North Korean Summit Ends

The stock market didn’t have much of a reaction to the North Korean summit on Tuesday in Singapore, but that could be considered a good thing as the missile launches that occurred last year won’t return and hurt stocks in the intermediate term. I was wrong to imply everything would be done prior to this meeting, but correct to imply not much other than pleasantries would occur at the actual meeting. The new reality, which is now clear, is that this was the first step towards negotiations between the two nations. The hope is further meetings can hash out the issues over time. The problem is it’s far from a guarantee that this first step will lead to a peaceful Korean peninsula.

The biggest news coming from the summit was that the regular military exercises America holds with South Korea will be ended because they are expensive and provocative. Furthermore, Trump welcomed Kim to a meeting at the White House in due time. In return, North Korea promised to denuclearize; the one caveat is it wants the entire peninsula to do so. Secretary of State Mike Pompeo will be working on further negotiations to be sure North Korea fulfills its promises. Even though North Korea is said to be destroying a major missile engine testing site, the sanctions on the country remain.

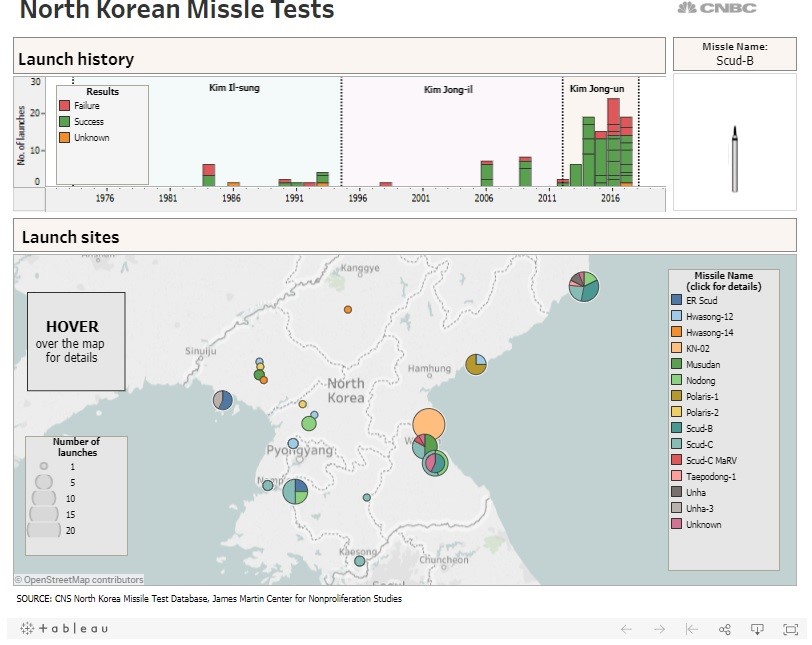

Peace is far from a guarantee, but future flare ups have been taken off the table for now. The table above shows the recent increase in missile tests in the past couple years which has riled markets. This means there’s no upside catalyst for stocks, but there’s also no downside catalyst either. That’s good news because American equities don’t need North Korea to boost prices; they have strong earnings growth and a strong economy to do that.

CPI Meets Estimates

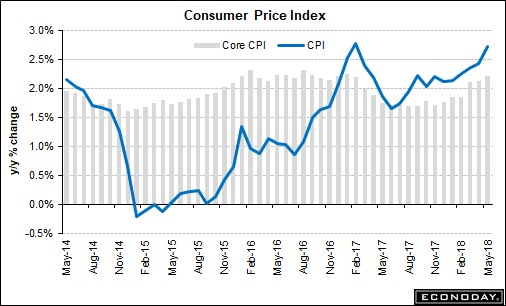

Even with the Fed meeting, ECB discussions about ending QE, and the North Korean summit, the most important event of the week may have been the May CPI report. All of the numbers came in as expected. Month over month CPI was up 0.2% and month over month core CPI was up 0.2%. As you can see in the chart below, year over year CPI was up 2.8% and year over year core CPI was up 2.2%. The cycle peak is 2.3% core CPI growth, so core CPI is much closer to its peak than core PCE. That point will be corrected if the May PCE report, which will be released on June 29th, comes in better than expected.

Don’t get excited by the CPI growth because 69% of the change was caused by energy price increases. Oil remains in the mid-$60s as traders wait for the OPEC meeting on June 20th-21st. Even if oil goes up further, it’s not a big concern in terms of monetary policy. We’d need a big spike to hurt most stocks and help energy names. Gasoline increased 1.7%, but the other segments increased less which is why year over year core CPI was only up one tenth from the previous month. Rent and owners’ equivalent rent were up 0.3% which is a moderate increase. Remember, the core PCE growth needs housing costs to increase to get to a 2% year over year improvement.

Medical care and hospital services were flat outside the increase in related commodities. New vehicle prices were up 0.3% and insurance was up 0.4%. There was a 1.9% decline in airfare costs and no change for apparel. Used car costs were down 0.9%. You can see the used car prices in year over year terms in the chart below. As you can see, the prices have been mostly flat after a spike in 2010 and 2011 due to the easy comparisons in 2008 and the first half of 2009.

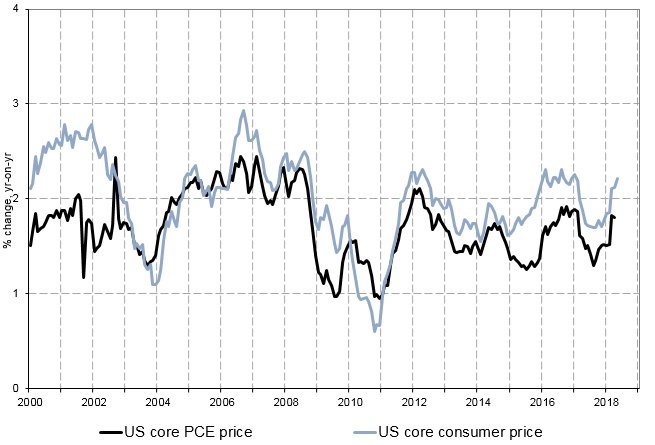

The big question is how core CPI gains translate to core PCE gains. As you can see in the chart below, the year over year core CPI was the highest since January 2017. Getting specific, this increase is 9.41 basis points below the cycle peak which was February 2016. Investors who thought the economy was peaking in 2016 and inflation was about to be a problem because it was late in the cycle were sorely mistaken as inflation never reached that point again and economic growth recovered in the 2nd half. February 2016’s inflation of 2.3% was helped by the easy comparison in February 2015 as inflation was only up 1.7% in that month. This current report has almost the same comparison as inflation was 1.7% in May 2017. There are relatively easy year over year comparisons for the next 9 months. I wouldn’t be surprised if year over year core CPI is the highest of this expansion in the next 4 months, which is when the easiest comparisons are.

Year over year core PCE is in a similar situation except it’s further off its cycle high. It’s about 30 basis points from the peak in March 2012. The bottom in core CPI was rounded in 2017, while there was a sharp spike down in core PCE in 2017 which means the year over year comparisons will get much easier until August. Starting in September, inflation should moderate. The Fed knows this which could be one of the reasons why it stated it won’t go crazy if inflation gets above 2%. In this expansion, the bouts of inflation haven’t lasted long. We’ll see if this time is different because wage growth pushes it up.

Conclusion

The North Korean nuclear situation has calmed down and core inflation isn’t rising out of control. Therefore, the Goldilocks situation for stocks will continue. I expect this situation to remain in place as long as the Fed doesn’t change its posture and decide to raise rates much more quickly. The economy will fall into a recession in the next 2-3 years, but there’s no need to accelerate that timetable when we have inflation below the 2% target. I will be bullish on stocks until the Fed really presses on the brakes hard.