Economic Anxiety

Scars of the COVID-19 shutdown won’t heal easily. These are economic and social. That’s a toxic combination. This situation is directly the opposite of the recent stock market performance. The stock market is acting as if COVID-19 is a done deal and any of its consequences will be gone in a few months.

We’ve never seen anything like the contrast we have today where Wall Street is extremely euphoric and Main Street is in despair. Only traders who are bearish see this situation for what it is. Consumers are optimistic because of the stock market and because many likely believe it can’t get any worse than it is now. The stock market has a high correlation with confidence.

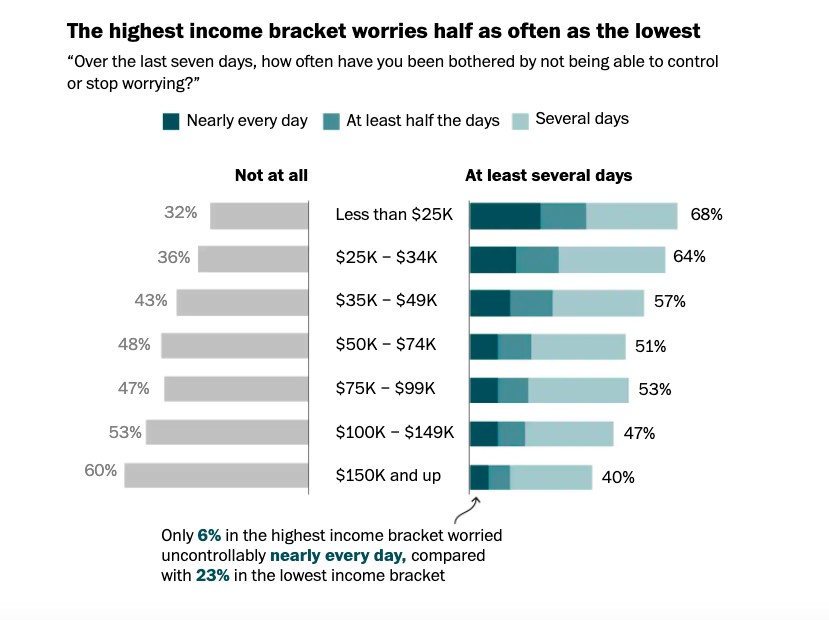

As you can see from the chart above, of the people making $25,000 or less per year, 68% couldn’t stop worrying for at least several days. It’s 64% for those making $25,000 to $34,000. This clearly is economic because of those making $150,000 or more, 60% had no days where they couldn’t stop worrying. It's an extremely sensitive topic for people. A huge swath of people won’t be mentally back to normal right away.

For months economists have been saying you can just flip a switch to get the economy going again. Clearly, you can’t because even the states that have opened are taking precautions. Plus, most Americans making under six figures are mentally drained. Surely, reopening and an improved labor market will help. We're looking forward to hopefully discussing improved figures soon.

Job Postings Improve

This looks like a Nike swoosh recovery as the beginning of the recession was quick and the recovery is slow and gradual. That occurred in the stock market, except the stock market is way ahead of the economy. The stock market is so far ahead of the economy, it wouldn’t be surprising to see stocks decline even as good news comes out.

It’s debatable if the latest data counts as good news because it’s expected improvement from an impossibly weak result. The only possible scenario where the economy didn’t improve in May was a spike in COVID-19 cases. Based on expectations, an improvement in the rate of change of data isn’t impressive.

As you can see from the chart above, the yearly decline in job postings on Indeed in the week of May 1st was 39.3%. In the week of May 22nd, the growth rate improved to -35.1%. This is still an incredibly bad reading. Personally, I need to see quicker improvement to justify the stock market at this level.

When the stock market was 10% to 15% lower, you didn’t need to know much about the recovery. You just needed to know it would happen to buy stocks. Threshold is ramping up dramatically to justify the higher prices. We’re getting to the point where stocks should fall even if the recovery goes according to plan.

That being said, the data is unmistakably better than it was in April and it is very likely to improve in June. How could it not improve with NYC and LA likely to open soon? NYC is on track to open in the 1st or 2nd week of June and Long Island is opening on May 27th. Open Table data on restaurant bookings growth has improved from -99.9% on April 30th to -86.8% growth on May 25th. Best of the 7 countries listed was Germany with -56.4% growth on May 25th.

Consumer Confidence Improves

Last month’s consumer confidence reading from the Conference Board shocked people. That’s because the economy was in tatters, yet expectations improved. My expectation for sentiment to bottom in April looks good from the University of Michigan poll’s perspective. Conference Board survey is a little bit ahead of the curve.

Differences between the current and expectations index explain how stocks are doing well, but economic anxiety is prevalent amount most in the middle class and poor. Specifically, the present situation index fell from 73 to 72.2 and the expectations index rose from 94.3 to 96.9.

That’s the preliminary May reading with the cutoff date being May 14th. It wouldn’t be surprising if the current data was even more optimistic about the future because the stock market has done well in the past couple weeks.

Percentage of consumers saying business conditions were good fell from 19.9% to 16.3%. We still don’t understand who would ever qualify the deepest recession in 90 years as having good business conditions. Unemployment rate is set to be in the mid-20s in May. Labor report comes out next Friday.

Those saying business conditions are bad rose from 45.3% to 52.1%. Those saying jobs are plentiful fell from 18.8% to 17.4% and those saying jobs are hard to get fell from 34.5% to 27.8%. Net figure actually improved which is shocking because we already know the labor market was mostly terrible in the first half of May.

Optimism comes from the stock market, the stimulus, and the fact that it can’t get much worse than it was in the first half of May. The economy will undoubtedly get better this summer. Then, we must see if a 2nd wave comes in the fall.

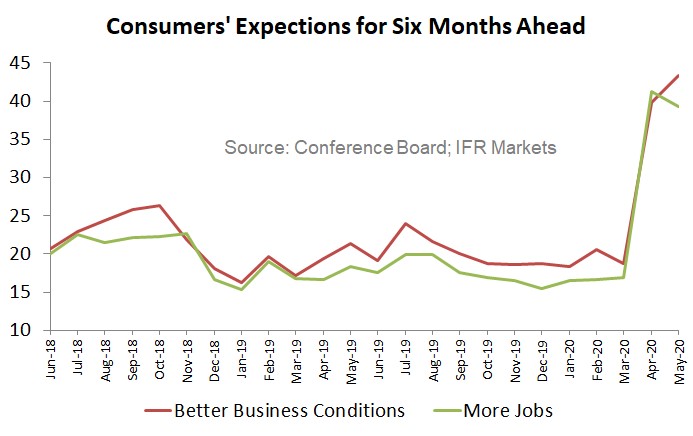

As you can see from the chart above, those expecting better business conditions rose from 39.8% to 43.3% in the next 6 months. Those expecting business conditions to get worse fell from 25.1% to 21.4%. Those expecting more jobs fell from 41.2% to 39.3% and those expecting fewer jobs fell 1 point to 20.2%.

Finally, short term income prospects were mixed as those expecting an improvement fell from 17.2% to 14% and those expecting a decline fell from 18.4% to 15%. It appears there is an increase in people thinking income will be unchanged as both fell. Unemployment benefit income is about to fall as the $600 weekly benefit expires at the end of July.