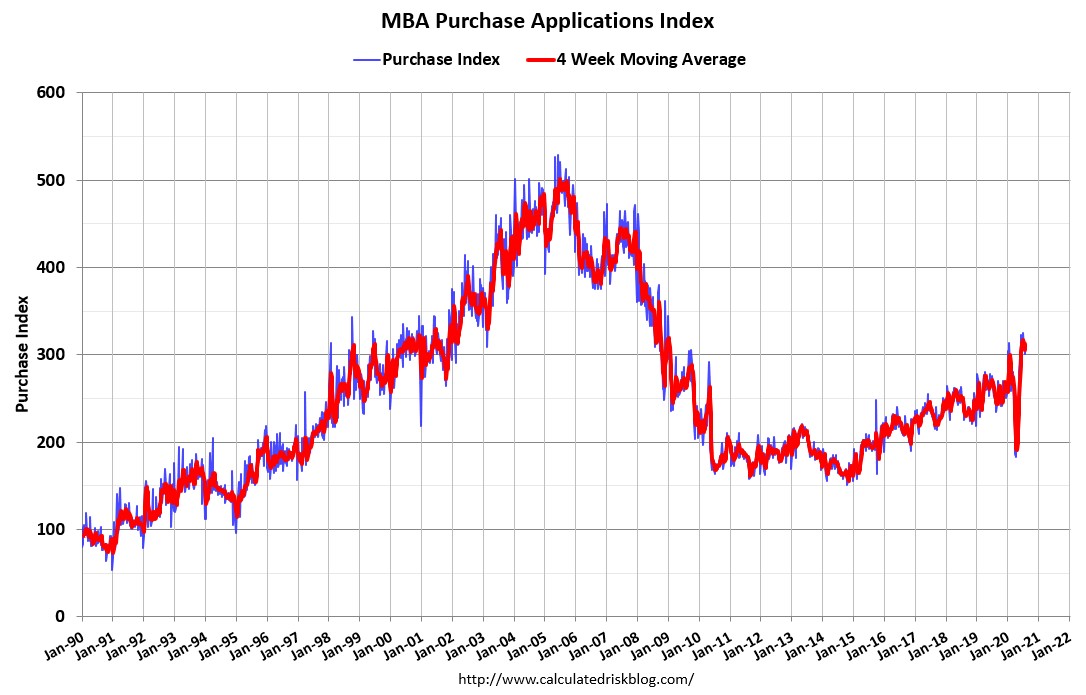

Housing Dips Slightly

Investors are obsessed with the latest data because the economy is changing faster than ever. This is especially important with housing data because official data is so delayed. We just got data on June and we’re now in August. July data won’t come out for a few weeks. It makes MBA weekly data more important. However, because the housing market has been so strong, people aren’t using it to gauge the economy.

MBA updates would be very closely watched if it wasn’t for the divergence between home buyers and the economy. Low rates spurred buying more than most expected. You needed to be extremely bullish to predict such a V shaped recovery in housing during the recession.

In the week of July 31st, there was a slight reversal. Composite index fell 5.1% weekly after falling 0.8%. Purchase index fell 1.8% weekly after falling 2%, but it was still up 22% yearly. It has grown 11 weeks in a row and is up double digits 10 weeks in a row.

As you can see in the chart above, purchase applications are about where they were last year. Refinances fell 6.8% weekly after falling 0.4%. It's unlikely that the 30 year fixed rate will fall much more even if the 10 year yield goes lower. We aren’t going to see banks pay people to take out loans no matter what. This about the floor. There aren't many people left who should refinance at these levels. The boom is mostly over.

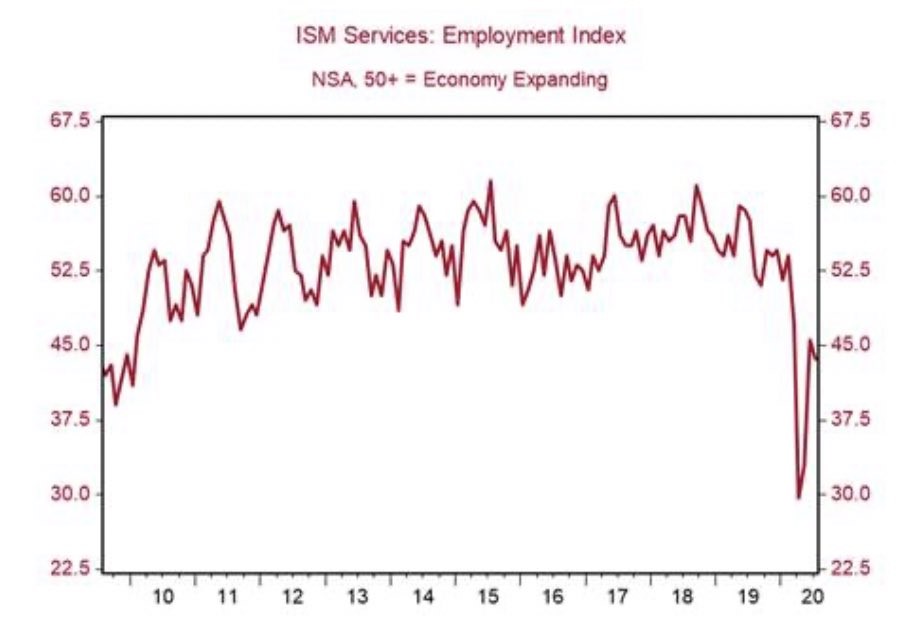

ISM Services PMI Improves

Just like the manufacturing report, the ISM services reading was strong. PMI rose from 57.1 to 58.1 which beat the consensus of 55. We are coming off the bottom, so it’s easier for diffusion indexes to rise above 50. In a normal situation this reading would be great.

That being said, this reading is pleasantly surprising because the economy seems to have slowed in July. Economists agree as this beat the high end of the consensus range which was 57.5. Economic reports are still beating estimates a few months into the recovery. That’s a great sign.

Business activity index was up 1.2 to 67.2 which is very strong. New orders index was up 6.1 to 67.7 which is a huge improvement. As you can see from the chart above, the employment index was down 1 to 42.1 which still signals a contraction. In the manufacturing report summary, we noted that production needed to increase because orders were strong.

Now, we can see that companies need to hire more workers because new orders for services were strong. July's labor report will be weak, but the August report will be stronger.

Current estimate is for 2 million jobs created and a 10.5% unemployment rate. That’s way too positive. A more realistic estimate is that there were 100,000 jobs lost. It’s weird to hear me say something negative about an economic report because many are bullish on this recovery.

This difference exists because some are bullish on the future, but were bearish on July a few weeks ago. At this point, July doesn’t matter to me or the market. That’s why the small cap value index is up 13.3% since July 9th.

Just like the manufacturing report, supplier deliveries and inventories fell which is a good sign. Their indexes were down 2.3 and 8.7 points to 55.2 and 52. They suppressed the headline PMI which is the opposite of the recession in which the PMI was pushed higher. That’s why it was consistent with such high GDP growth in relation to what was reported in Q2. This report is consistent with 3.3% GDP growth. Atlanta Fed Nowcast is predicting 20.3% Q3 GDP growth. That’s because of the easy comp.

12 industries reported growth in new orders and 2 saw a contraction. A retail trade firm stated, “Retail sales have continued to increase month over month, likely due to the general reopening of the economy. Mask mandates have been put in place for almost every market we operate in, causing an increased need for supply of masks for employees and customers.”

Retailers are doing relatively well because virus transmission in stores is low. It’s not nearly as problematic as indoor dining at restaurants.

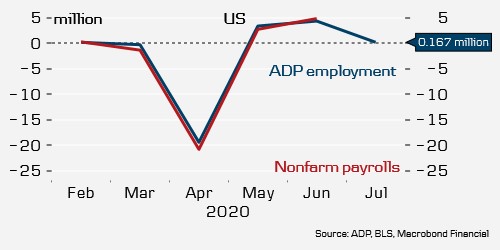

ADP Misses Estimates Wildly

In the past few weeks, we have been predicting a very weak BLS report. ADP report confirmed my expectations. As you can see from the chart below, there were 167,000 jobs created which missed estimates for 1.888 million and fell from 4.414 million in June. This missed the low end of the estimate range which was 750,000.

Normally, this would be a great report, but it’s a sharp slowdown from June. The stock market ignored it Wednesday. Let’s see if the stock market ignores the weak July BLS report on Friday.

There were 63,000 jobs created by small firms and 129,000 jobs created by large firms. Mid-sized firms did the worst as they lost 25,000 jobs. Service providing sector added 166,000 jobs and good producing added 1,000 jobs. Service sector will need to power the unemployment rate lower.

Strongest industry was professional and business which added 58,000 jobs. That’s a good sign. Education and healthcare added 46,000 jobs. As people start going in for elective surgeries, hospitals will get healthy financially again.

Cases & Deaths Are Falling

COVID-19 situation is getting better every day. This is the lynchpin of my bullish argument for the economy. There were 55,148 new cases which was down huge from last Wednesday when there were 65,323 new cases. Investors are looking for the 7 day average of new cases to fall below the April peak.

7 day average is 58,024; it peaked at 32,471 on April 10th. Wednesday new deaths fell from last Wednesday which is a great sign. There were 1,311 new deaths this Wednesday and 1,465 last Wednesday. 7 day average of deaths has peaked. Investors are looking for it to fall below 1,000.

Remember, the intermediate term prediction is 300 by the end of September. We should know if another wave is coming this winter by October. Good news is by then treatments will be much better.