October Core CPI - Neutral Rate Holds The Policy Key

Core inflation is starting to decelerate like many expected. Some economists are even projecting the cycle peak in inflation has occurred.

Inflation will likely fall in the next few months along with oil. If you think the cycle peak in inflation has occurred, then it implies you’re bearish on the economy. This cycle has been so long that there have been several inflation peaks. Fed raising rates in this environment makes no sense.

The Fed thinks inflation will regain momentum next year.

A key point to realize is the Fed’s goal is to have consistent 2% inflation. In this cycle, it has only stayed near 2% temporarily when it has easy comparisons. There haven’t been 2 year stacks of 4% core inflation.

Even though inflation is disappointing, you can argue that the Fed is simply trying to normalize rates.

The million dollar question is where the neutral rate is. Hawkish policy is a mistake. But it’s not clear if this rate hike in December pushes rates into that territory.

That’s where rates slow the economy. Personally, I think monetary policy will slow growth in 2019. If growth slows, it will difficult to tell if it was caused by monetary policy because there are other negative factors which will also weigh on the economy.

The only reason to cause a recession with rate hikes if you think inflation is a big problem. There needed to be a recession after the housing bubble because housing prices needed to become affordable again. They needed to be especially affordable because the unemployment rate rose.

October Core CPI - Slightly Disappointing

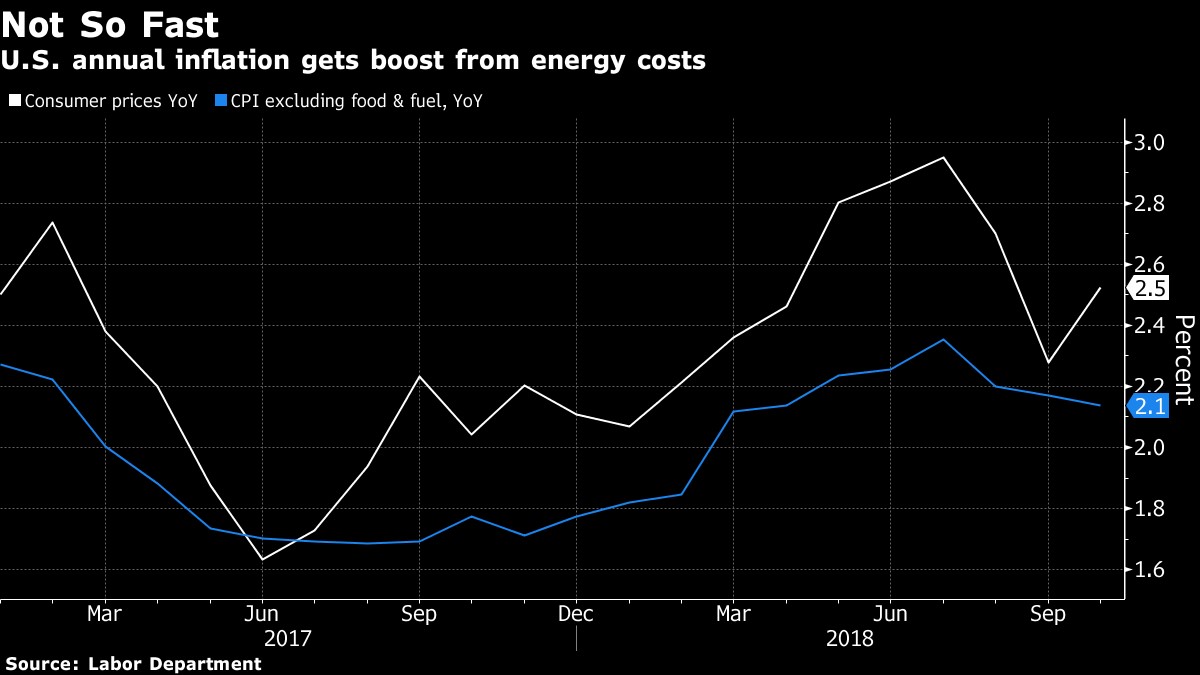

Month over month headline inflation was 0.3% which matched estimates and was above the 0.1% growth in September. It was 2.5% year over year which met estimates and was above September’s rate of 2.3%. This acceleration will be short lived because oil prices have been cratering. Energy increased 2.4% month over month in October. Gasoline was up 3%.

Core inflation was up 0.2% month over month which met estimates and was up from 0.1% in September. As you can see in the chart below, year over year core CPI was 2.1% which missed estimates and last month’s growth of 2.2%. That deceleration occurred because of the slightly tougher comparisons. The comparisons will come down in November and then ratchet up for several months. There’s a low chance core CPI will be 2% or higher in the first half of 2019.

October Core CPI - Housing inflation was moderate.

Since I expect home price growth to fall in the coming months, overall inflation will flatline as housing is its biggest component. Rents were up 0.2% and homeowner’s equivalent rent was up 0.3%. Medical services were up 0.2% and physician and hospital services were flat month over month. Food prices were down 0.1% and apparel was up 0.1%. Prices of new vehicles were down 0.2% which is the 2nd straight decline. However, used car prices were up 2.6%. That’s on top of a 3% decline in September, meaning there wasn’t much change in the past 2 months.

Energy was up 8.9% year over year. There will probably be slightly positive growth next month, but that depends where oil goes in the next few days. Natural gas prices have been increasing, so that might improve energy inflation. Food was up just 1.2% year over year and medical services were up 1.9% year over year. Housing was up 3.2% year over year which is the weakest inflation since February. That’s just the beginning as home price growth has barely started to slow. We could easily see below 1% inflation if the housing market turns sharply lower in the next few quarters.

October Core CPI - Potential Inflation

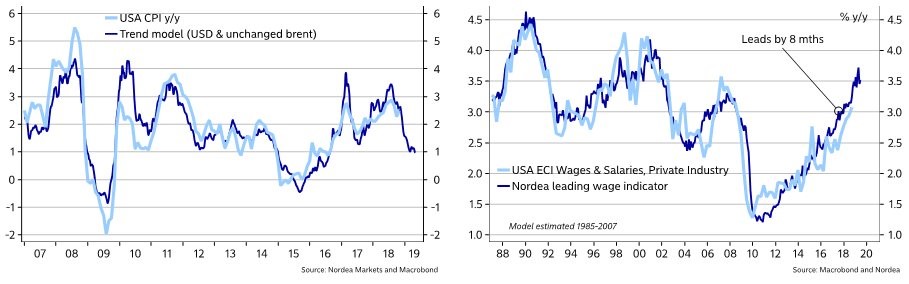

The good news about this inflation report is real hourly earnings growth was 0.7%. When the decline in gas prices is calculated, real wage growth will explode. As I have been forecasting, retail sales growth this holiday season should be great. As you can see from the chart on the right, the Nordea leading wage indicator expects private ECI wages and salaries growth to be about 3.5% in the next year. If the labor market stays strong, real wage growth will be amazing next year. Weakening global growth and the Fed hikes could ruin the party. As you can see from the chart on the left, if the U.S. dollar and Brent crude oil stay where they are, year over year CPI growth will fall to 1% in 2019. As I mentioned earlier, home prices are also weakening which will further pressure CPI. This is the perfect storm for declining inflation.

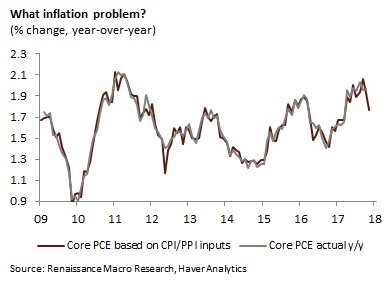

Inflation is going to decelerate in the next few months. The October PCE report will be released November 29th. As you can see from the chart below, you can predict core PCE inflation by using PPI and CPI inputs. Because the PCE is so late, we have almost all the data on the reporting period. This explains why there is almost never a big surprise in this report. A miss by 0.1% is a big deal. Renaissance Macro used these inputs to project year over year core PCE growth of 1.8% which is below the Fed’s target of 2%. The PCE inflation reading includes medical payments made on the behalf of customers. Therefore, medical inflation in the PCE report will be weaker than in the CPI report.

October Core CPI - Conclusion

Core CPI already started to slow. It signals October core PCE inflation will be only 1.8%. The Fed is about to raise rates in December even though it’s possible inflation may have peaked for the cycle. If the Fed is going to hike rates until financial conditions become stressed and the unemployment rate increases, the stock market is going to face a world of pain in 2019. There will probably be a recession after the slowdown gets underway. The Fed rate hikes increase the possibility a recession will occur. The economy has never experienced a slowdown in this cycle while the Fed was hawkish. The first slowdown had QE and ZIRP. The 2nd slowdown occurred after there was only one rate hike.