Fiscal Stimulus On The Docket

On the day before the ADP report, we got another update on the consumer. By the way, the current estimate for September job growth in the Friday BLS report is 900,000. Investors moderately concerned this estimate is too high, but there will be over 600,000 jobs added.

Moving on to the consumer, RedBook same store sales growth rebounded as it was 2.2% which was a 0.7% increase from the prior week. This data is from September 26th which is the last week of the month. It's not surprising that we are seeing better spending growth because the labor market is healing and consumer confidence is up.

A big potential negative catalyst is COVID-19 cases increasing materially. And a big potential positive catalyst is a fiscal stimulus. House Democrats unveiled their fiscal stimulus package which is $2.2 trillion ($200 billion less than the last estimate). It includes another round of $1,200 checks which would be huge.

As more people get their jobs back, higher unemployment benefits have less of an impact. Plus, these checks are set to go out to more people. $500 will go to adult dependents and full-time students younger than 24.

Their plan also calls for $600 in weekly unemployment benefits through January. This exact plan won’t pass, but if the GOP moves up from $1.2 trillion, something will be done. What’s $1 trillion among politicians? We will know what will happen within 5-7 days. The House could pass the bill this week, but the Senate is likely to want less superfluous spending.

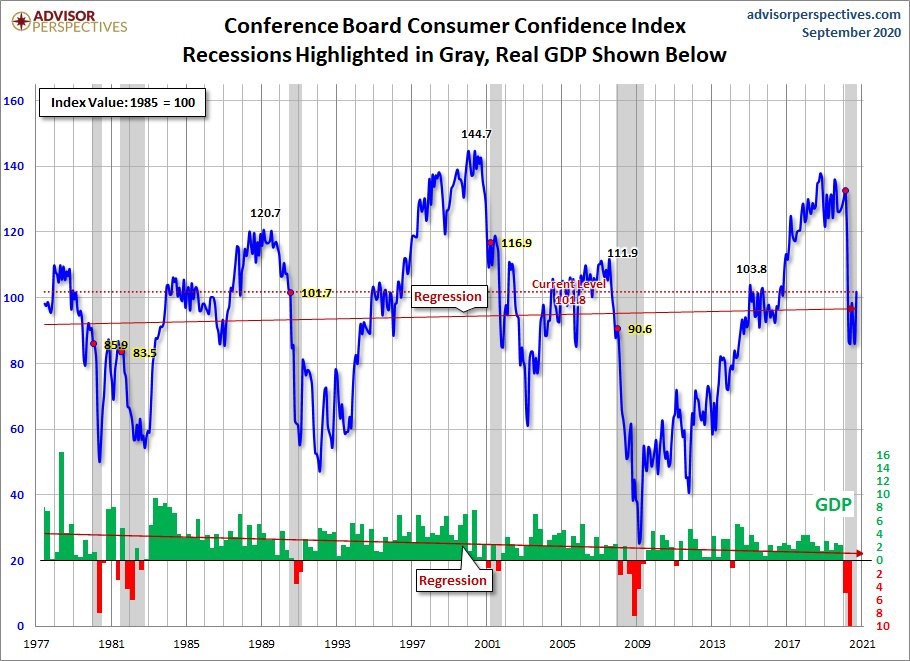

Consumer Confidence Improves Markedly

As you can see from the chart below, the September consumer confidence index was much stronger than last month just like the University of Michigan index. It came in at 101.8 which beat estimates which were 90. That’s the biggest beat since November 2011.

Economists were probably focused on the decline in jobless benefits and the increase in COVID-19 cases. Consumers were focused on the better labor market. This index rose from 86.3 which made this the biggest spike in April 2003. That spells good news for the holiday shopping season. Adding a stimulus on top of this optimism would be a huge boon for retailers.

Expectations index was up from 86.6 to 104 and the present conditions index was up from 85.8 to 98.5. Cutoff date for this survey was September 18th. Some Democrats might be optimistic about the potential for Donald Trump to lose, but the strength in the present index shows the economy truly is getting better.

Net percentage claiming current business conditions are good rose from -27.3% to -19.1%. That’s a massive improvement. It came in a period where stocks fell which implies that consumers ignored the correction.

There was an even bigger increase in the net percentage of consumers expecting business conditions to improve in the next 6 months as it went from 9.1% to 21.3%. 33.1% expect more jobs in the months ahead and 15.6% expect fewer jobs.

Only way you can expect fewer jobs is if you think another wave of COVID-19 is coming. Someone also could be biased by their own industry. There will surely be a few industries which underperform in the next 6 months.

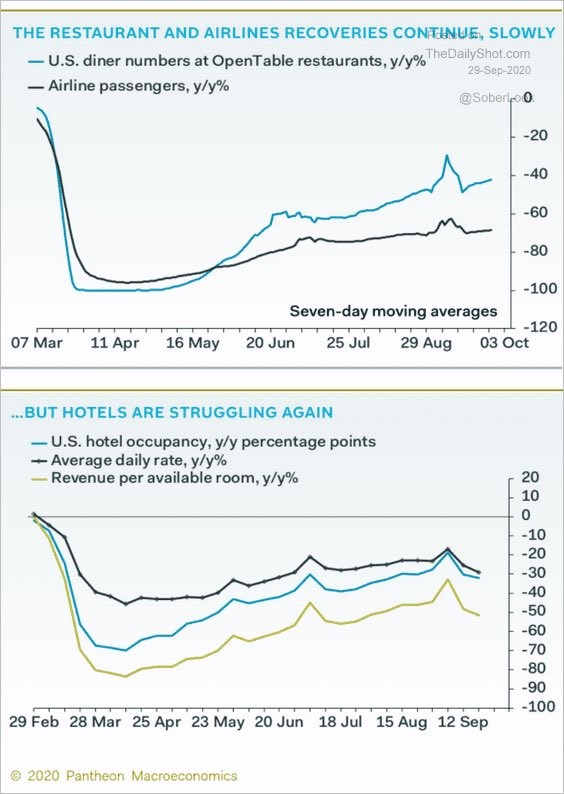

Lumpy Reopening Of The Economy

The economy is reopening, but it’s not an equal recovery across the board because some areas are still deemed unsafe by the public or by politicians. As you can see from the bottom charts below, there was a dip following Labor Day. However, diner numbers improved the most followed by airline passengers in the past 2 weeks. Hotels are doing much worse as they saw declines in revenue per room, daily rates, and occupancy levels in the past 2 weeks.

It’s tough to make a big deal out of 2 weeks of data. However, investors are hyper-focused on the data because COVID-19 is so unpredictable. Normally, a 2 week decline in those things wouldn’t be a big deal. However, normally growth isn’t in the negative double digits.

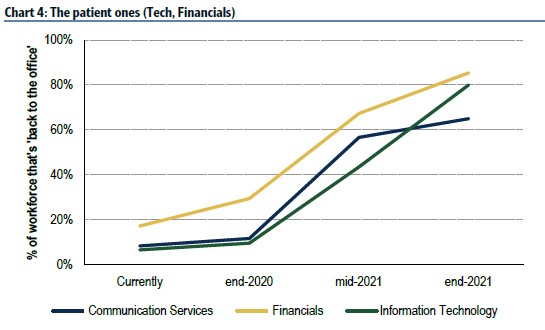

On a similar note, the return to offices hasn’t been the same across industries. The chart below shows hardly any firms in the tech and communication services sectors have their workers back in the office. Financials are also mostly waiting until 2021 to get back to the office.

On the other hand, more than half of firms in the materials, industrials, and energy sectors are back at the office. A problem for firms in the office space industry is that those sectors don’t employ many workers.

This survey based on what businesses think they will do is only an estimate. It’s based on the expectation for better testing, a vaccine, and better treatments by the middle of next year. If you believe it will be materially safer to go back to the office in 9 months and your business is near normal given the weak economy, it makes sense to wait it out.

If you think business won’t be back to normal within the next 2 years, you should either make changes to your business to improve the efficiency of people working from home or start to bring them back this fall as testing permits. Businesses should be able to get rapid testing for workers by the end of the year.

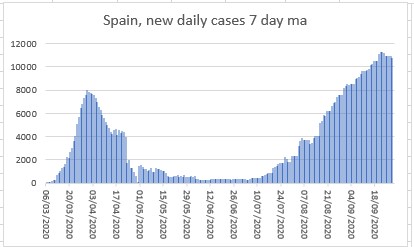

COVID-19 Cases In Europe Peak

It’s no surprise COVID-19 cases in Europe are now peaking because changes were made to limit its spread and people know what to do. As you can see from the chart below, the 7 day average of new cases has peaked in Spain. A problem remains that if the economy reopens in the next few months, we might see another spike.

Death rate is much lower in Europe than in America as the 7 day average of new deaths in France is 67 even though the 7 day average of new cases is 12,083. That’s less than one tenth of the new deaths in America with more than one quarter of the new cases. To be clear, the number of new deaths will probably increase in the next 2 weeks as cases increased rapidly in mid-September. Either way, the death rate is still lower in Europe.