No Rate Cuts - Earnings Season Is Almost Over

No Rate Cuts - Earnings season isn’t completely over and the rate of change of analysts’ estimates always matters. However, now that most firms have reported their Q1 results, investors’ focus will shift to economic reports. To be clear, it’s great that earnings estimates were beaten by a high amount and that Q2 estimates didn’t crater like last quarter.

However, economic reports haven’t been good recently. They show low growth and have mostly missed estimates. We can’t ignore this slowdown. Stocks can’t have an uninterrupted rally with the economy weakening. I expect the economy to improve in Q4, but I can’t be bullish on stocks if that improvement is already more than priced in.

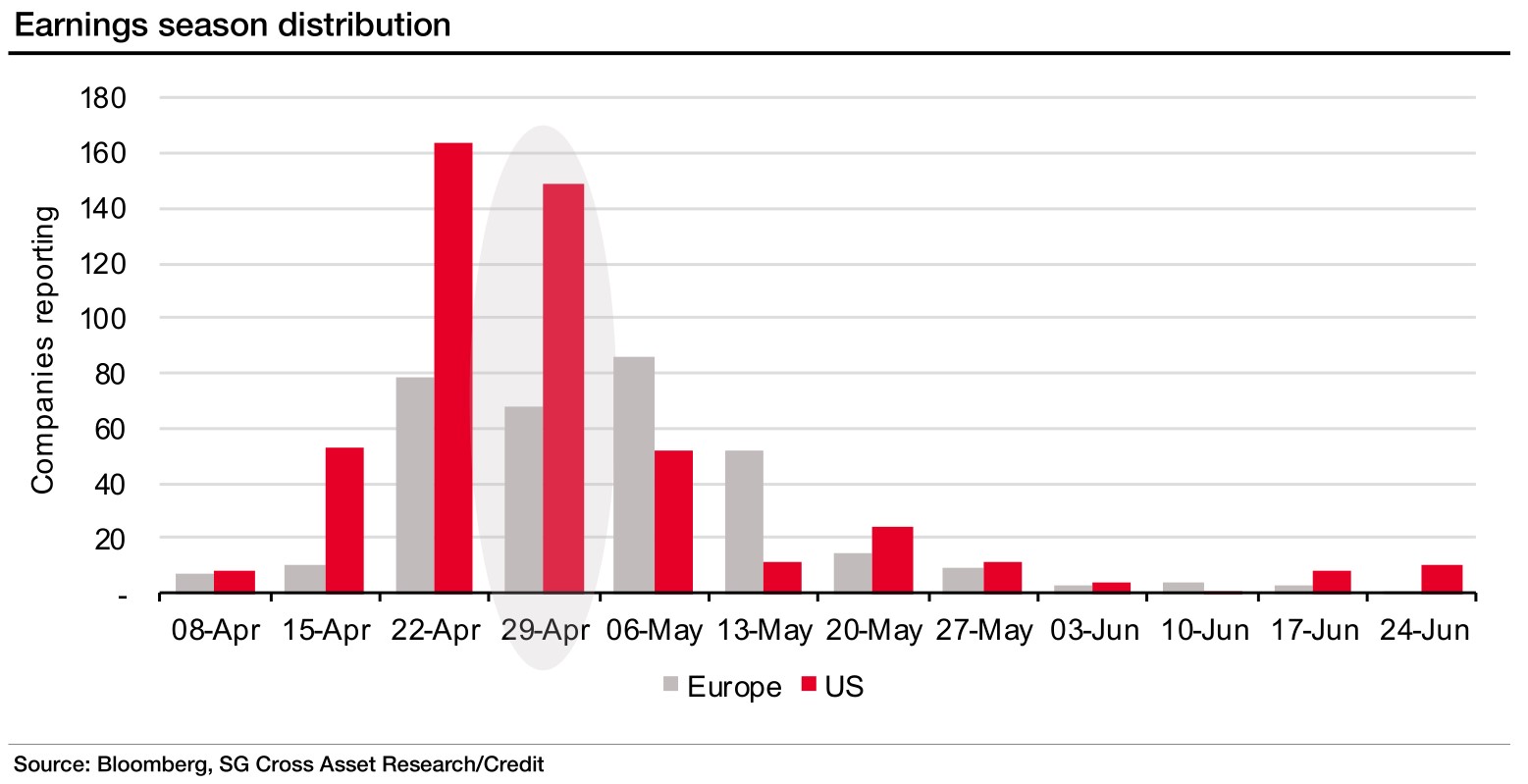

This has been a good earnings season. As of Wednesday evening, 333 S&P 500 firms had reported earnings. 77% of these firms beat estimates on 7.2% growth. 61% beat sales estimates on 4.4% growth. This week the sales growth beat rate improved.

As you can see from the chart below, this past week was the 2nd biggest week for American earnings. Next week there is a drop off; the following weeks only have a few earnings reports. It’s not as if the remaining 33% of earnings reports don’t matter; it’s that because they will gradually come out, they won’t dominate the market. The chart shows next week is the peak of earnings season for European firms. Keep that in mind if you see a divergence between European and global stocks.

No Rate Cuts - No FOMC Dissent

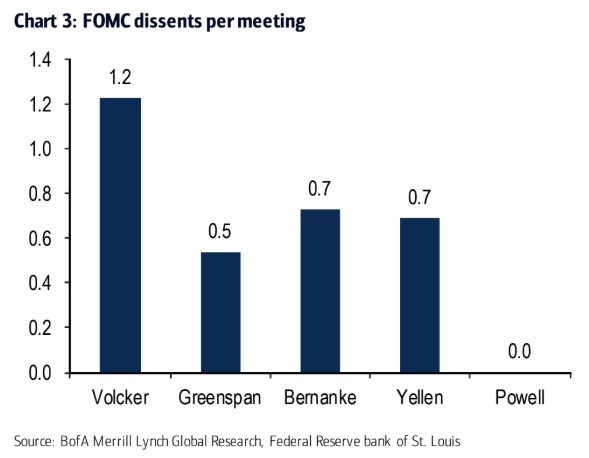

It’s not an exaggeration to say there hasn’t been any disagreement at the Fed since Powell became chair early last year. As you can see from the chart below, on average Yellen had 0.7 dissents per meeting and Powell has had zero. At this point in his tenure, it’s fair to say there have been a few tough decisions.

The toughest one was probably when the Fed raised rates in December during the economic slowdown and stock market crash. It was also difficult for the Fed to turn dovish late December after that rate hike. However, that wasn’t something members voted on. You can say members vote with their mouths whenever they give a policy speech or do an interview.

A takeaway from this chart is the Fed isn’t leaning in a different direction than how the majority voted because everyone has been on the same page. It’s fair to say that the number of votes on a certain policy decision is in itself forward guidance.

The fact that no one voted to cut rates in May tells us the Fed isn’t close to cutting rates. That was reinforced by the statement and the forward guidance. Since the Fed started hiking rates, core PCE inflation has only been above 2% once. Low inflation hasn’t stopped the Fed from hiking in the recent past and it won’t cause the Fed to cut rates this year.

No Rate Cuts - Weak Home Price Growth

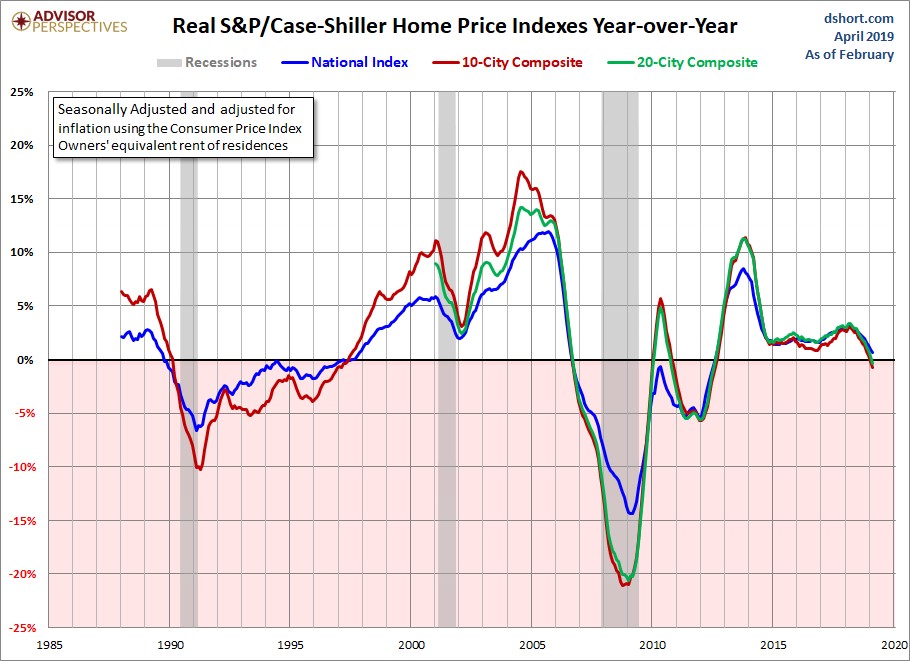

Investors have been calling for an improvement in the housing market for a few months now. Latest Case-Shiller home price report saw the 20 city price index’s growth rate fall to the lowest point since August 2012. However, keep in mind this report was from February, so it doesn’t necessarily mean my thesis that the housing market will recover this spring is incorrect.

Specifically, the national home price index was up 4%. The 20 city non-seasonally adjusted yearly price growth was 3% which fell from 3.5% and missed estimates for 3.2% growth. As you can see from the chart below, the 10 city and 20 city composite real price indexes fell on a yearly basis.

Hottest city was Las Vegas which had 9.7% price growth. However, even it has fallen from grace as its price growth peaked at 13.8% in August and has fallen every month since. Denver, which was once one of the hottest cities, saw its price growth fall to 4.6%. Its price growth peaked at 8.5% last March.

Finally, Seattle had the steepest drop as its price growth was only 2.8%. That is down from the 13.5% growth peak in May of last year. That February growth rate was only a little above some of the weakest cities like New York. It was the weakest price growth since June 2012. It looks like its prices are about to fall on a yearly basis.

To be clear, the housing market can rebound this year even if some of the hottest areas lose steam. There’s no rule that says national home price growth can’t improve while some cities like Seattle see yearly declines.

No Rate Cuts - Pending Home Sales Index Improves

Good news is the Pending Home sales index showed sequential improvement in March. The index was up 3.8% to 105.8. That beat estimates for a 0.7% increase. Anytime the index is above 100, it means pending home sales are above the historical average.

Only the South’s index was above 100. Since it is so high and the largest region, it pulled the overall index above 100. The South is at 127.2 and had yearly growth of 0.7%. It was the only region to have yearly growth as the national index fell 1.2% year over year. Midwest had the steepest decline as it was down 5% yearly. Northeast’s 90.5 reading was the lowest of the 4 regions.

No Rate Cuts - MBA Applications Fall

The week of April 26th was another down one for purchase applications. Composite index fell 4.3% weekly on top of a 7.3% decline. Purchase index and the refinance index fell 4% and 5% on top of declines of 4% and 11%. Yearly growth in the purchase index was only 1% which is pretty terrible for the spring housing push.

March was a great month for the applications index, but April had lower yearly growth. It’s unlikely that the slight increase in rates from the bottom hurt demand because the average monthly 30 year rate was 4.14% in April which was 7 basis points lower than March’s average. If you’re curious, the average rate fell from 4.2% to 4.14% in the week of May 2nd.