Same Store Sales Growth Falls Further

As predicted, same store sales growth in the Redbook report is coming down. That’s because the hoarding is over. Undoubtedly when the economy recovers we will see higher growth, but we aren’t there yet. We are stabilizing along the bottom. We can expect the economy to start to rebound in May when most states start to reopen.

Specifically, in the Redbook same store sales report from the week of April 18th, sales growth was -6.9% which fell from -2%. Yearly sales growth will probably bottom in the next 2-3 weeks. People are still losing their jobs. Few jobs have come back yet. They will start to in May.

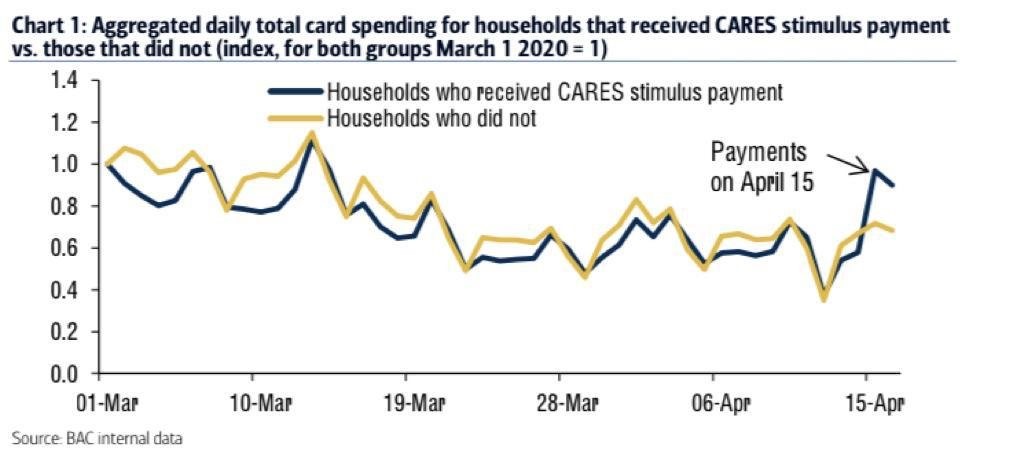

As you can see from the chart below, spending from those who received the CARES stimulus payment increased, while it’s still low for those who didn’t. Stimulus spending will likely be very temporary. However, it’s a good signal that spending at households who didn’t receive the check appears to be bottoming.

Bad news is that the people who have the most discretionary income didn’t receive help. Meaning, overall spending in the past few days likely was closer to the yellow line than the blue one. Watch spending from the rich and the upper middle class to have an idea of where the economy is headed.

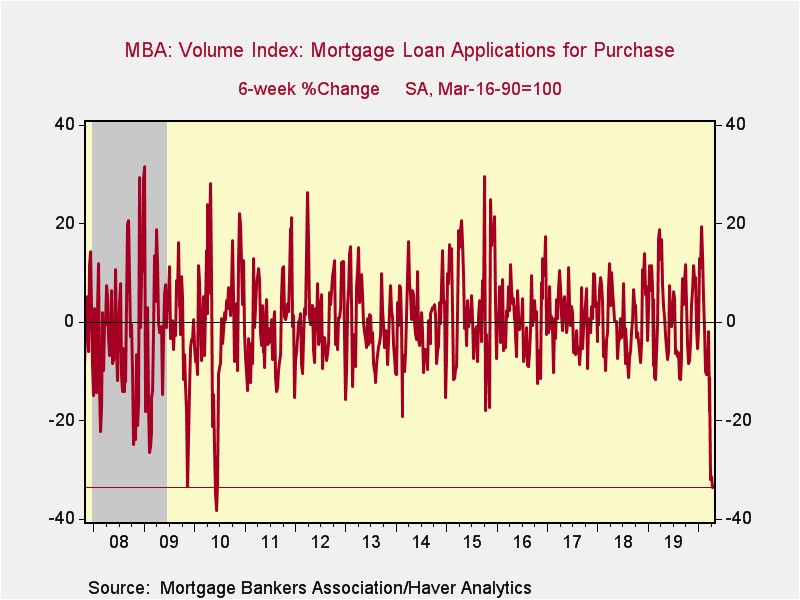

Mortgage Applications Stabilize At A Low Level

Mortgage applications have been plummeting as you’d expect. Good news is they may have found a bottom. After crashing for the past 5 weeks, the purchase index was up 2% weekly. It was down 2% in the prior week. Refinance index fell 1% after rising 10% . That's why the composite index was down 0.3% after rising 10%.

An increase in purchase applications was the first since the week ending March 6th. As you can see from the chart below, in the past 6 weeks the purchase index is down 33.6% which is the worst since 2010 when the homebuyer tax credit was unwound.

A decline in mortgage purchase applications probably sugar coats how bad this situation is. It’s not as if everything is normal besides some buyers pulling back. People can’t afford to make their mortgage payments. That’s because many people didn’t come into this situation with enough emergency savings.

Even though the consumer was in relatively good shape cyclically, it wasn’t in good enough shape to deal with losing all its income for an indefinite period. Even if you have a savings account with money set aside, it makes sense to avoid paying the mortgage to save money for food and necessities in the near term. People are very scared and uncertain.

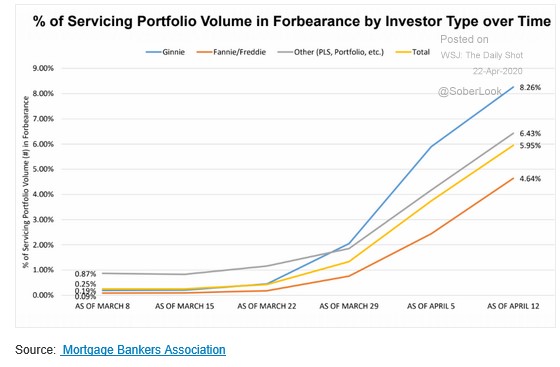

Mortgages Are In Forbearance

Even 3 months of savings might not make many people feel safe because of the potential for this shutdown to drag on. It will likely partially end this summer. But people don’t know when they will get their jobs back. That explains the chart below which shows the percentage of loans in forbearance.

As you can see, 8.26% of Ginnie Mae mortgages are in forbearance. Average is 5.95%. Hope is people can put the few months of payments they can’t make now at the end of their mortgage. If they had 9 years left on their mortgage, they can put it in forbearance for 3 months. Thus making the loan stay at having 9 years left instead of 8 years and 9 months.

Very Negative Corporate Debt Market

The stock market has gotten very cheap. When the market was down 33%, that priced in earnings falling to zero and then taking 7 years to get back to the pre-crisis trend. Many are betting takes 2 years to get back to the trend. Earnings this year won’t be zero (although they will be down double digits).

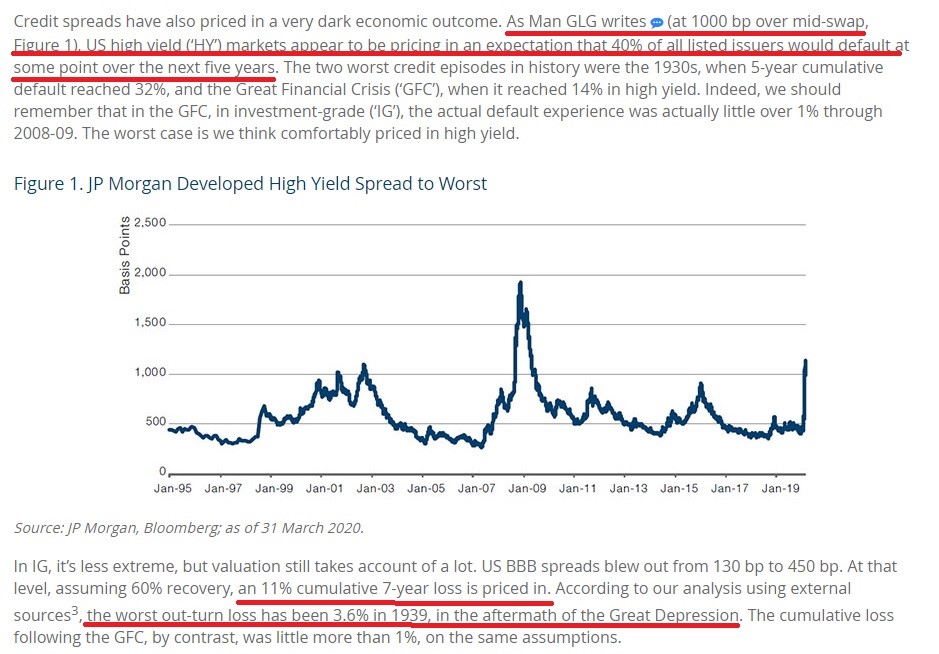

This situation is even more wild in the corporate bond market which makes the situation ripe for opportunities. High yield debt market is pricing in a 40% default rate over the next 5 years even though actual defaults from the great financial crisis were 14%. The situation might be worse, but not that much worse.

On the one hand, banks are allowing for some flexibility with covenants because of the extreme situation. On the other hand, many oil companies will go out of business. Energy sector dominates the high yield market. There needs to be a great flush of oil company bankruptcies to make the sector stronger. You can only buy the strongest companies like EOG and Chevron. They will survive and thrive in the next upcycle. It’s not just junk debt that’s pricing in a huge crisis.

Investment grade debt is pricing an 11% default rate over the next 7 years. In the great financial crisis, the default rate was 1% and during the Great Depression it was only 3.6%. It's highly doubtful that many defaults will occur in the investment grade category. Even though many companies are at the low end of that range and the economy has shut down.

There is great leeway for these companies as banks know these firms would normally be in fine shape if the economy didn’t shutdown. Plus, the Fed is buying investment grade debt. In my opinion, it’s virtually a free lunch to get long investment grade debt at those levels. Only thing that stops me from doing that is there are so many even better opportunities via common stock.

Conclusion

Our economy is in terrible shape, but we might be near as bad as it gets. Redbook same store sales growth is down and people are having their loans put into forbearance. Good news is spending and mortgage purchase applications might be stabilizing.

Despite the negatives, there are places to invest because of the low prices. Avoid energy stocks with high debt, but you can buy the majors. Investment grade debt overall is priced as if this will be worse than the Great Depression. Some economic reports might be as bad as the Great Depression. But investment grade debt will be fine because of flexibility with covenants and the Fed buying corporate debt.