Slowing Economic Growth - Weak Markit Reports

March flash Markit reports signaled economic weakness accelerated. This was a sharp put down of the rally in stocks this year. At some point, the slowdown needs to end for the stock market to reach its record high. That has been my issue with this rally. It’s possible that the economy recovers late this year, but why jump the gun so much? Why buy stocks at these levels with the economic results weakening?

Technically, the economy always recovers after recessions. That doesn’t mean you should buy stocks right before the recession. The worst bear markets occur before and during recessions. I’m not saying a recession is coming. But I am saying buying extended stocks with no sign of the slowdown ending could be a mistake.

Slowing Economic Growth - German PMI Hits 69 Month Low

German PMI was a big headline generator because of how weak the results were. PMI fell from 52.8 to 51.5 which was a 69 month low. This is the weakest reading since the European recession from 2012 to 2013. Flash services reading fell from 55.3 to 54.9 which was a 2 month low. It continues to outperform manufacturing.

However, the decline helped push the overall index lower.

As you can see from the chart below, the manufacturing PMI fell from 47.6 to 44.7 which was a 79 month low. It is down 10.6 points from last year. Manufacturing output index also fell to a 79 month low as it declined from 47.9 to 45.

Employment at goods producing firms fell for the first time in 3 years. The overall rate of job growth fell to the lowest level since May 2016. Germany’s unemployment rate is 3.2% as of January. It could be headed higher if these weak reports continue. Germany’s manufacturing weakness was blamed on the weakness in the auto industry. It was blamed on Brexit, the weakening global economy, and the U.S. China trade war.

If services weaken more, the PMI could fall below 50 which indicates economic contraction.

Slowing Economic Growth - U.S. PMI Falls To A 6 Month Low

U.S. services growth fell quicker than Germany’s, but its manufacturing PMI was still above 50. This explains why the U.S. PMI indicates the economy’s growth rate is still solid. Specifically, the flash composite index fell from 55.5 to 54.2 which is a 6 month low.

Services index fell from 56 to 54.8 which is a 2 month low. That’s not a weak reading, but it’s not strong enough to make up for the weakness in the manufacturing sector. Manufacturing PMI fell from 53 to 52.5 which was a 21 month low; the manufacturing output index fell from 52.7 to 51.6 which was a 33 month low.

Input price inflation fell to a 2 year low which supports the Fed’s decision to pause its rate hikes. Private sector hiring slowed because of weakness in new business growth. The most interesting part of the Markit report was that despite the weakness, Markit still anticipates GDP growth above 2% in the first quarter.

Markit gives you a plethora of reasons why and how the economy is slowing; then in the comment section it mentions its projection for growth which is higher than almost all the ones I’ve seen. That projection doesn’t mean this was a good report. This report is consistent with the ‘growth slowing’ theme where reports are weak, but not recessionary.

Slowing Economic Growth - GDP Estimates

There are very few estimates showing Q1 GDP growth will be above 2%. The CNBC rapid recap, which was updated on March 15th, shows the median of growth estimates has ranged from 1% to 1.4% with the current average being 1% and the median being 1.4%. That’s including 11 estimates. St. Louis Fed Nowcast is optimistic as usual as it expects 2.19% growth.

Atlanta Fed Nowcast from March 22nd shows growth being 1.2% which is up from 0.4% on March 13th. The estimate increased because the wholesale trade report caused the nowcast of the contribution of inventory investment to increase from -0.4% to -0.02% and because the solid existing home sales report caused the nowcast for real residential investment growth to increase from -4.8% to 0.6%.

I’ve been expecting housing to start positively impacting GDP growth, but so far, the results have been middling. The existing home sales report beat estimates by the most since at least 2005, but it doesn’t affect economic growth. We need to see stronger new home sales for growth to improve.

Nowcast shows the range of the average top 10 and bottom 10 GDP forecasts is between about 0.7% and 2.3%. The estimates fell as the GDP Nowcast improved.

Finally, the NY Fed’s Nowcast shows Q1 growth is expected to be 1.29%. Last week only had 2 reports that affected the Nowcast: the wholesale inventories report and the Philly Fed manufacturing current activity. Interestingly, even though the Philly Fed index beat estimates, it only helped the Nowcast by 1 basis point.

Wholesale inventories hurt it by 9 basis points. The Philly Fed index helped the Q2 GDP estimate by 15 basis points as the overall estimate increase from 1.5% to 1.67%. Since the ECRI leading index was extremely weak to start the year, I have been anticipating weakness in Q2.

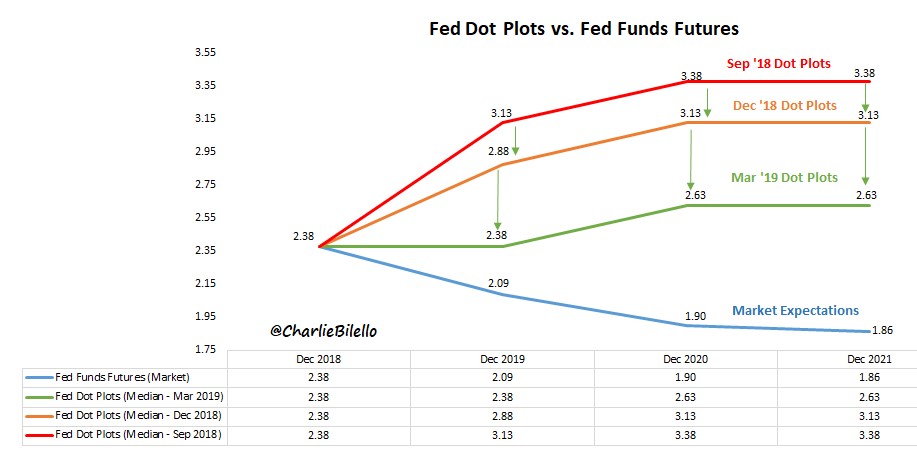

Slowing Economic Growth - Market Expecting Rate Cuts

Fed funds futures market has moved far in the direction of rate cuts. Even with the updated March guidance, the Fed’s rate expectations are way higher than what the market is anticipating. As you can see from the chart below, the market expects rates to be 1.9% in December 2020, while the Fed’s guidance is at 2.63%.

Fed funds futures market has a bad long term track record of predicting where rates will be. That being said, now there is an inverted yield curve, so the Fed is boxed into a corner unlike earlier in this expansion. Just for the Fed to get its one rate hike next year, we will need to see increasing growth expectations and higher inflation.

An inverted yield curve will limit bank lending making it tough to see such an improvement.