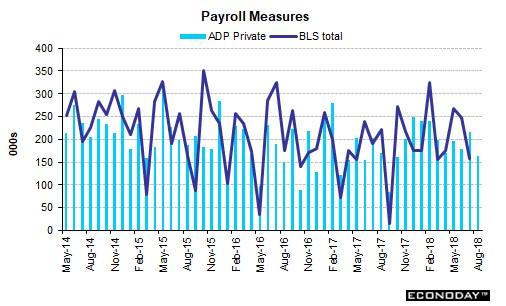

Private Sector Job Creation Misses Estimates

Private Sector - The ADP report is used to forecast the BLS monthly jobs report. In May and June the ADP report was below the BLS report. Therefore, when it came in strong in July, economists were expecting a blowout BLS report. Instead, it missed estimates.

If the BLS number comes in below the ADP report for August, it will be a problem. The ADP report showed there were only 163,000 jobs added as you can see from the chart below.

The consensus was for 182,000 jobs created. This report came in below the lowest estimate which was 170,000. The July report was revised lower from 219,000 to 217,000.

This wasn’t a bad report, but the slight weakness signals the labor market might not have much slack left. 163,000 jobs created is still above population growth, but it is closer than the previous months.

After 4 straight months of at least 200,000 jobs created, five of the past six months have seen less than 200,000 jobs created.

The biggest weakness in this report came from small businesses as they created 52,000 jobs in July and only 21,000 jobs in August. There were only 9,000 jobs created by firms with 1-19 employees.

Other small businesses with 20-49 workers added 12,000 workers. Good producing small firms added 1,000 jobs and service-providing small firms added 20,000 jobs.

Private Sector - This information is in stark contrast with the amazing NFIB small business reports.

The August ADP report showed mid-sized firms did well as they added 111,000 jobs. Large firms with 500 or more workers added 31,000 jobs. Goods producing firms added 24,000 jobs. Manufacturing lead the charge as it added 19,000 jobs.

The service-providing sector added 139,000 jobs. The two best industries were professional and business & education and health which added 38,000 jobs and 31,000 jobs respectively.

Economists expect the August BLS report to show 195,000 jobs were created. They expect hourly earnings growth to increase to 2.8% year over year from 2.7% in July.

Since there were 157,000 jobs created last month, if there is another weak month of job creation, economists will fear the labor market is near being filled. Since the slack in the labor market is tightening and productivity growth is improving, I expect wage growth to accelerate.

If wage growth increases in the next few months, real wage growth will return because I expect year over year inflation to weaken in the fall as comparisons get tougher.

Private Sector - Challenger Job-Cut & Jobless Claims

The August Challenger Job-Cut report showed there were 38,472 job cuts in August which was up from 27,122 in July. This was still a historically low number of layoffs.

The most layoffs were in industrial goods, then consumer products, and then retail. This report reflects a healthy labor market.

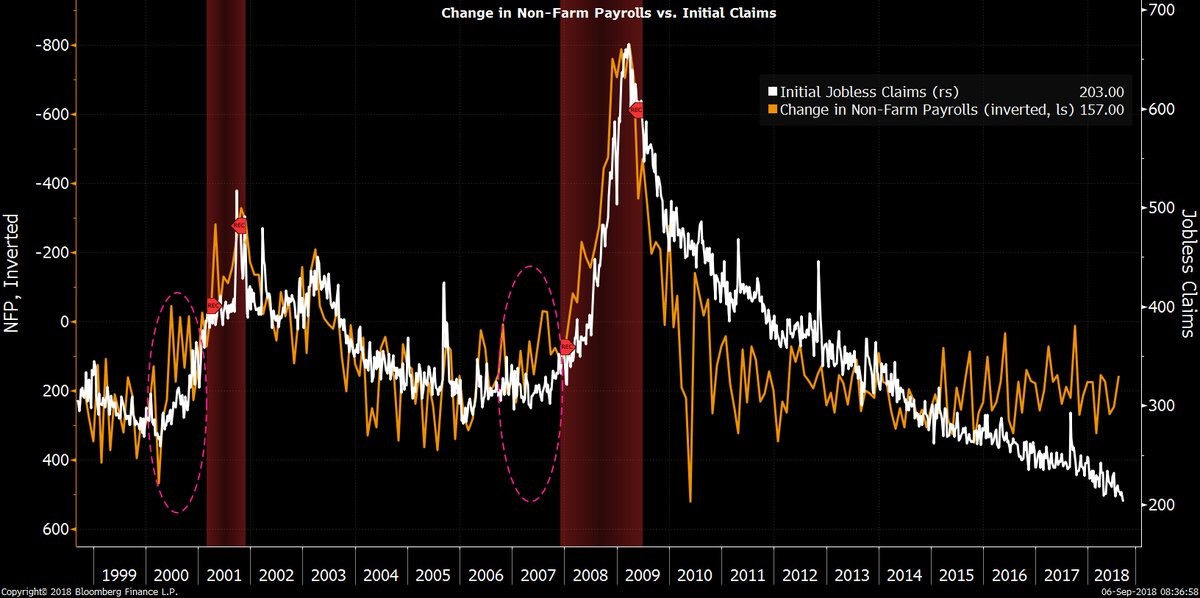

As you can see in the chart below, the jobless claims report showed 203,000 claims which is down 10,000 from the prior week. It beat the consensus for 213,000.

The 4 week average fell 2,750 to 209,500. Both the weekly report and the 4 week average showed the lowest claims since the first week in December of 1969 when the labor market was much smaller.

Continuing claims were down 3,000 to 1.707 million; the 4 week moving average fell to 1.719 million which is the lowest since the first week of December in 1973.

The unemployment rate for insured workers is 1.2%. California, Kansas, Maine, Puerto Rico, and Virginia estimated their results, so they may be revised. Either way this report signals the labor market is strong.

Based on the jobless claims alone, I expect the BLS report to show over 300,000 jobs added. However, the chart shows the two metrics have deviated in the past few quarters.

Private Sector - Productivity & Costs

As I mentioned, workers should be getting real wage hikes in the next few months. Productivity growth is strengthening and inflation should fall because it will have tougher comparisons.

On Thursday, the revisions for Q2 productivity growth and unit labor costs were released. Quarter over quarter non-farm productivity growth was 2.9% which was the same as last quarter and met estimates.

Unit labor costs were down 1% which met estimates; this is below last quarter’s decline of 0.9%.

Output was up 5% in Q2 which almost doubled the 2.6% increase in Q1. Growth in hours worked slowed to 2% from 2.3% in Q1. Compensation growth was only 1.9% in Q2 which was lower than the 3.9% growth in Q1.

Real compensation growth was only 0.2% in Q2 which was lower than the growth of 0.5% in Q1.

This is a good report because output growth was strong. Real wage growth should strengthen in Q3 if output growth is maintained.

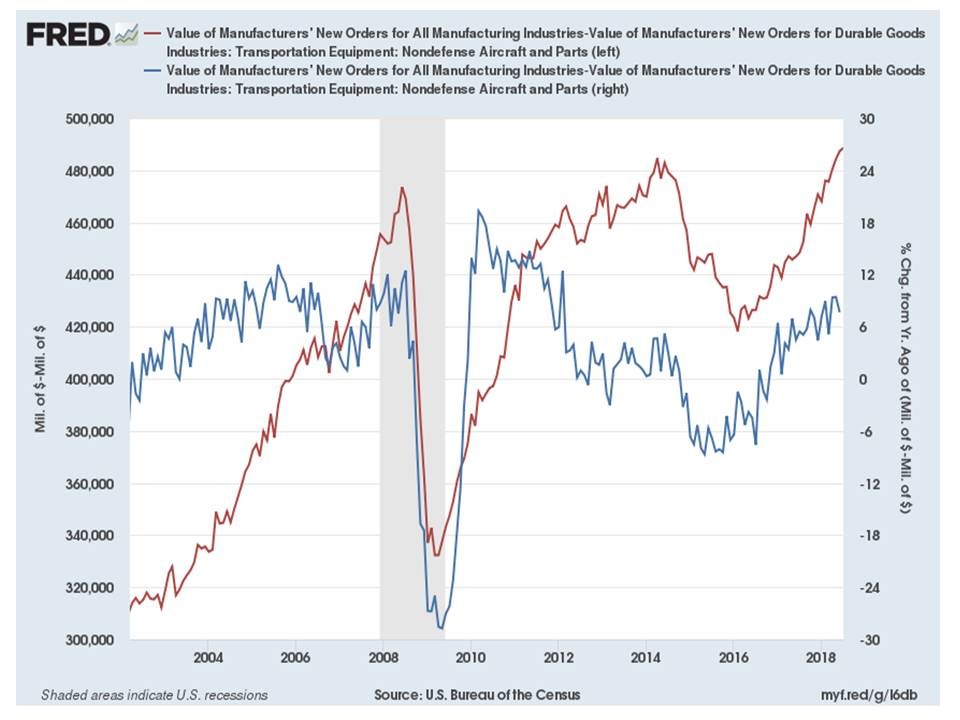

Private Sector - Factory Orders

July factory orders were down 0.8% from last month. This missed estimates for -0.7%. The June report was revised from 0.7% growth to 0.6% growth.

Core capital goods growth was strong despite this negative headline. Orders for non-defense ex-aircraft goods were up 1.6% month over month. This beat the 1.4% increase shown in the advanced durable goods report.

As you can see in the chart below, core capital goods orders growth is in the high single digits on a year over year basis. Core orders have surpassed the peak in 2014.

Non-durable goods orders were up 0.2% and durable goods orders fell 1.7%. There was a 35% month over month decline in commercial aircraft orders which manipulated the durable goods number.

There was solid growth in electrical equipment, machinery, mining and oil field equipment, motor vehicles, and ships and boats. Primary metals orders were up, and aluminum orders fell sharply.

Core capital shipments were up 1%. There was a 0.8% increase in inventories. Inventory investment will bolster Q3 GDP growth.

I can see Q3 GDP growth coming in close to 4% because of inventory investments and the bears claiming it wasn’t a good report because inventory building isn’t really growth.

The bears can’t have it both ways though because the lack of inventory building hurt Q2 GDP growth.