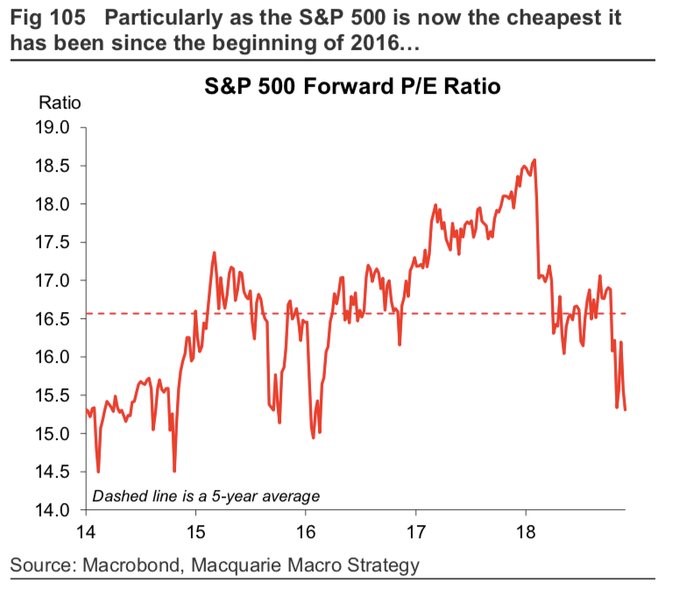

As you can see from the chart below, the S&P 500’s forward PE ratio has fallen to the lowest point since early 2016.

It is way below its 5 year average. Valuations at the peak in late 2017 looked like a market peak, but it’s tough to compare it to previous peaks.

One of the reasons multiples were high is because some traders speculated taxes would be cut. Therefore, it’s like that peak wasn’t real. It would be like if stocks fell as tax increases were discussed.

Stocks wouldn’t be cheap because earnings would be about to fall.

This analysis of the S&P 500’s forward PE multiple has nothing to do with the economic cycle.

Stocks - It is about how stocks will react to various economic outcomes.

If earnings growth slows to the mid-single digits in 2019, there’s little reason to sell stocks. I had been pessimistic on 2019’s performance assuming stocks would rally between 5% and 10% this year.

If stocks crater in the last two weeks of December, I can’t be as bearish as I was previously.

It seems odd to be bullish heading into a recession, but at a certain price I would be more optimistic. This is why economic forecasts are a tool rather than something you can blindly follow.

You can’t just follow averages. I have seen many interviews in the financial media where the interviewer asks the guest what will happen to stocks and the economy when the yield curve inverts.

The respondent gives the historical average results. Those are only a guide, not something you should bet on.

Stocks - Conclusion

The CNN fear and greed index being in the single digits gives us a bullish short term projection. Technicals will lead the way in the next few days. There is a lot of support at these levels because the market has bounced off the February low so many times.

The Fed’s decision on rate hikes and future dot plots will determine how stocks end the year. It’s the most important Fed meeting in years.