The markets are focused on President Trump’s speech to Congress tonight at 9PM. I will be discussing what was mentioned in the speech in my next article. This article will review the latest information we’ve received about the health of the consumer. Target provided terrible guidance while the Conference Board showed the consumer is more optimistic than ever before. I will also review some of the interesting buyback trends and how unrealistic earnings estimates are. Regardless of how great deregulation and tax cuts are, the charts I will show in this article should be disconcerting to even the most adamant bulls.

Some of survey data which attempts to gauge the level of optimism in the economy has been waning slightly, but is still strong. One example of this moderate deceleration was in the Dallas Fed Manufacturing Survey I reviewed in my last article. This trend of moderate deceleration was not confirmed by the latest Conference Board Consumer Confidence Index. This index reached new 15 year highs. The Present Situations Index rose from 130.0 to 133.4 and the Expectations Index rose from 99.3 to 102.4. There was a 1.1 point increase in consumers’ expectations for business conditions to improve in the next 6 months.

I may be reading too much into the data, but I think this shows consumers’ initial hopes about the Trump administration are becoming fulfilled. The other way to look at this is to say all the data is within the range of the initial post-Trump pop. They will remain in that range until legislation starts to pass and we see its results. Some other surveys have shown a political divide over the amount of optimism consumers have, with Democrats having a more pessimistic viewpoint of the economy. This survey doesn’t break down the political differences, but it’s hard to see how many Democrats could be negative if the index is at a 15-year high.

In direct contradiction to this survey, Target reported a disaster quarter which had terrible guidance. Target stock is down 12% today and over 30% since its peak in July 2015. Chalking up poor department store sales to the increase in online sales is an overly simplistic conclusion to make because it ignores the level of deceleration. Target’s Q4 year over year same store sales came in at the low end of its guidance as it showed a decline of 1.5%. The guidance for Q1 expects to see a low-to mid-single digit decline in same store sales. While I don’t buy the idea that the firm’s weakness was only caused by the shift to online sales, I do think Target lost market share. Walmart saw a 1.8% increase in same store sales in Q4 and Walmart U.S. expects to see a 1.0% to 1.5% increase in same store sales in Q1. Signet, the biggest jewelry firm in America, also is seeing weakness, but it’s tough to sort out how much of the weakness is caused by the diamond switching scandal.

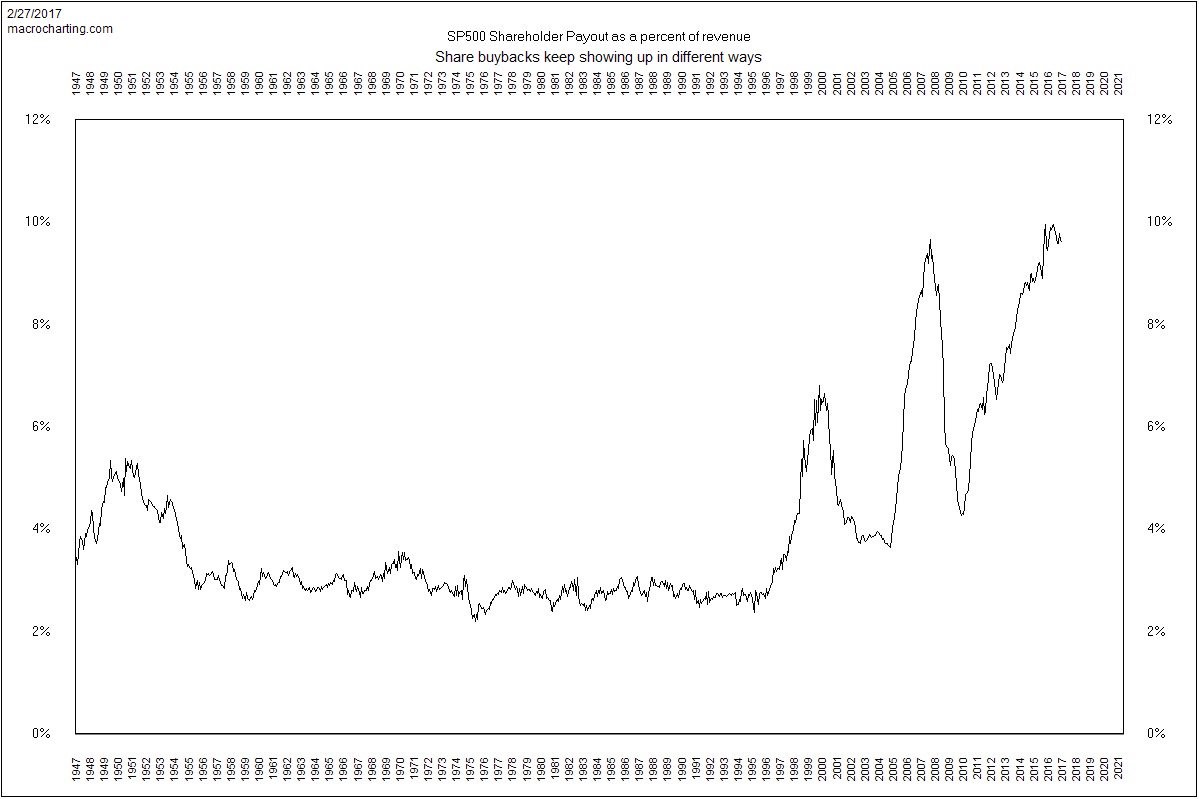

While buybacks have been declining recently, that’s not because management wanted to be more conservative; it’s because earnings had been declining up until recently. The chart below shows the payout percentage of revenues. Businesses are just as levered as they have ever been. I remember in the 2009-2011 period, there was a change in investors’ attitudes about buybacks. Investors thought that the money was wasted because the stock buybacks were purchased at such expensive levels. It’s amazing how quickly people forget about the recent past and make the same mistakes. Buybacks are once again being hailed as a great way to return capital to shareholders. No company will ever admit its stock is overvalued which puts shareholders at risk because the buybacks only artificially push the stock higher. As an investor, I wish buybacks worked the way insider buying worked. The stock should only be bought when it’s undervalued. That’s difficult determination to make, but firms can start with not thinking it’s always a good time to buy back their stock.

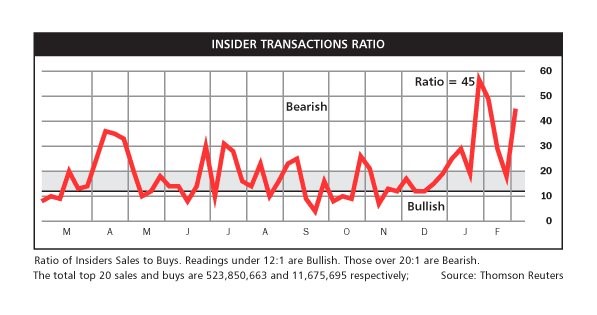

As you can see in the chart below, insiders are selling stocks lately. I am not saying firms must mimic insider transactions because sometimes insiders sell shares to diversify their portfolio. However, I think would be nice to not lever up the company to buy shares that have high PE ratios and are operating at peak margins.

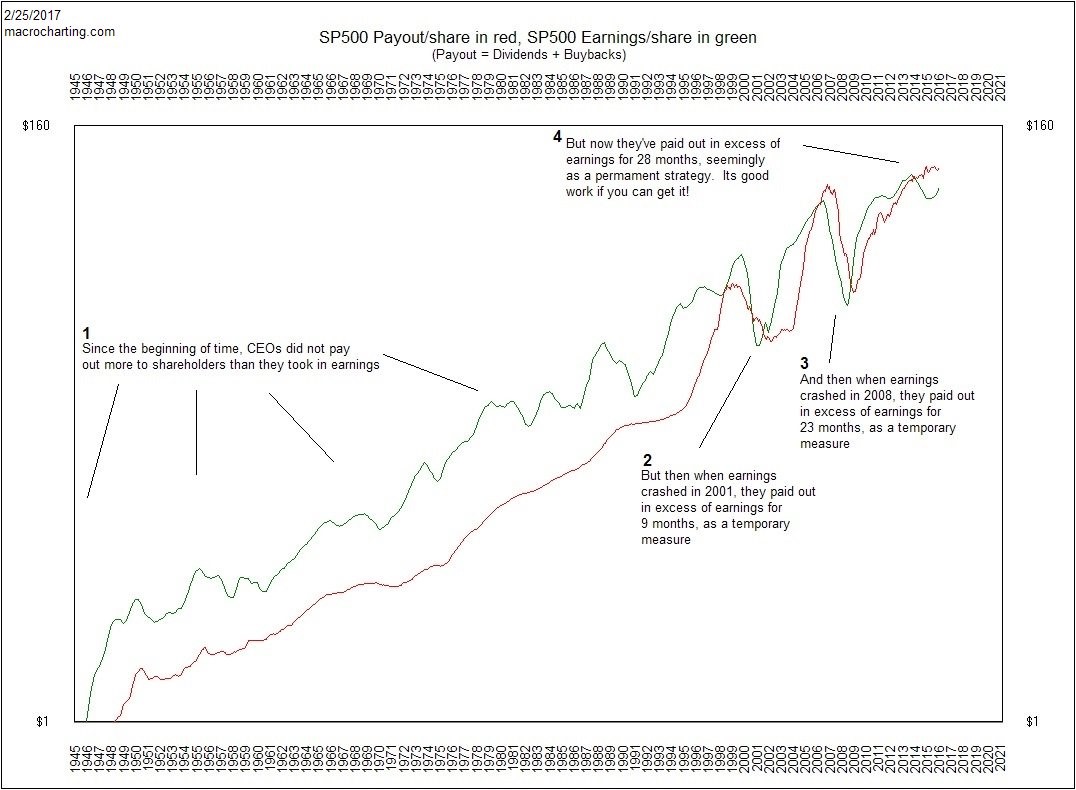

You can see the levering up that I am referring to in the chart below. As you can see the payout of dividends and buybacks has been above earnings for 28 months which is longer than the prior two bubbles. Theoretically, if firms can payout more than they earn, then valuations based on earnings don’t matter as much. The reason this doesn’t work out in the long run is because firms can’t spend money they don’t have. I expect earnings to rebound slightly and buybacks and dividends to increase along with them. The only way the streak of payouts being larger than earnings will be broken is if the stock market crashes and we have a recession.

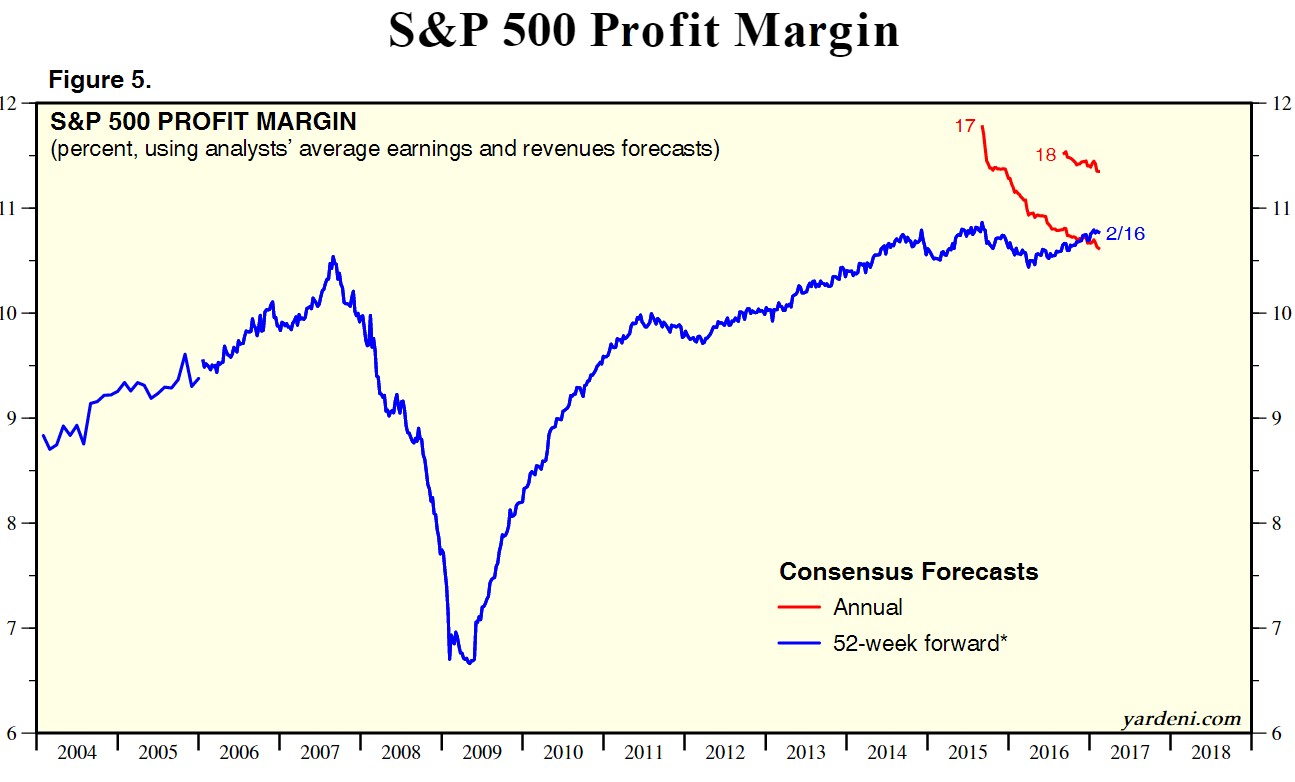

The chart below explains my point that the S&P 500 is at peak profit margins. The initial estimates for 2017 earnings implied record profit margins. The expectations about future growth start out unrealistically and then when initial results start to come in, reality comes into focus. This is like how the Fed never predicts growth will be negative. It’s always near the long-run growth rate. The 2018 earnings growth estimates must fall a lot because margins won’t get that high. There may be a blip higher because of tax cuts and regulation reform, but it seems unreasonable to model into valuation estimates the assumption that margins will remain at peak levels forever.

Conclusion

The consumer sentiment index is the highest in the past 15 years. Investors must be asking Target’s management “if you can’t do well in this environment, what will happen when sentiment weakens?” It’s possible the real environment is worse than the survey indicates since Target is huge retailer, making it a decent bellwether. The chart which shows the payout ratio to S&P 500 earnings is disconcerting. It may take the record margins expected in 2018 to be reached for the payout ratio to flip to the healthier side.