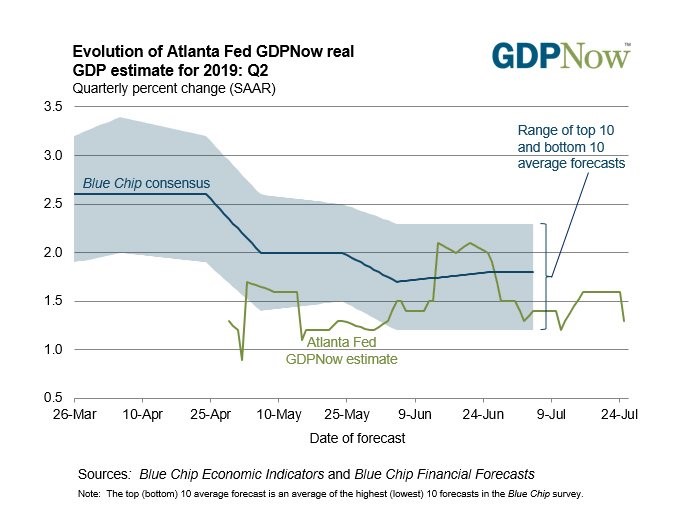

Q2 GDP Growth - The Final Atlanta Fed GDP Nowcast

Q2 GDP Growth showed as the final Q2 Atlanta Fed GDP Nowcast was released on Thursday. It was a dud as the estimate was lowered from 1.6% to 1.3%. You can see this from the chart below.

This report is expected to be the exact opposite of Q1, namely headline growth will be much lower. But the underlying numbers will be much higher. Specifically, net exports and inventory investment will subtract 1.72% from GDP growth.

Domestic demand outside of trade and inventories will show growth of 3%.

Q2 GDP Growth - Hopefully, the bears who complained about the weakness in underlying growth in Q1 will recognize the improvement in Q2. I don’t count on that happening. Stay consistent. Always compare the same data points. Moving the goal post to fit a narrative is a mistake.

Advance economic indicators and the advance durable manufacturing goods orders caused the estimates for the contributions of inventory investment and net exports to fall. Specifically fall from -0.97% and -0.5% to -1.09% and -0.63%.

We always knew they would hurt GDP growth, but we didn’t know the impact would be that bad. Those results mean headline GDP growth will probably be strong in the 2nd half, but that doesn’t matter. What matters is real final sales.

To be clear, the Atlanta Fed’s estimate is more bearish than most estimates. It’s even below the NY Fed’s Nowcast from last week. That might update lower on Friday. The CNBC median estimate is for 1.8% GDP growth; the range of estimates is from 1.5% to 2%.

That’s as of Thursday, so they are the final estimates. There is no new data releases between Thursday afternoon and Friday that can change anyone’s estimate.

Q2 GDP Growth - Very Solid Durable Goods Orders

You have to question the weak manufacturing surveys such as the one from Markit and the one from the Richmond Fed because actual results aren’t that bad. Hard data reports such as the durable goods orders reading and the industrial production report don’t signal a 1% decline in output and terrible sentiment.

June durable goods orders report beat estimates dramatically across the board. Headline new orders growth was 2% monthly which beat estimates for 0.5% and the highest estimate which was 1.8%. However, the prior reading was revised down from -1.3% to -2.3%. That puts a damper on results.

Excluding transportation, monthly growth was 1.2% which beat estimates for 0.2% and the highest estimate which was for 0.5% growth. Unlike headline orders, this index’s previous growth rate was revised higher to 0.5% from 0.3%.

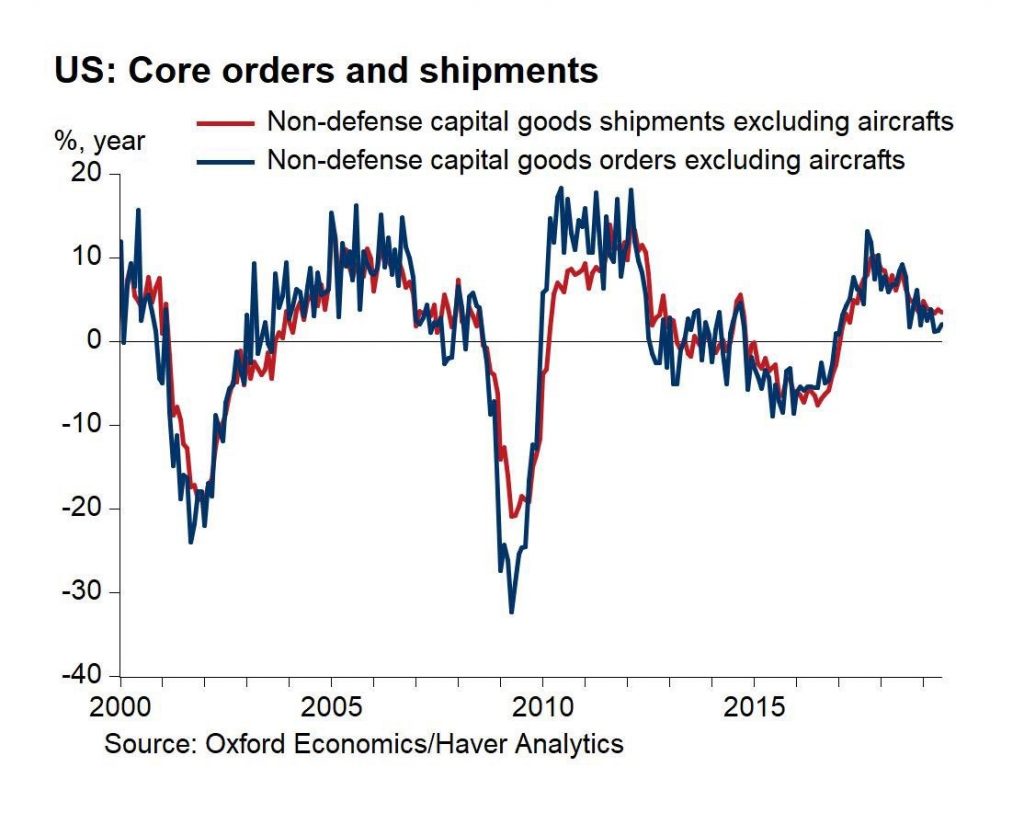

Best part of this report was core capital goods orders growth which was 1.9% monthly which beat estimates for 0.2% and the highest estimate which was 0.3%. In May, that index’s growth rate was revised slightly lower from 0.4% to 0.3%. Shipments growth was 1.4% and core shipments growth was 0.6%.

Yearly core orders growth improved from 1.2% to 2% which is the best reading since March.

Q2 GDP Growth - Obviously, this report doesn’t signal we are definitely headed for a new upturn in manufacturing, but it’s not as bad as many expected. This reading is also lapping a very tough comp. Growth was 8.4% in June. July comp is tougher as that was last year’s peak. Yearly growth might be negative next month; anything positive is a plus in my opinion.

New orders for machinery and fabrications were up 2.4% and 2.1% monthly. Orders for primary metals were up 0.8%. New orders excluding capital goods were strong as orders for motor vehicles were up 3.1%. That’s obviously a big difference from the Markit report. It showed the auto industry brought down the manufacturing PMI.

Civilian aircraft orders exploded 75.5% because of the rebound after Boeing’s 737 issues in months past. Defense aircraft orders fell 32.1%. That’s not a big deal as defense spending has increased during this administration. United Technologies, which merged with Raytheon, just had a great quarter.

Another weak part of this report was unfilled orders which fell for the 3rd straight month. They fell 0.7% in June. Unfilled civilian aircraft orders fell 0.8%.

Q2 GDP Growth - Yet Another Great Jobless Claims Report

Markit employment reading fell to a 27 month low, but jobless claims have been strong this month. It’s now tough to say if the new orders index in the manufacturing ISM will improve, but it’s easy to see jobless claims will boost the leading indicators index.

Markit shows 130,000 jobs being added in July. I don’t think that’s bad news, but it must be framed with recent results in the Markit reading which were higher. It’s like looking at the University of Michigan consumer inflation forecast. It doesn’t matter what actual inflation is in relation to this estimate. It only matters what past results were. Compare apples to apples.

Specifically, the jobless claims report in the week of July 20th showed initial claims fell from 216,000 to 206,000. That was much below the consensus of 219,000. 4 week moving average fell sharply from 218,750 to 213,000. This is the 3rd straight week that average has fallen.

Personally, I still believe it won’t fall below the April low. But I think it will stay low in the near term (next 3 months). Based on these reports, I expect July job creation to be between 150,000 and 200,000. This wouldn’t be the first time this year the Markit guess was too low.

Conclusion

Q2 GDP growth will be much lower than Q1. It might even be below 1.5%. However, if real final sales growth is strong, it doesn’t matter what the headline reading is. Thursday had 2 great economic reports and stocks fell.

Lately, it seems like stocks are falling on good results, but I will chalk up stock performance to other news events like earnings reports. Either way, durable goods orders showed a solid monthly improvement and jobless claims were strong again.

The 4 week average has fallen every week in July. Renewed strength on the labor market doesn’t jive with rate cuts.