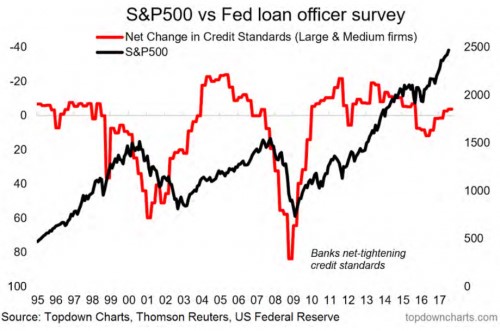

The economy has been improving in 2017 as global trade lifts off. We’ve had one of the most unusual scenarios take place this year. As you can see in the chart below, the Fed loan officer survey shows that the credit conditions have eased despite the Fed raising rates That’s not usually how it works, but the economy has been helped along by the global central banks’ record stimulus in the first half of 2017. The second half won’t be as accommodative as the first half. The real tightness will start in the middle of 2018 if the expectations are met. As you can see, when credit conditions ease, the stock market rises. There are some bullish investors who think that correction in 2016 will lead to another few years of economic growth. It’s not impossible, but it will have to happen without stimulus. This would be the first real growth the economy has seen this recovery. At some point, inflation will weigh on the recovery, but we are at least a few quarters away from that.

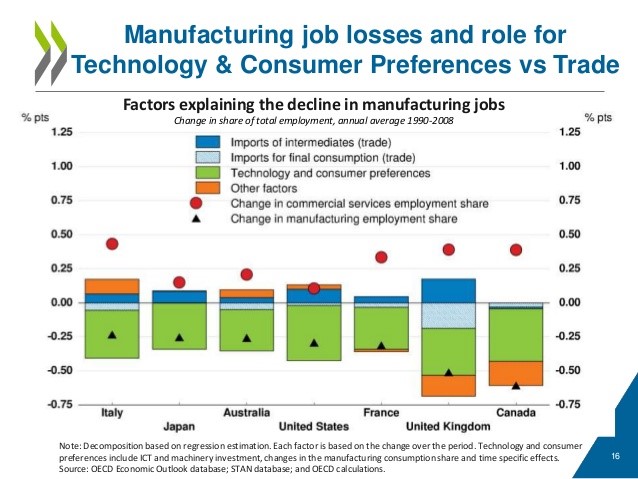

The unemployment rate is low like it usually is at the end of the business cycle, but it doesn’t show the amazing changes in the workforce. Workers are becoming independent contractors instead of working for one employer. Secondly, the baby boomers are just starting to retire which is putting pressure on wage growth. Thirdly, the type of work is changing as services take share from manufacturing. The loss of manufacturing jobs has become a politically contentious topic, but it doesn’t need to be. The chart shows that the U.S. is normal when looking at the other developed countries. The loss in manufacturing employment is coming from changes in tastes, improvements in robotic technology, and other factors such as outsourcing.

There weren’t any economic reports on Monday, but Tuesday was jam packed with them. One of the most important reports was retail sales which beat expectations. Retail sales had their biggest increase in 7 months which should bolster GDP growth. Retail sales were up 0.6% as consumers made more discretionary purchases and surprisingly bought motor vehicles. One of the reasons for the increase in purchases is that prices for new motor vehicles had their biggest drop in almost 8 years and have fallen for 6 straight months. This means demand is being helped by discounting which won’t boost production and help the economy. It’s still way too early to tell where GDP growth will be, but this retail sales report is a great sign. Both June and May were revised higher by one tenth. On a year over year basis the July retail sales were up 4.2%. This has boosted the dollar slightly. I’m still bearish on the dollar, but anytime an economic report beats expectations, it will shoot up.

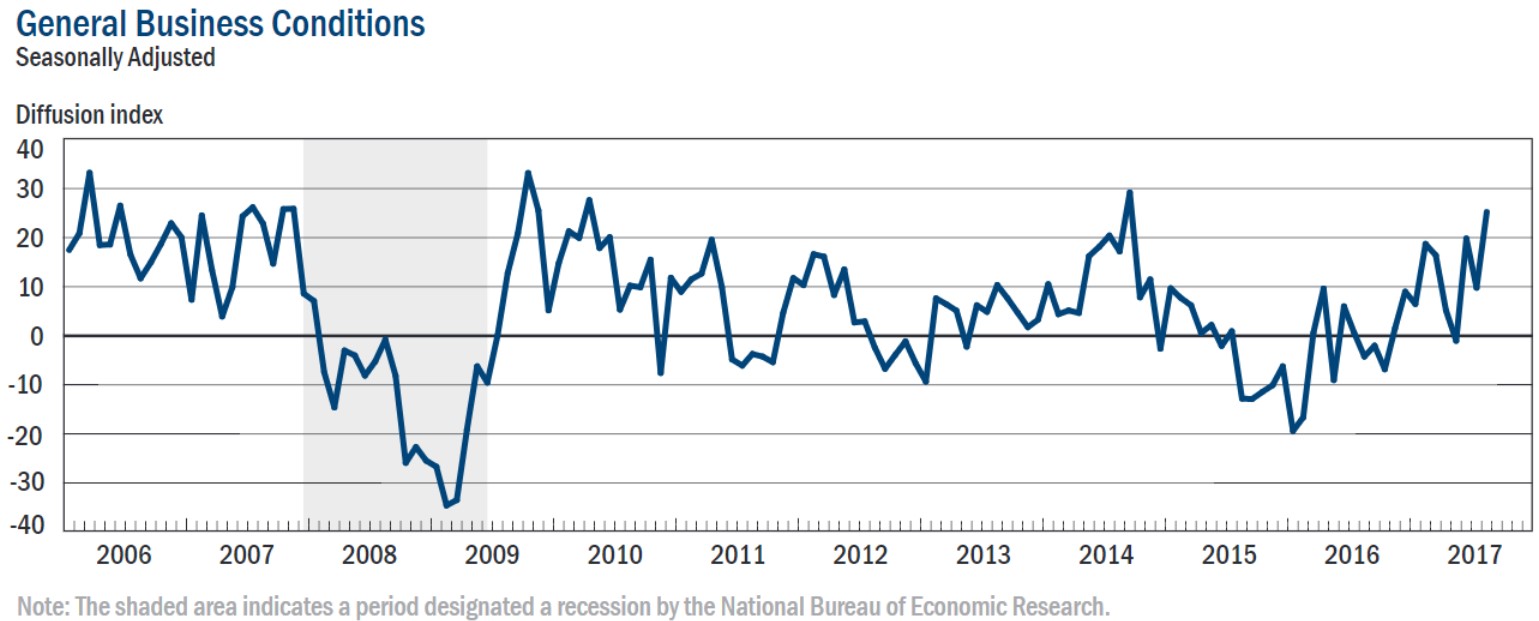

The Empire State Manufacturing index for August was spectacular as you can see in the chart below. The index reached 25.2 which was the highest reading in 3 years. This destroyed estimates for 10.0. The report was great across the board. The new orders index was up 7.3 points, the average workweek index was up 10.9 points, and the number of employees index was up 2.3 points. Looking at inflation, the prices paid index was up 9.7 points, but the prices received index was down 4.8 points. If these great economic reports keep coming out, inflation will come. I consider it great news that inflation isn’t running hot with the economy firing on all cylinders. Looking at the 6-month forward looking indicators, the general business index was up 10.3 points and the new orders index was up 7.9 points. The prices received index was up 6.0 points and the prices paid index was up 2.6 points. There’s nothing to not like about this report. Earlier in the year, it looked like the economy was about to go into another manufacturing recession; clearly that didn’t happen.

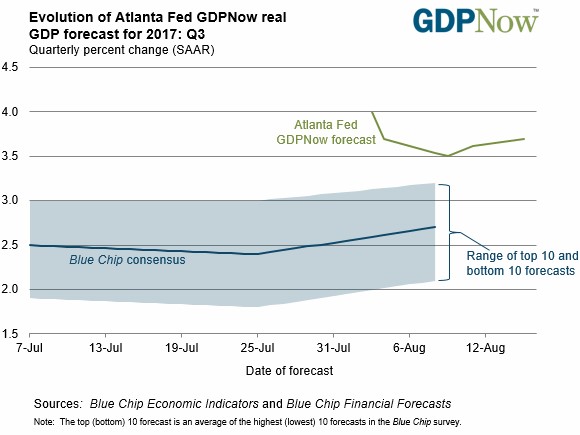

The GDP Now report usually starts high for an unknown reason and falls as economic reports usually don’t show 4% growth. For the first time in a long time, the GDP Now report has improved after the initial estimates as it increased from 3.5% to 3.7%. It increased because of the retail sales report I mentioned earlier in this article. The last NY Fed Nowcast has GDP growth at 1.96%. With the great economic reports, I expect it to go over 2% when it is updated on Friday. The St. Louis Fed is at 3.68% growth. The chart below shows the blue-chip average is now up to about 2.7%. It has been unusual to see improvements to expectations mid-quarter. It’s still very early as September hasn’t happened yet. There could be some economic weakness at the end of the month caused by the debt ceiling issue. I will be watching that along with the first revision to the Q2 GDP report which comes out in 2 weeks.

The other economic report released Tuesday was import and export prices. Import prices were up 0.1%; excluding petroleum they were flat. This isn’t a seasonally adjusted report so you can see the disinflation clearly. Export prices were up 0.4% in July which was the biggest improvement since June 2016. On a year over year basis, import prices were up 1.5% and export prices were up 0.8%.

Conclusion

The economy is doing really well. The stock market did better than the economy earlier in the year, but now the economy is catching up, making up for lost ground. Even though earnings growth will decelerate in Q3 on a year over year basis, Q3 GDP growth could be one of the fastest growth quarters in this recovery. This economic growth could help President Trump get his agenda passed. It’s funny to see the reverse of what was expected occur. We thought the tax cuts and infrastructure program, which President Trump addressed Tuesday, would help the economy, but instead the strong economy might help President Trump get them done. Either the debt ceiling can help the odds of future legislation passing or this could end in disaster. I expect a last-minute deal to get done in October. That’s only a hunch. We’ll get new information in September.