Q3 Ends On A High Note

With its modest rally on Monday, the stock market closed out the quarter positively, continuing this great year. S&P 500 moved closer to 3,000 which it has been stuck near for weeks.

Anyone who claims to look at stock returns on a yearly basis instead of year to date is about to change their mind as the market laps the decline late last year in the next 3 months. Frankly, I find the concept of looking at returns over the past year instead of year to date silly. 12 months is an arbitrary time frame just as how the year starts at an arbitrary time. I look at both.

Denying this great rally since late last year is foolhardy. Waiting until this December to recognize it doesn’t benefit you. Unless you’re a bear holding out hope that stocks will crater in the same manner as last year. Since Q4 of last year, the economic slowdown has progressed, the trade war has gotten worse, and the Fed has cut rates. Treasury yield have also fallen sharply.

October Could Be Problematic, But Q4 Is Usually Great

Based on price change only, the S&P 500 was up 13.07% in Q1, 3.79% in Q2, and 1.19% in Q3. The market has slowed down from its unsustainable pace. But it has still had a great year as it’s up 18.74% year to date. S&P 500 is down 1.62% from its record close. If all the October events turn out badly, we could see the market fall 10% and if they all turn out well, it will be at a record high.

There have been 9 years since 1950 where the S&P 500 has been up this much in the first 9 months of the year. The market finished higher every year and had an average annual return of 28%. It’s no surprise the market always finished the year higher after having such a great start and entering the best quarter of the year statistically.

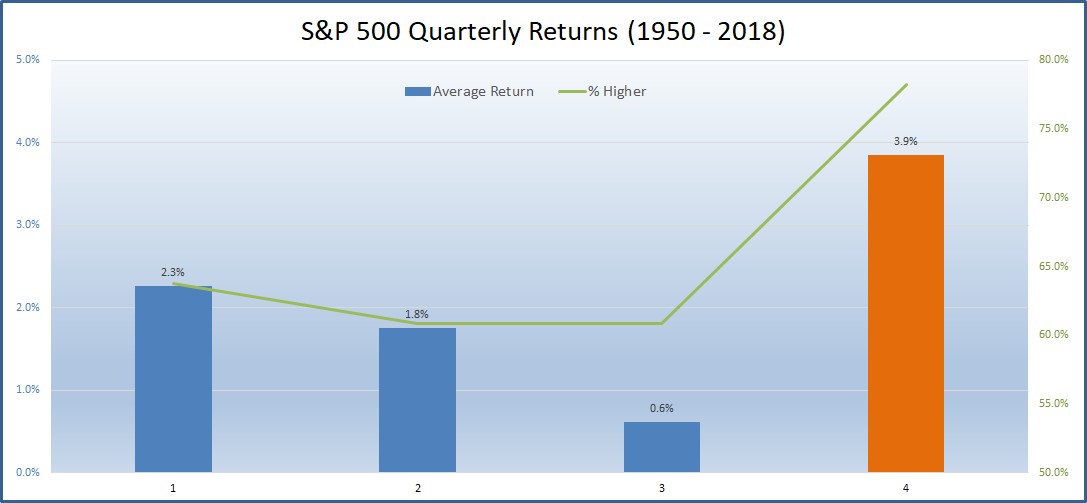

As you can see from the chart below, the S&P 500 has increased 78.3% of the time in Q4 and has an average gain of 3.9%. So far, the market has followed the average since Q1 was the best quarter and Q3 was the worst.

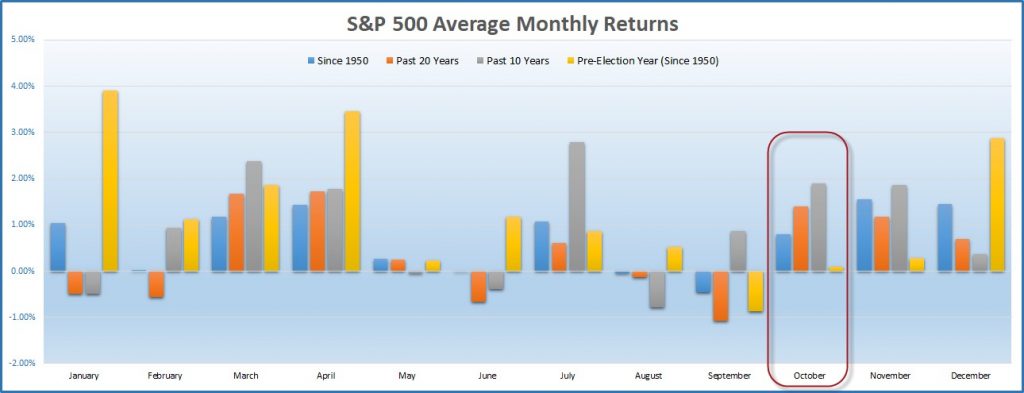

October is known for big surprises as October 2008 and October 1987 were very volatile months. However, as you can see from the chart below, October has had great returns in the past 20 and 10 years. As the chart also shows, in pre-election years since 1950 October is a weak month. Typically, in the fall of pre-election years there are primary debates.

Maybe some investors get scared of the possible extreme choices before a more mainstream candidate gets picked in the following year. This month the market will need to deal with trade negotiations, the Democratic debate, earnings season, and the Fed meeting. There will also be the usual economic reports such as the labor report this Friday. Consensus is for 145,000 jobs created in September (up from 130,000 in August).

There will only be one Democratic debate as all 12 candidates will be on one stage. It will be on the 15th. I’m guessing (rightly or wrongly) the lower polling candidates will get few questions as the major candidates square off. Even though Warren was down by 11 points in the latest Politico poll, she gained one point. So Biden’s polling average fell to a cycle low 6.3%. It will be interesting to see how Warren does in the debate as the rising star. She will be asked more (potentially tougher) questions and other candidates will challenge her more.

Specifics Of Monday’s Rally

S&P 500 increased 0.5% to 2976 on Monday. It has been near 3,000 for almost a month now. News events set to take place over the next 3 weeks will likely change that. Nasdaq rose 0.75% and Russell 2000 was up 0.19%. VIX fell 0.98 to 16.24. I expect it to touch 20 this month. CNN fear and greed index only increased 2 points to 54 which is neutral. The market is less than 2% from its record high and investors are neutral. That’s quite something.

Only down sectors were energy and the financials which fell 0.75% and 0.11%. Energy sector fell because Saudi Aramco announced it restored full oil production following the September 14th attacks. It also fell because of weak Chinese economic data.

Best sectors were tech and healthcare which rose 1.04% and 0.9%. Maybe healthcare liked the Politico poll showing Biden up by 11 points on Warren. Utilities were up 6 basis points. That sector has had a great year. As you can see from the chart below, the sector’s PE ratio is 21.8 which is the highest in at least 30 years. That’s a growth PE for a sector with little growth. If you think rates will rise, this sector is a great short.

The Coming Fed Rate Cut

Last 4 days of this week are interesting because each day multiple Fed members speak. The week will be capped off with Powell’s speech on Friday at 2:00 PM. These speeches will move the Fed funds futures market. Currently, there is a 41.2% chance of 1 cut and a 58.8% chance rates are kept the same this month.

That’s a high level of uncertainty for a rate decision in just 29 days. We will likely get much more clarity in the next 1-2 weeks. I think there’s more likely to be a cut in December than October, but the decision will depend on the September labor report and the trade negotiations. There is no certainty as of today.

Conclusion

Q4 usually a great quarter and October has recently been a great month. However, October has had low returns in pre-election years and there will be a heavy dose of news events this month. At the end of the month, we will know what the Fed did, have a better idea of who will win the Democratic primary, know most of the results of Q3 earnings season, and know if a trade deal is coming soon. It will be a fun month for traders.