Mortgage Applications - More Weakness In MBA Applications

The housing market weakened this summer. Home price growth is going to fall in the next few months. Affordability is a problem in many cities.

The latest housing data comes from the MBA mortgage applications index. This composite index was down 3.2% week over year in the week of November 9th. That’s on top of the 4% decline in the first week of November. Purchase index fell 2.3% on top of 5% weakness. The purchase index is at its lowest point since February 2017.

Refinancing index fell 4.3% on top of a 3% decline. That put it at its lowest level since December 2000.

Unadjusted purchase applications fell 3% from this week last year. The refinance share of mortgages increased 0.3% from the prior week to 39.4%. Average interest rate on 30 year fixed mortgages increased 2 basis points to 5.17%. That's the highest level since 2010.

Mortgage Applications - Redbook Shows Continued Strength

Retail sales and the labor market are lagging indicators. Meaning, by the time they show weakness, the stock market will likely be down over 10%.

Redbook same store sales report from the week of November 10th showed 6.1% year over year growth. The 6.5% annual growth pace is the strongest in a decade. Thus supporting the thesis that the economy is late cycle.

It sounds illogical that I’m expecting a strong holiday season for retailers. But that’s what happens when the leading indicators begin to show weakness. Especially if it happens while the laggards are still strong. This will be the last strong holiday shopping season in this cycle.

Mortgage Applications - Analyzing The NFIB Survey

Your opinion on the NFIB survey depends on your overall opinion on the macro economy. It’s tough to review. You can say the October index is at a 4 month low. Or you can say that it’s just 1.4 points below its record high in August.

On the negative side, when indexes fall from amazing to great, it’s very bad in rate of change terms. The economy is on its last legs. Fed is getting too hawkish and global growth is slowing. Any modest blemish on what was one of the shining parts of this cycle is a bad signal.

On the positive side, it was impossible for this index to keep making 45 year highs. It was a given that it would fall slightly. That’s irrelevant because it’s still extremely elevated.

It’s tough to say if falling 1.4 points equates to going from amazing to great. This is still one of the best reports ever. When you consider the fact that economic growth is weakening, it’s impressive small businesses are this optimistic.

Mortgage Applications - Politics appears to affect these results.

So I’m interested to see if the index falters in November because the Democrats won the House.

The best way to review if this indicator is weakening is to look at the details of the report. Overall index fell from 107.9 to 107.4 which was below the consensus for 108. It was also below the lowest estimate which was 107.5. I’m surprised that the estimates were this high.

Economists don’t fully realize an economic slowdown is in place.

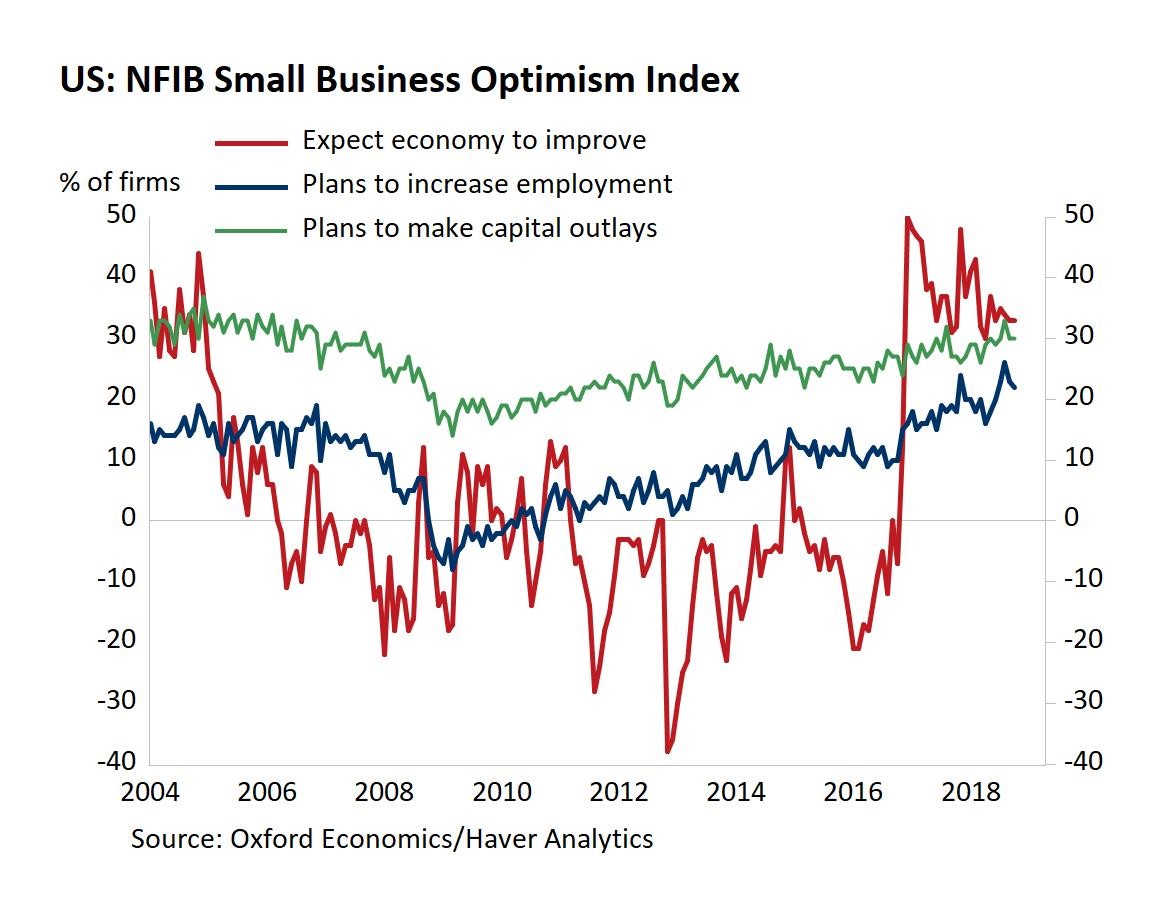

The chart below shows 3 of the 10 components of the index. While the NFIB is focusing on the 2 years of historic readings, I’m focused on where it will go in the next 6 months. That’s all the market cares about.

As you can see, the index measuring expectations for the economy to improve is well off its recent high. And plans to make capital outlays and the plans to increase employment are near their peaks.

In this survey, the weakest component was the net percentage saying now is a good time to expand as it fell 3% to 30%. Earnings trends fell 2% to -3%. The best component was the plans to increase inventories which was up 2% to 5%.

Overall, 5 components fell, 1 rose, and 4 stayed the same.

Mortgage Applications - There’s nothing dramatic in this report which shows a big change has arrived.

The most negative part is probably that the expectations for the economy to improve are way below the peak. That’s like how the current expectations index is much higher than the future expectations index in the consumer confidence report.

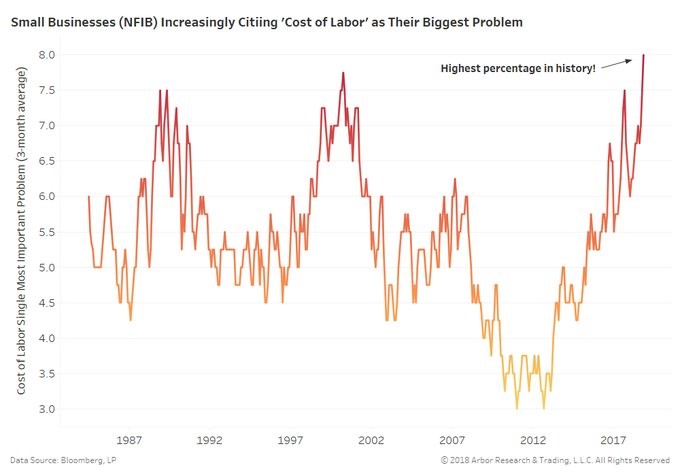

The part of this report that screams the economy is near the end of the cycle is the sentiment on the labor market.

As you can see from the chart below, the 3 month average of the percentage of small businesses citing labor costs as their biggest problem is at the highest point in the history of the 45 year survey.

Previous peak in the 1990s cycle preceded the 2001 recession. In Neel Kashkari’s speech this week, he suggested businesses should raise wages to attract workers if they are having a tough time finding them. That would hurt margins and push stocks lower.

A net 34% of small businesses reported raising wages and 23% said they have plans to raise them. It appears firms are following his suggestion.

Mortgage Applications - Confidence Review

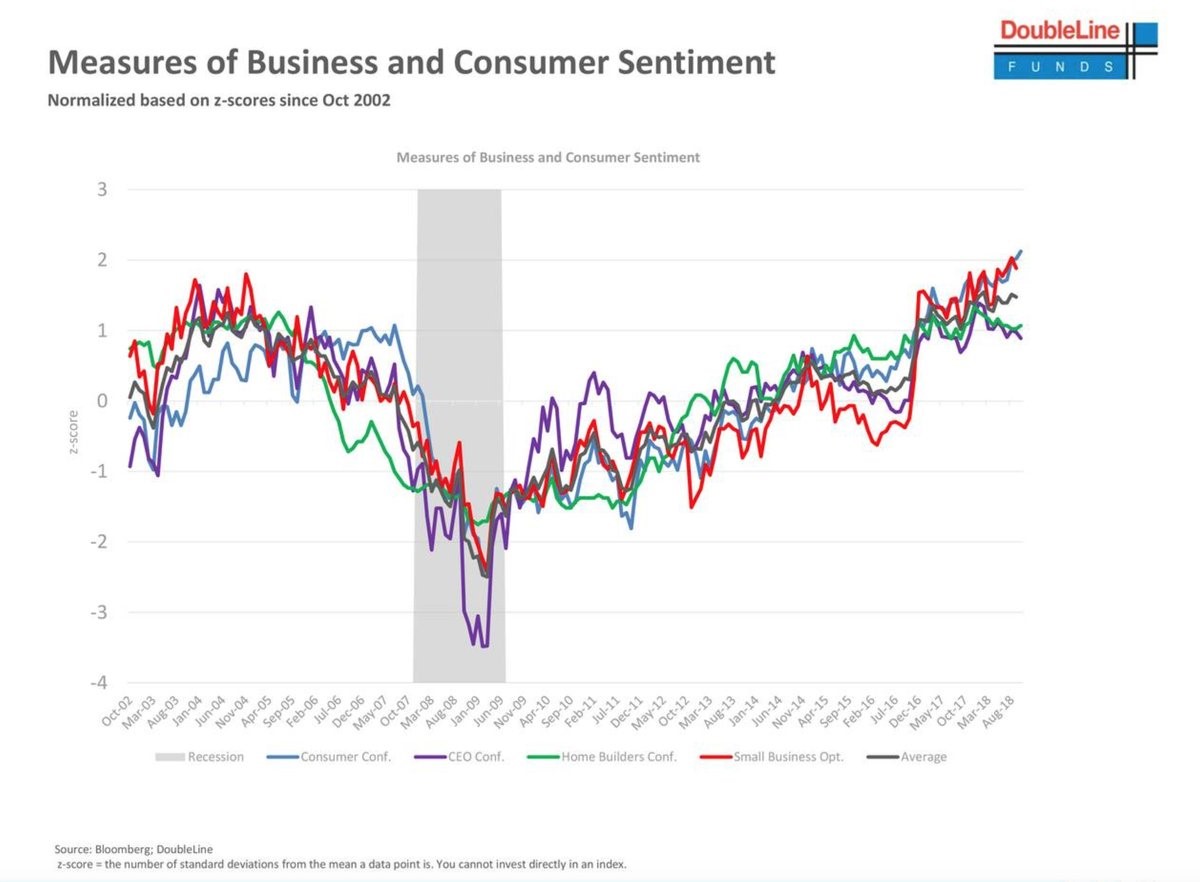

The chart below shows the z score of consumer confidence, CEO confidence, home builder confidence, and small business optimism since 2002.

As you can see, sentiment is diverging with homebuilders and CEO’s being less confident, while consumers and small businesses being more confident. Eventually, those sentiment indicators will converge. I think it’ll be lower.

Mortgage Applications - Conclusion

There are a lot of late cycle bells going off. The housing market is weakening; retail sales growth is strong. Small businesses are having a very tough time hiring workers. The labor market is tightening and wage inflation is increasing.

The 4 month low in the NFIB index could be nothing or it could signal sentiment is eroding.

This November report might show weakness because of political reasons.

If that’s the case, the index needs to be ignored. Even though my thesis would be confirmed, I can’t base a thesis around small businesses not liking Democrats.