Multiples Are High

Recently, forward EPS estimates seemled like they might be bottoming which is a positive. This was in the discussion on how PE multiples rose about 60% since the bottom just like they did in the few months after the March 2009 bottom. If earnings rise, they can help stocks further this run. A key point was that Raymond James completely whiffed on is that stocks are way more expensive compared to 2009. You can’t compare percentage changes to multiples without looking at what they rose to.

Specifically, the S&P 500’s forward PE ratio rose from about 9 to 14 in 2009 after the bottom. This time it rose from about 13 to almost 22. That’s a slight of hand that can’t be ignored. If a student goes from a score of 50% to 75% they are passing; if another student starts at 30% and raises its score by 50% to 45%, they are still failing.

The stock market is expensive because of tech and healthcare stocks. Industrials are actually slightly cheaper than the rest of the world’s market. High valuation is a sector specific issue which has the potential to cause a crash because of how large it has gotten. If you’re a bull, you should hope for a 10% correction in cloud and biotech stocks because that will remove the euphoria. If they keep exploding, the decline will be larger.

Shopify now has a $89 billion market cap. Bigger it gets, the greater the impact the fall will have on the market. With the speed it has been rallying at, we could be looking at a $150 billion company before the bubble pops. The company is doing well, but not that well. If a consumer staples stock beats EPS estimates by 5%, does its stock rise 50%?

No, unless market expectations were for a big miss. Shopify literally gets a grade of F or unavailable for every single valuation metric. That’s impressive. It has a forward enterprise value to sales multiple of 44.45. Even if estimates are dramatically too low, this stock is dramatically overpriced. At the peak in February, it had a price to sales ratio of about 39; now it’s at 55.

Earnings Update

Q1 earnings season is basically over. As of May 21st, 478 S&P 500 firms had reported earnings. This change to Q2 EPS growth estimates has been profound this month as expected. EPS estimates always fall during earnings season. Sine many firms can’t even give guidance, it would be a bloodbath.

Remember, stocks likely wouldn’t fall when bad earnings came out. Obviously, individual stocks have fallen, but the market has been fine overall. That’s because everyone knew results would be bad. Stocks might rally in the Q2 earnings period because while estimates will be bad, guidance should improve. It's more worriesome about how the re-openings go and the general euphoria in tech stocks.

As a result of Q1 earnings season, the EPS growth estimate for Q2 fell from -36.45% on May 1st to -43.9% on May 22nd. Just as expected, EPS won’t be negative. However, growth will still be really bad. Even when firms beat results, growth will probably be below -40% because estimates aren’t fully done falling.

Current estimate for Q3 growth is -26.55% and the estimate for Q4 is -14.11%. Q4 is up in the air. That estimate could easily be far too bearish if the economy starts to recover in the summer. It could be too high if a 2nd wave of COVID-19 occurs.

FactSet Results

Now let’s look at the data from FactSet. Of the 474 firms that reported Q1 results, 267 gave comments on guidance. 172 withdrew their guidance and 95 gave full year guidance. If a company gave guidance, it was a positive almost no matter how bad it was. Generally, good results are correlated with the ability to give guidance. 31 consumer discretionary firms withdrew guidance and only 1 gave guidance. That was the worst ratio.

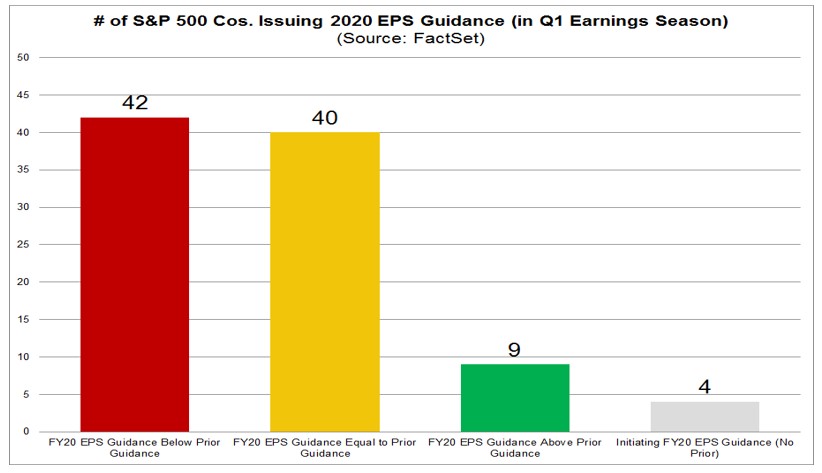

Best ratio was from utilities as 24 gave guidance and only 2 withdrew it. Good performance is correlated with the ability to give guidance, referring to the results relative to firms that can’t give guidance. Very few firms gave good guidance on an absolute basis. As you can see from the chart below, 42 firms lowered guidance, 40 firms maintained guidance, and 9 firms raised guidance. If your firm raised guidance, it was the crème of the crop.

Bottoms up EPS estimate for 2020 has fallen from $177.81 to $128.49 this year. On that basis, the current EPS multiple is 23 which is unusually high. Stocks have high multiples compared to trough earnings, but this recovery has been too strong especially from tech.

Beginning Of Energy Cycle

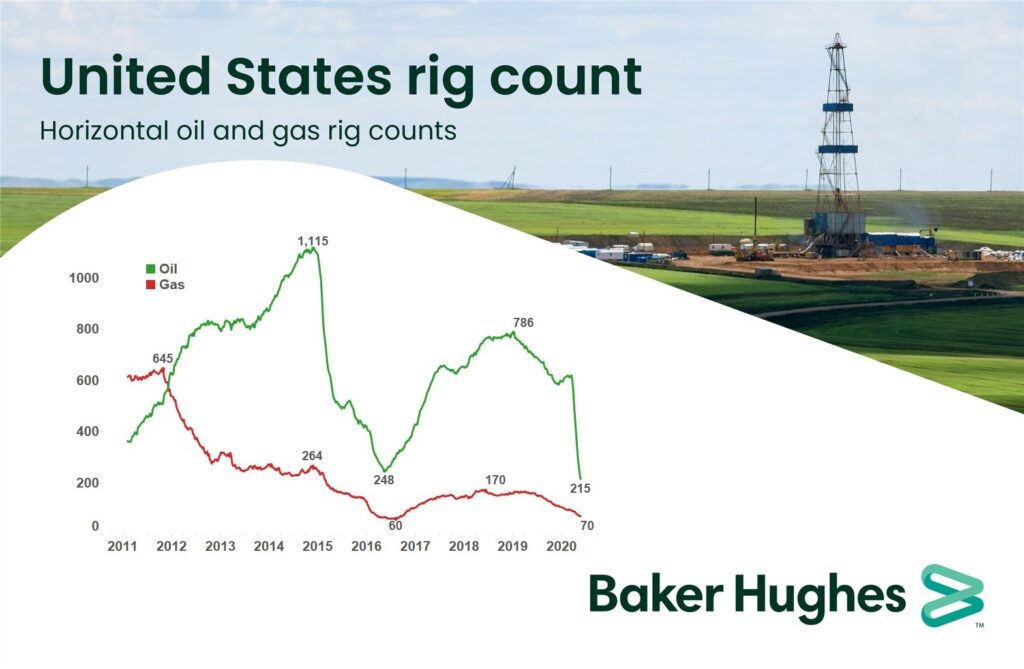

If COVID-19 doesn’t shut the economy down in the fall, we are at the beginning of the energy cycle. As you can see from the chart below, the number of oil rigs has fallen to 215 which is below the trough in 2016. First, we have seen oil prices bottom. Now we are seeing the glut of inventory fall. As we see demand come back, prices will rise. Next, the rig count will rise again which will let energy firms profit from higher prices.

Conclusion

Multiple rose 60% like the start of the last bull market, but the absolute number is much higher. Stocks are at a 22 or 23 multiple which is much higher than 14. We can’t ignore this even though Raymond James does.

Tech sector is in a big bubble which will cause the CLOU ETF to fall by at least 20%. This earnings season was filled with estimate cuts and withdrawals of guidance.

Good news is it can’t get any worse unless there is a 2nd wave. Q2 earnings will be bad, but guidance will likely be stronger. Rig count has fallen. It is below the prior low. Energy cycle is at its trough.