Q2 Optimism Along With Weak Philly Fed

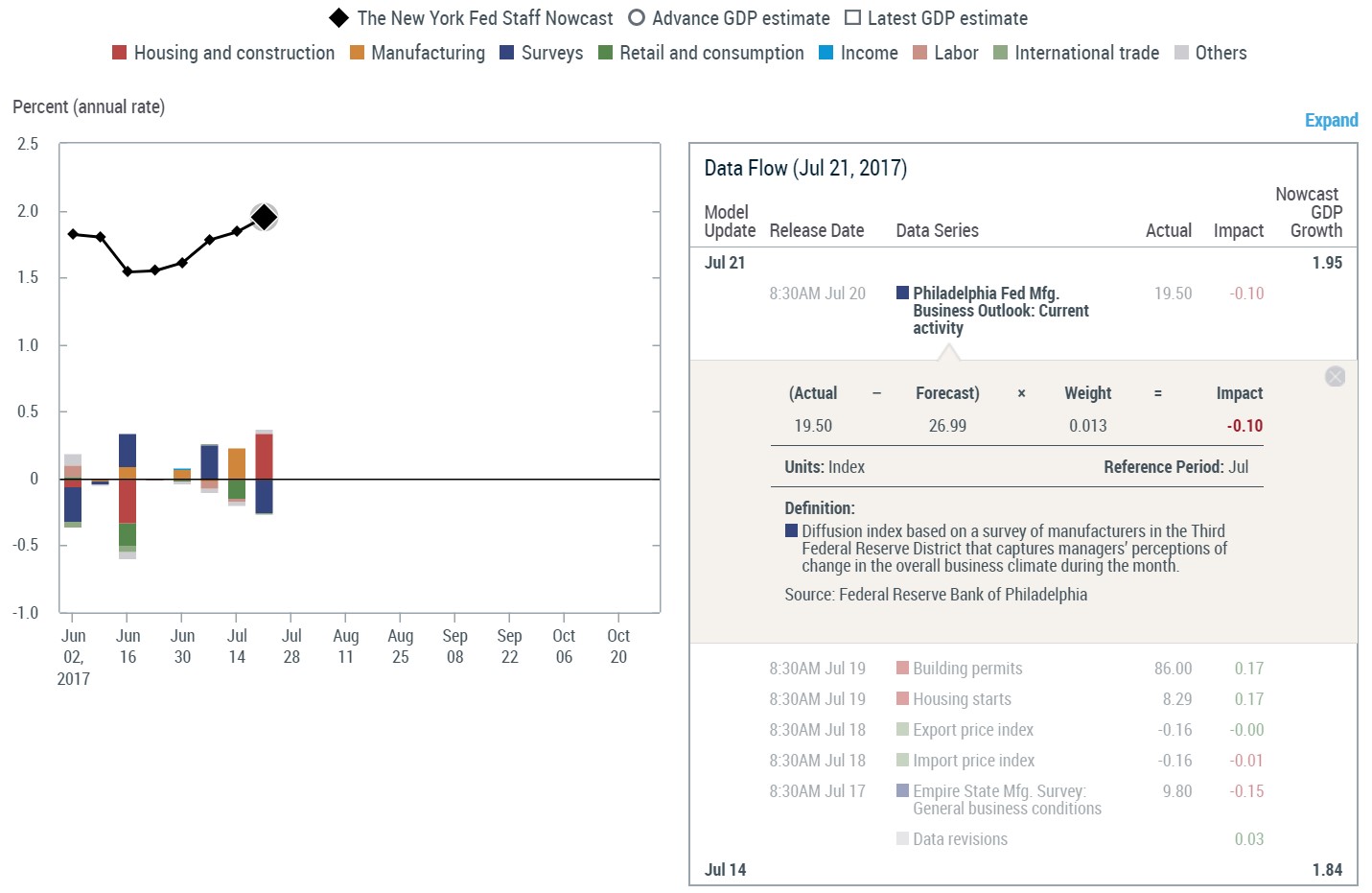

The two Q2 GDP forecasts from the Fed increased slightly even though one of the most important economic reports of the week showed a sequential decline. This was because it was a July report which is outside the second quarter. We’ll go over the changes in the forecasts later. First let’s look at the decline in the Philly Fed index seen in the chart below. The headline number fell from 27.6 in June to 19.5. The 6-month forecast increased from 31.3 to 36.9. I have been focused on the prices paid segment to see if any inflation is sprouting in line with what the 10-year breakeven rate shows. The Philly Fed’s price index was weak as the price received index was down 11.6 points and the prices paid index was down 4.5 points. The 6-month expectation index saw prices received inch up 1.0 point and prices paid increased 5.7 points. This shows the current situation for inflation is still moribund, but the expectation is for a slight rebound. This report doesn’t help the Fed’s quest to find inflation increases.

As I mentioned, the Fed’s forecasts improved slightly. The Atlanta Fed’s penultimate forecast for Q2 GDP increased one tenth of a percent to 2.5%. The residential construction report caused the estimate for real residential investment growth to rise from -1.6% to -0.6%. The NY Fed’s forecast improved .14% to 2.04%. The chart below shows the Q3 forecast which includes the reporting period for which the Philly Fed’s report took place. Even with the -0.1% impact on the forecast, it increased by 0.11% to 1.95%. The Q3 forecast has been on a big winning streak since the last time I mentioned it a few weeks ago. This is positive news as we might end up having back to back quarters with over 2% annualized growth as I’m expecting 2.25% growth in Q2. While those aren’t historically high numbers, for an environment with a decelerating birthrate, it’s probably higher than the long run growth rate. Besides a temporary boost from tax cuts, sustainable annualized GDP growth of 3% or higher is a relic of the past.

The final economic report that I will mention is the leading indicators report which beat expectations for June by two tenths of one percent as it was up 0.6%. This is up from 0.3% growth in May. Keep in mind that this is a June report which means it is included in the second quarter. This metric includes 10 reports such as manufacturers' new orders, stock prices, and average weekly initial claims for unemployment insurance. Anything that includes stock prices will be higher as the bull market roars on. The bull market’s effect matters for the economy even though I downplay it. To be clear, I downplay the concept of using monetary policy to boost stock prices which causes a wealth effect for shareholders causing them to feel rich and buy more stuff. I think it makes more sense to focus on wage growth and inflation. That being said, a strong stock and junk bond market allows companies to raise capital to expand operations. That’s a strong tailwind at the back of the economy.

Debt Ceiling

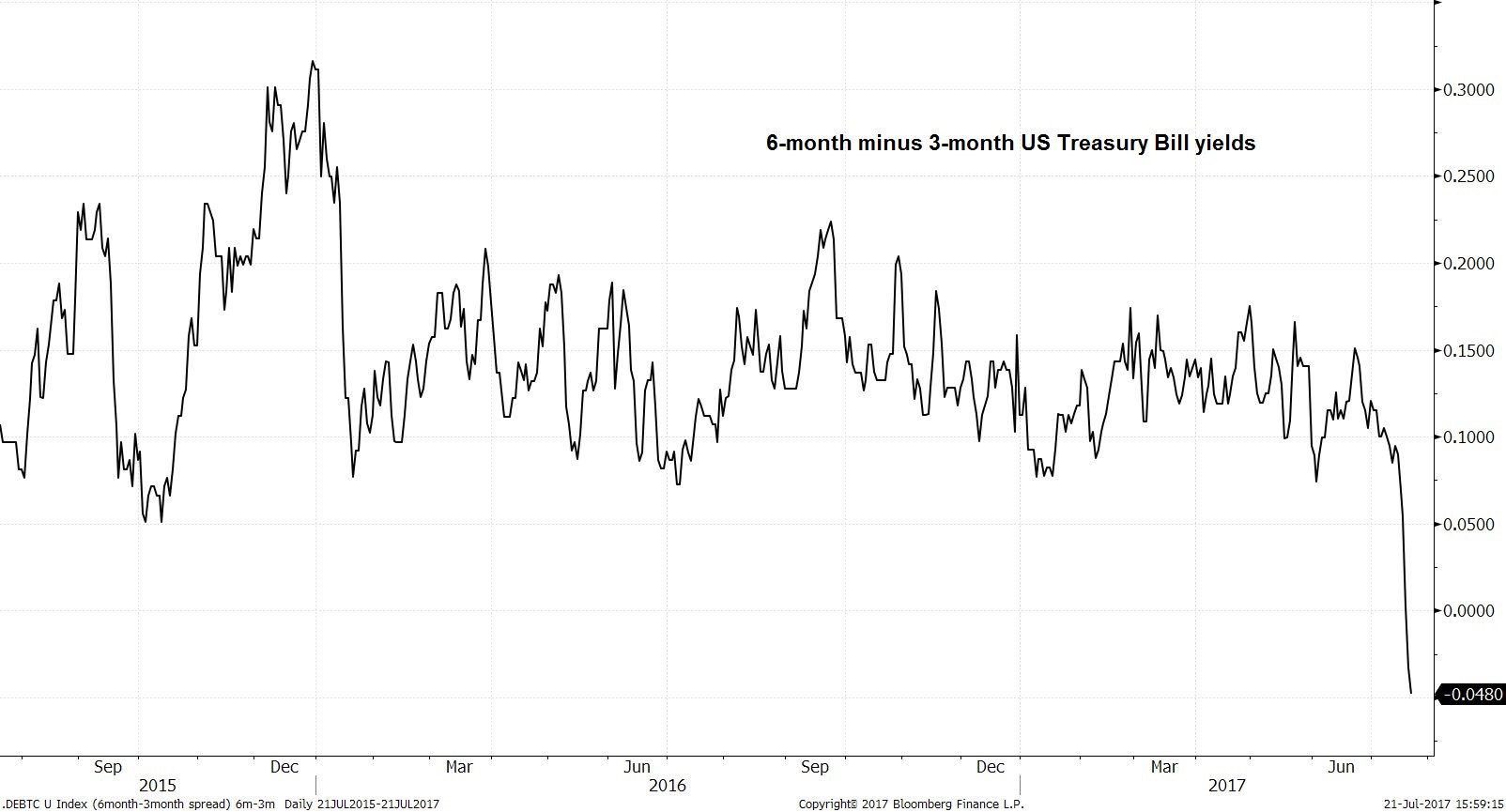

My initial thought on the debt ceiling was that passing healthcare reform would cause momentum which would allow the debt ceiling to be raised easily. Nothing easy comes in Washington as the healthcare plan is facing a brick wall. If it doesn’t pass, there will be ill will among Congress which will make getting a deal done on the debt ceiling harder. The chart below shows the short-term yield curve inverting because the government might face problems with the debt ceiling. It makes more sense to buy a 3 month bill than a 6 month bill.

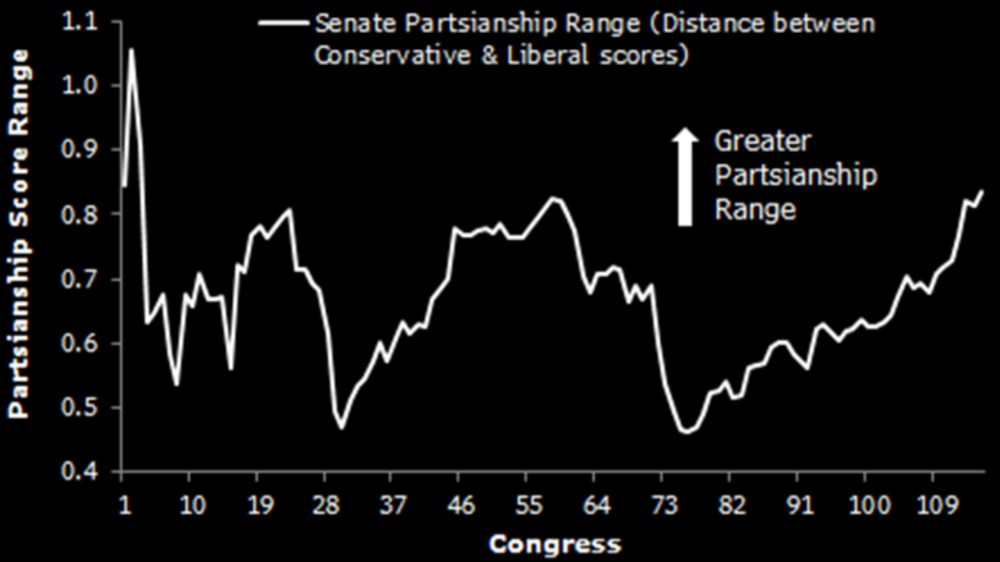

Obviously, the debt ceiling will be raised in the fall, but the longer Congress waits, the more stress the markets will face. If there’s no deal by the end of August, the stock market will drift lower. In 2011, S&P downgraded America. If another ratings agency does that, it would cause a selloff in stocks and a buying spree in treasuries ironically because they are a ‘flight to safety’ investment. This fiasco would be a negative signal to the market that tax reform won’t be passed because raising the debt ceiling should be easy for a Congress controlled by one party. Trump and the Republicans will see their approval ratings fall if this occurs which will make it tougher to get anything done. This friction isn’t because of incompetency. It’s because of the huge ideological divide among Republicans. The chart below predicted the debt ceiling calamity in 2011. It shows the level of partisanship in the Senate. It has reached an epic divergence, not seen since the founding of the country.

The Fed meeting is next week. The decision will be to not raises rates as the market gives that a 96.9% probability. As usual, the statement will be telling. The Fed is now getting the economic data it needs to raise rates (besides inflation), but the handoff of growth being supported by monetary policy to fiscal policy is being botched. This could cause the Fed to have a dovish tone. The debt ceiling issue will impact the statement directly in the September meeting if it isn’t raised. This situation is unlucky for the Fed as it might be starting its unwind in October in the midst of chaos.

Conclusion

My GDP estimate is slightly below the blue chip’s expectation for 2.8% growth. Regardless of whichever estimate the report hits, growth will be solid. I am upgrading my angst over the debt ceiling. I am aware of the ideological divide in the GOP, but I didn’t realize that such a basic thing like raising the debt ceiling would be trouble. The dire situation I ran through certainly isn’t the base case as today, but it will be in a few weeks if nothing is done and Congress goes on vacation.