Spending Continues To Rebound

Some economists believe that if we just wait a few more weeks, we will see a decline in consumer spending growth because of lowered jobless benefits. That’s the wrong approach. It's understandable that they want to highlight how bad the situation is for people who haven’t gotten their jobs back and are getting less money.

However, their pain isn’t going to translate into worse overall data. This thesis is supported by the fact that those not getting benefits have already lowered their spending. Why would this negative catalyst hurt spending in September more than August, if the impact has already been felt?

Over the next few weeks, more states will be giving out $300 to $400 in unemployment benefits per week. When unemployed people get the money that was owed to them over the past few weeks, their spending will increase. They will be in worse shape than July, but their odds of getting a job will increase.

Each week, more people will be employed as long as COVID-19 deaths don’t increase. A big battle is unnecessary COVID-19 regulations and businesses taking extra precautions. You can understand why a politician or a CEO would be cautious. They don’t want to be seen as callously risking people’s lives. Maybe if the 7 day average of daily new deaths falls below 300, the situation will normalize even without a vaccine.

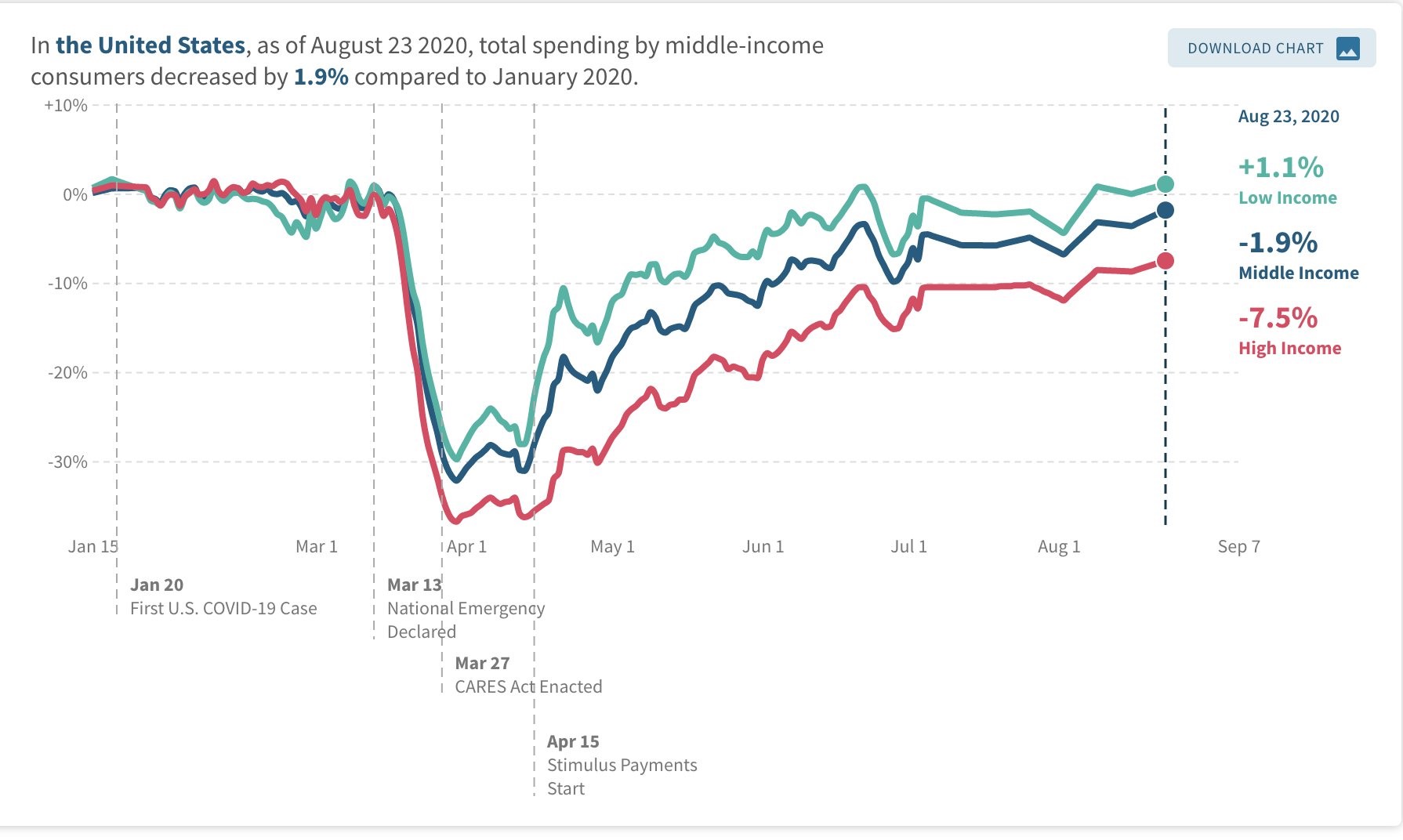

Response in the first two paragraphs of this article is to refute those who go against the data seen in the chart above. As you can see from the chart above, low income spending in the third week of August was 1.1% higher than it was in January. This improvement will only continue as more people in the leisure and hospitality industry get jobs. Those in the middle income class are spending 1.9% less and those with high income are down 7.5%.

As restrictions and worries go away, the high income people will spend more on vacations which will get the low income people more jobs. This recession could easily have less long term damage than the one in 2001 if COVID-19 continues to abate. The fiscal stimulus did its job.

Longer Unemployment

Bears will point to the chart below as reason for concern. As you can see, the share of unemployment over 15 weeks spiked to 60% and the share unemployed for 15-26 weeks increased to 48%. Obviously, the percentage will increase. Either people got their jobs back or are still unemployed.

People getting their jobs back don’t help this data point, but this improvement is still relevant. It’s good to see such a low percentage of people are unemployed for 5 weeks. That means few people have lost their jobs in the past few weeks. Labor market is working through the job losses from this spring. This situation isn’t getting worse.

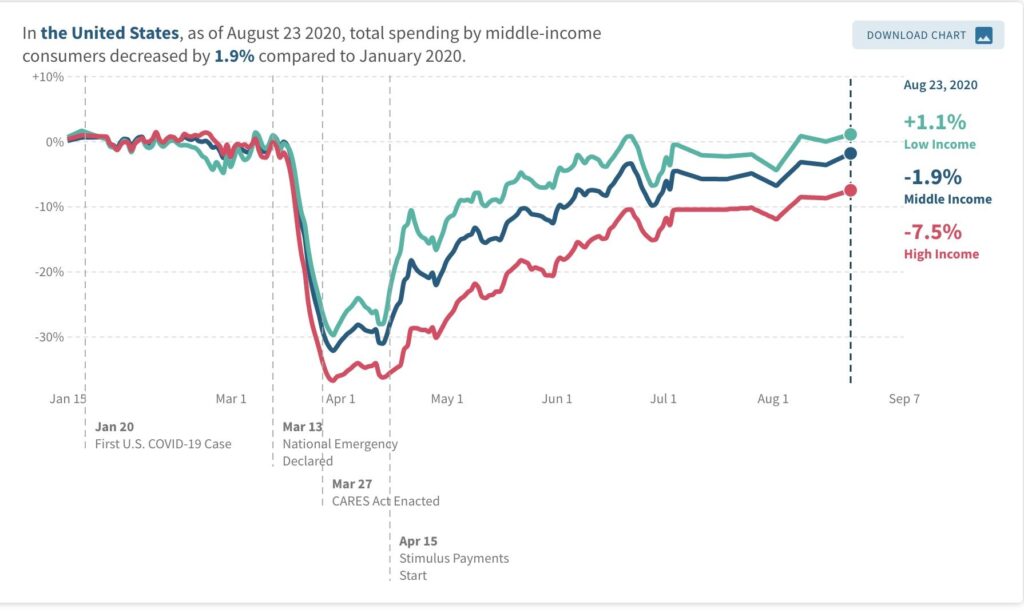

August Small Business Confidence

In August, the small business confidence index rose from 98.8 to 100.2 which beat estimates for 98.9. As you can see from the chart below, confidence is lower than it has been in the past couple years, but it’s above where it was for most of the last expansion. Personally, I think this index is too optimistic for what small firms are facing. However, I only have anecdotal evidence of the stress small businesses are under.

Keep in mind, this survey is biased towards the GOP which means if Biden wins, it will fall. That doesn’t necessarily mean the Democrats are always bad for small business. That’s just how this survey views things. You need to know this because you won’t want to think the economy is suddenly in a disaster because the Democrats won the election (if they do).

The economy is more nuanced than one side being bad or good. Each policy has its own effects. That’s important if you are making individual bets such as going long a certain sector.

NFIB’s chief economist stated, “We are seeing areas of improvement in the small business economy, but many firms are "still struggling" & remain "uncertain." It’s pretty obvious many small businesses are in trouble as they don’t have access to unlimited free money like large firms have.

Small firms might not have technologically savvy management teams which allow people to work from home. They also have a tougher time dealing with new regulations. Within this report, there were 2 major changes. Net percentage saying now is a good time to expand rose 7 points to 12%. Net percentage with positive earnings trends rose 16 points to -25%. This data point is almost always negative. This was a great improvement.

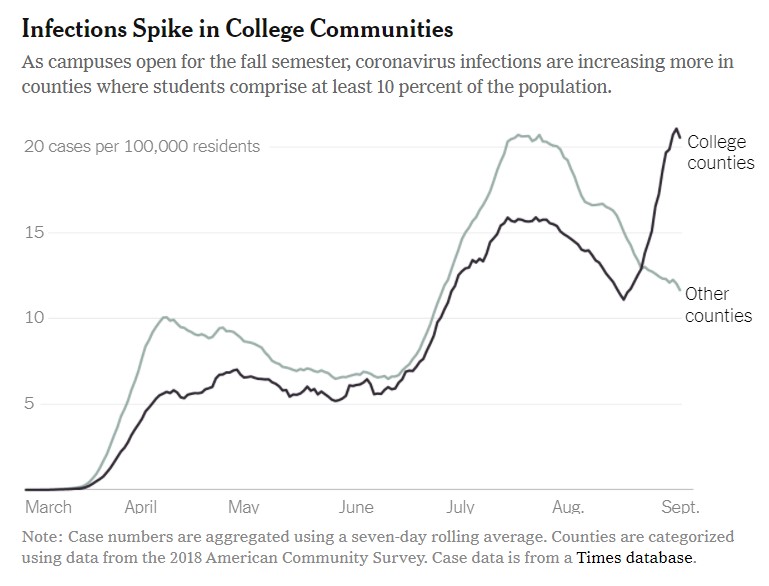

COVID-19 Spread At College

In the past few weeks, COVID-19 cases haven’t been rising nationally despite kids going back to school. On the positive side, the chart below shows counties where less than 10% of their populations have college students have seen COVID-19 cases fall steadily in the past few weeks. On the negative side, counties where at least 10% of their population is students have seen a spike in COVID-19 cases above their record high in late July.

Past couple weeks have seen very little change in cases. This college situation is the change under the surface that the national data doesn’t show. The COVID-19 situation would be in amazing shape without school reopening. Good news is deaths keep falling. That being said, ignore the decline on Tuesday because holidays always lower deaths. Let’s look at how many deaths there are on Wednesday for a better understanding.

Conclusion

Consumer spending growth and small business confidence are improving. Obviously, people unemployed for more than 15 weeks are a larger percentage of the total people unemployed because most job losses occurred in the spring. Good news is the unemployment rate is falling. Great news is COVID-19 deaths have been falling. A spike in COVID-19 cases caused by college students is something to watch out for, but national new cases have been stable.