Big Monday Rally In Tech

This stock market is like a machine. The market started August and the week with a modest rally with tech outperforming. Rationally, you’d think this rally in tech can’t continue, but it keeps proving everyone who cares about valuations wrong. Specifically, the S&P 500 was up 0.72% as the big cap companies, Microsoft and Apple dragged it higher again.

Nasdaq was up 1.47% and the tech sector was up 2.46%. This time small caps rallied even though regional banks declined. Russell 2000 was up 1.78%, while the regional bank index fell 0.29%. Small cap growth stocks outperformed as the IWO ETF was up 2.34%. S&P 500 is now up 1.98% year to date. It will likely end the year lower. As for now, this is only a slightly below average year.

S&P 500 has its sights on the February high as it is down just 2.7% from the record. If it were to top at the current price, it would be common to hear about a double top. When the stock market was crashing and starting to recover, most expected a new record high quickly.

However, we didn’t expect it to be led so heavily by the speculative tech stocks. This isn’t a healthy market. This looks like a bear market rally even though a new high would make it officially a bull market. At this point, Apple’s valuation is so high, we can consider it a speculative stock.

It rose 2.5% as it now has a 35 PE multiple despite growing net income by only 7% in the past 5 years. Microsoft stock rose 5.6%. The company is valued so highly that if it acquires Tick Tock for about $50 billion and it doesn’t go well, it wouldn’t be a big issue. $50 billion isn’t much for a $1.64 trillion company.

Usual suspects rallied as Tesla was up 3.8%. At this point, there doesn’t need to be a reason for it to rally. Valuations and fundamentals are completely irrelevant in the short term. Most don’t think the company can last much longer if it continues to have issues with quality control. If it gets that sorted out, the next problem is affordability as the company sells cars that most people can’t afford and it loses money doing so.

It’s not easy to lower prices when you are already losing money at the original price. Shopify stock was up 5.8% to a new record high as it’s now up 236% since its March bottom. Fastly was up 15.7% to a new record high. Even though it isn’t profitable like Shopify, its stock is up 903% since March 16th. Anyone claiming this isn’t a bubble needs to look at this 1990-like gain.

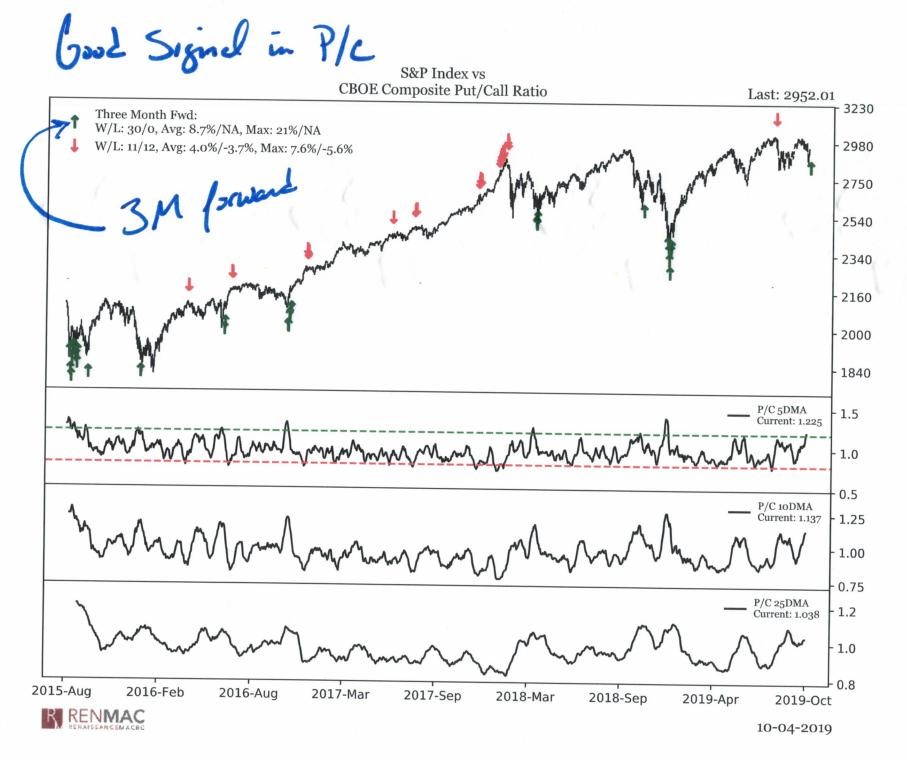

Very Low Put To Call Ratio

There are always expensive stocks in the market, but there has never been bubble valuations in companies as big as Apple and Amazon. This has changed the dynamic of the S&P 500. It’s becoming riskier by the week.

As you can see from the chart below, speculation has pushed the put to call ratio to the lowest level since June 8th which was right before the 7% correction. Furthermore, the 40 day put to call ratio moving average is the lowest since late 2000 after the tech bubble burst. It was lower in 1997, 1998, and 1999 though.

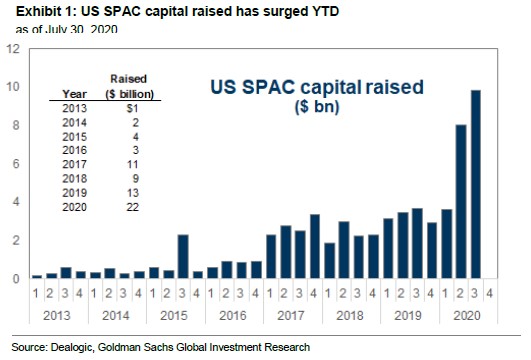

SPACs Are The New 1990s IPOs

Those who say this isn’t a bubble because in the 1990s, there were crazy IPOs have now been proven wrong by the speculative SPAC frenzy. As you can see from the chart below, these reverse mergers have raised $22 billion this year. Even though 2019 was a historically good and quiet year, there has already been more money raised via SPACs this year.

Most famous SPAC is Nikola which was up 21.6% on Monday because of an upgrade by Deutsche Bank. It had a big impact because the stock was very oversold.

Never Seen Before

Speculation in U.S. markets is unlike anything most have seen before. Tch stocks are causing America to dramatically outperform the rest of the world. Some aspects of this market aren’t as frothy as the late 1990s, but the chart below makes the case that we are in unprecedented territory.

As you can see, America’s relative performance versus Europe has never been this great. America has faster growth and more tech stocks, but you’d think Europe would be doing better this year since it has better dealt with COVID-19. STOXX 600 is down 13.4% year to date which is about 15.4% below the S&P 500’s gain.

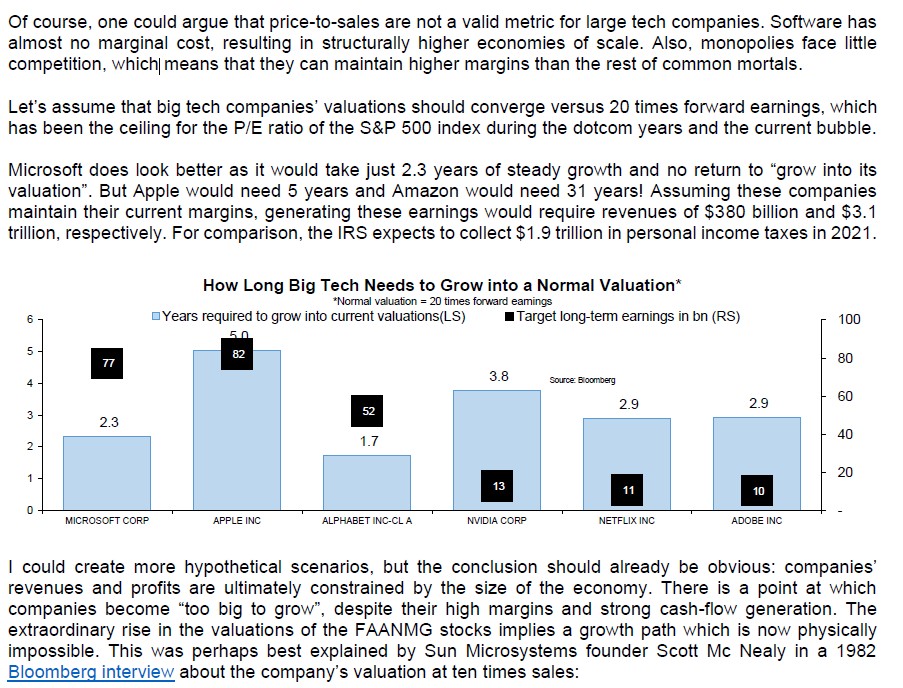

Basically Impossible

Major tech stocks are now so expensive, they are taking over the entire economy on their own. A few years ago, perma bears falsely claimed the stock market was in a bubble because the whole market was higher than GDP. Tech stocks alone are being priced as if they can grow larger than the economy which is representative of a bubble. Goldman Sachs thinks Amazon stock should rise to $4,200. That’s the size of the entire Russell 2000. I’d take the small caps over 1 company.

Amazon would need 31 years of no stock returns to grow into its valuation if it grew at its historical pace, which is an unlikely feat. It’s almost impossible for all of these mega cap tech stocks to grow this much because sales would be $3.1 trillion which is more than all personal income taxes in 2021 ($1.9 trillion).

As you can see from the chart above, Apple would need 5 years to grow into its valuation. Most of the time, expensive stocks don’t grow into their valuation. They usually crash. When a valuation gets so high, the business doesn’t even need to do badly for its stock to be weak.

Best case scenario for these stocks is they have sharp volatility and return nothing in the next decade. If any of them end up achieving the lofty goals the market has set, their stocks will get back to current prices eventually. This is a huge difference from the past few years where FAAMNG has delivered about 20% returns each year.

1 Comment

Neville Newman

August 5, 2020The Bloomberg interview with Scott McNealy was actually in 2002, not 1982. (1982 was the year that Sun Micro was founded). The title of the article is "A Talk with Scott McNealy".

It is actually a great article, definitely worth reading the whole thing. McNealy's explanation of what P/E ratios men for investors (not traders) is beautifully simple.

Also note what McNealy had to say about MSFT trying to get in and be the "choke point" for a wide range of devices to approach ubiquity. He always saw MSFT as the Big Bad. Indeed, we've reached the scary part of his prediction, but the villians are Apple and Google (iOS and Android).

Here is the Bloomberg article. It is paywalled, so if you are not a Bloomberg subscriber you will need to hit ^P while the page is loading and then you can read the article in the print preview window.

https://www.bloomberg.com/news/articles/2002-03-31/a-talk-with-scott-mcnealy