New Home Sales Report - Strong New Home Sales

There was an interesting revision in the New Home Sales Report. Technically, the April new home sales reading missed estimates slightly. But this was still a great report. Positive revisions in the previous months far outweigh the slight consensus miss.

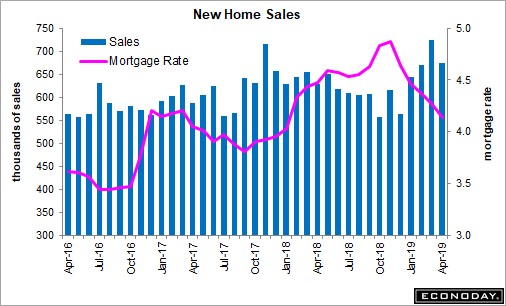

Specifically, April new home sales were 673,000 which missed estimates for 680,000. The previous two months were revised higher by a combined 39,000. That’s much higher than the 7,000 miss. March reading was revised from 692,000 to 723,000. Obviously, that’s a big change which is great in its own right. However, it’s even more important because that’s a new cycle high.

The median cycle peak in new home sales is 28 months before the next recession. That’s huge because the countdown had been going for 17 months prior to this new high. Therefore, the next recession could occur in 27 months instead of 11 months (28-17 = 11).

Clearly, medians aren’t always hit.

New Home Sales Report - There can be a recession at any time. However, it would be incredibly rare for new home sales to peak right before a recession. Housing is the leading indicator with the most lead time before recessions. The best hope for the bears is that the March reading is revised lower as it is only 8,000 above the November 2017 high. The February reading was just revised 8,000 higher, so it’s certainly possible.

Quarterly average of yearly new home sales growth is always negative before recessions. Q4 negative reading counts, but the longer yearly growth stays positive, the less power that indicator has. You can say the decline in interest rates saved the housing market.

30 year fixed mortgage rate fell to 4.06% this week which matched the low on the year. However, consumers still need to be in good shape to take advantage of declining rates. Eventually, when housing gets more affordable, it hits a point where demand picks up. That point was very early this time as yearly price growth hasn’t gone negative.

That pick up in demand occurred because the consumer isn’t leveraged and the labor market is solid. Plus, inflation’s decline has helped real wage growth.

The 3 month average of new home sales is 688,000 which is up 2.4% sequentially. That’s better than the 3 month average growth of 1.7% in existing home sales.

Both of those averages have improved since the drop in interest rates.

New Home Sales Report - Lucky for home buyers, rates appear to be staying low because of the trade war and the cyclical slowdown. Obviously, if the slowdown leads to an increase in the unemployment rate, even outright declines in home prices won’t help home buyers.

As for now, I think there’s a possibility real investment growth has a positive impact on GDP in Q2 after being negative for 5 quarters straight. The Atlanta Fed GDP Nowcast revised its Q2 GDP growth rate up from 1.2% to 1.3% because of the new home sales report. Its estimate for real residential investment growth improved from -4% to -1.6%. Another great new home sales report in June will make that impact positive.

Another positive from this report was the price growth as median prices were up 11.9% monthly and 8.8% yearly to $342,200. Yearly price growth was slightly more than yearly sales growth which was 7%. Sales were so strong that that supply fell 0.9% in April to 332,000. However, supply relative to sales increased from 5.6 months to 5.9 months.

Global Weakness

New Home Sales Report - I don’t love the Citi surprise index because it is highly sensitive to changes in economic reports. A slight slowdown which catches economists off-guard can cause this index to go negative.

As you can see from the chart below, the global surprise index has gone negative numerous times without there being a slowdown or recession. However, it’s worth noting how the index has been negative for 290 days which is the longest streak since at least 2003.

Usually economists get the drift that the economy is slowing by now. Obviously, this isn’t as bad as the 2008 financial crisis as the decline isn’t as deep. It troughed at about -100 in 2009 while it troughed at about -40 in this slowdown. Given how long the index has been negative, it wouldn’t be surprising if it goes positive in the next few weeks.

However, just because results beat lowered expectations doesn’t mean this slowdown is over.

Poor April Durable Goods Report

New Home Sales Report - The U.S. economy is weak and potentially headed towards the worst slowdown of this expansion. Next stop after that distinction is a mild recession.

April durable goods new orders report saw headline monthly growth of -2.1% which slightly beat estimates of -2.2%. However, this isn’t good news because March’s growth rate was revised 1% lower to 1.7%. Excluding transportation, monthly growth was 0% which again beat estimates by one tenth.

March report was revised 0.9% lower to -0.5%. Finally, core capital goods orders fell 0.9% which missed estimates for 0.1% growth. The March reading was revised from 1.3% to 0.3%. Yearly non-defense capital durable goods orders ex-aircraft growth was only 1.3% which is the weakest growth rate since January 2017.

The list of negatives is long. This isn’t a report I can explain away. Details match the headlines. Orders for primary metals have fallen 0.8% and 1.9% in the past 2 months. Fabrications orders were up 0.4% after falling 1.6%. Machinery orders were up just 0.1% after falling 2%.

Supporting all the negative data on autos, new vehicle orders were down 3.4%. Civilian aircraft orders fell 39%. The decline in civilian aircraft orders actually isn’t bad because this reading is always volatile and there were 737 cancelations because of the plane crash. Finally, civilian aircraft unfilled orders fell 0.3%.

New Home Sales Report - Conclusion

We are in opposite land where most of the economic data is weak except housing. Last year most of the economic data was strong except housing. Real residential investment growth is still expected to be negative in Q2.

But I wouldn’t be surprised if it ends up being positive since most of the housing reports from April and May were solid. Lower yields only help the situation.