On Monday, Tesla passed General Motors in terms of market cap, making it the highest valued automaker. This article isn’t about Tesla, but Tesla serves as a red flag for how out of whack valuations have become. Tesla isn’t even the leader in electric vehicles sales which is its niche. The firm lost $675 million last year, yet the market cap is above $50 billion. When a cursory look at the leading automaker shows such unbelievable results, it’s a sign of a bubble.

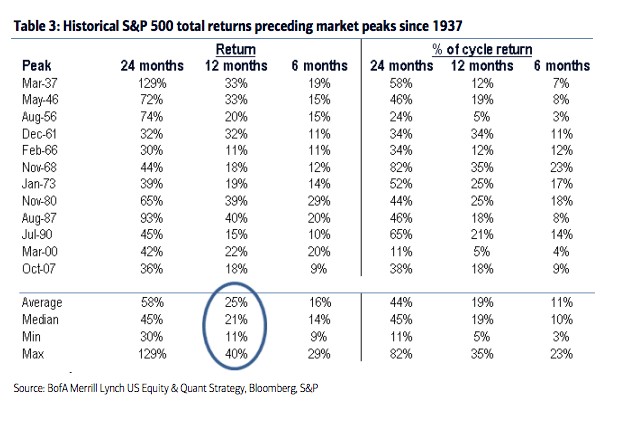

The chatter on Wall Street is that now is the time to buy stocks because we’re at the end of the bull market which is when stocks rally the hardest. Morgan Stanley’s chief equity strategist believes the S&P 500 will rally almost 30% in the twelve months because of this late-cycle phenomenon. The argument boils down to saying that there’s no rational reason stocks should go up, but at the end of previous bull markets there was irrational buying. Buying based on historical precedent isn’t a terrible idea at face value. As you can see from the chart below, stocks have performed great right before their bull market peak. The problem I have with this entire premise is there’s no guarantee stocks are twelve months from their peak. If they peak in three months, you’ll lose more than you make with this advice. Claiming that you know the exact point where stocks will peak shows a dangerous level of arrogance. It’s the same arrogance which has cost the bears dearly in the past few years if they made short term negative bets on the market.

This point isn’t to criticize Morgan Stanley too harshly because it’s tough to invest in bubble times. There are a few bearish bloggers who write about Tesla who have accurately predicted its financial metrics, yet have gotten the trade wrong. Fundamentals don’t matter until they do when there’s a bubble. Both shorting and owning momentum stocks like Tesla as well as the S&P 500 index fund have become risky strategies. One final point I have is I highly doubt that if stocks rally the 25% shown in the chart above, that Morgan Stanley will go negative on stocks. It would be tough to make a proclamation that at that exact point stocks will crash.

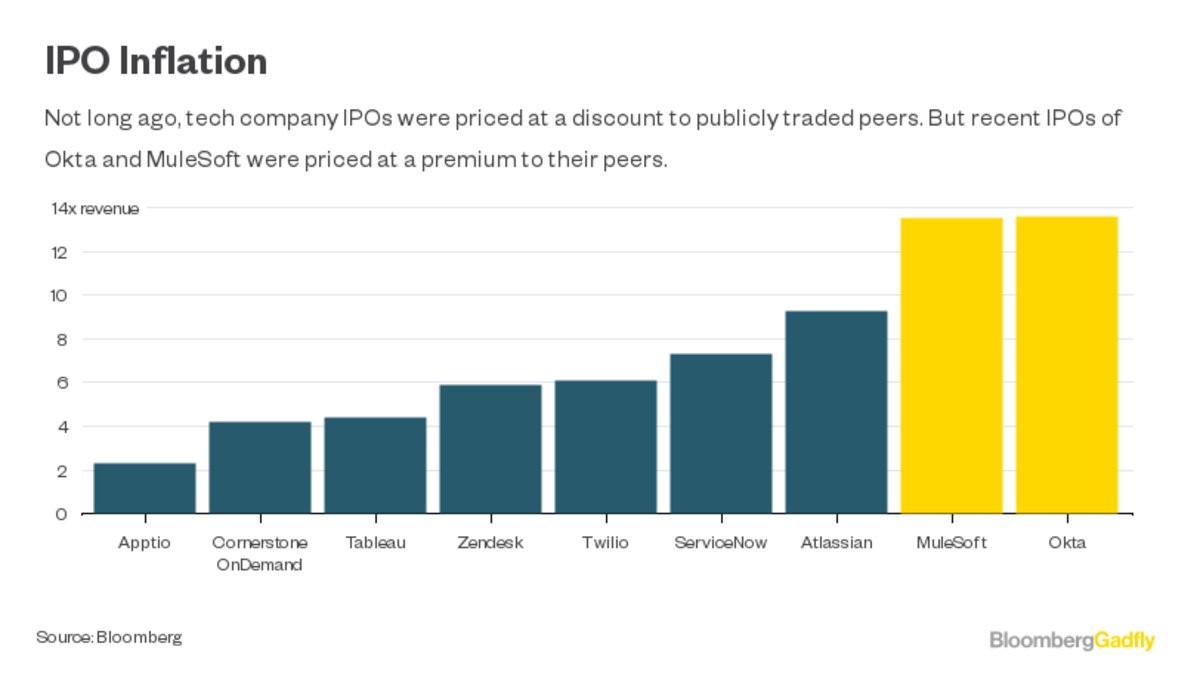

There are many facts which support stocks crashing before the next twelve months. I’m not saying I know for certain whether it will happen, but my arguments serve to caution investors who think it will be easy to make money in stocks in the medium term. As you can see in the chart below, the tech IPO market has become heated like the tech bubble of the 1990s. Snap has been part of the opening of the floodgates for tech firms getting high valuations at their IPO. As you can see, the recent two IPOs, MuleSoft and Okta, have received higher valuations than their publicly traded peers. Getting a higher valuation than stocks in a market which is at high valuations is quite a stretch. The most anticipated IPOs in the next few quarters are Uber, Dropbox, and Airbnb. You would think they would want to hurry up and go public while the market is hungry for them. Uber’s profitless business will serve as another reminder of the hope trade which is dominating equities.

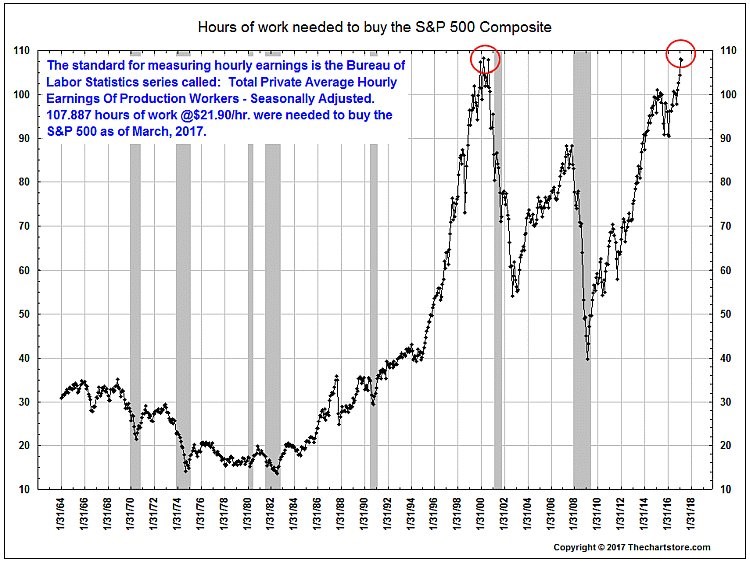

Another way to see how expensive valuations have gotten is shown in the chart below. The reasons why the number hours needed to work to pay for the S&P 500 has gotten so high are because corporate profit margins are near their record high while hourly earnings growth trails CPI and because the market multiple has become inflated. Temporarily inflated earnings operating at peak margins should have low multiples since margins revert to the mean. The argument that firms have used technology and outsourced labor to permanently increase their margins doesn’t hold any water because firms have leveraged their balance sheets to a new record high. If profits were that easy to come by, there would be no need to take on such debt. Another point is that since most firms have similar advantages, competition for market share should eventually crimp margins.

Looking at the historically high corporate margins along with the historically low amount of corporate taxes collected as a percent of GDP makes one question how the GOP will be able to cut corporate taxes which is supposed to boost stocks further. This analysis has been proven to be accurate as the GOP has had a tough time figuring out a plan for tax reform. The logical conclusion to solving a government deficit would be to cut spending, not to lower taxes. Although spending cuts weren’t part of the initial plans of the Trump administration, they may end up happening as the deficit hawks in the GOP may be emboldened by their healthcare win and look for spending cuts when the debt ceiling is hit in the fall.

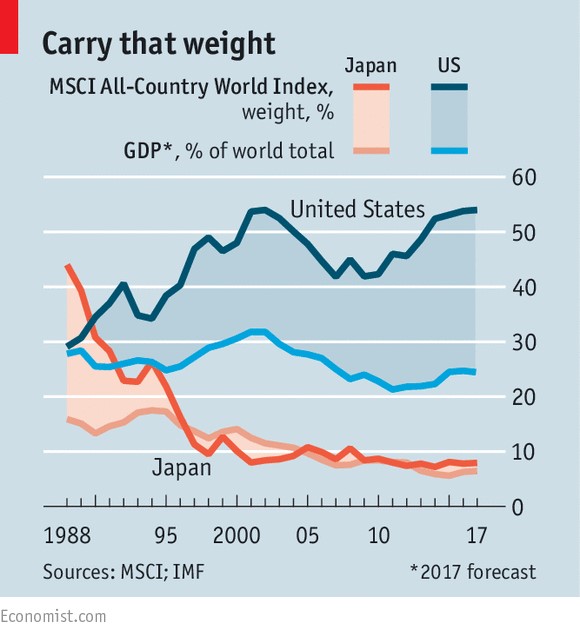

The final chart below shows the percent share of the MSCI All-Country World Index the U.S has as compared with its GDP. It shows how when Japan had an outsized percentage of the index compared with its GDP, it eventually fell back down to Earth. The counterpoint that China has a lower equity market as a percent of its GDP is met with the overvaluation of the European stock market. There will always be undervalued and overvalued equity markets within the world which makes me not buy the claims that the U.S. deserves such a high weighting in the index. To be clear, the problem isn’t with the way the index is formulated, but instead with the level of capital flow into U.S. stocks.

Conclusion

It’s not surprising to see Tesla’s valuation exceed Ford and GM given the momentum its stock has. What is surprising is seeing Piper Jaffray putting a $368 price target on the stock. It gets to that price by using what it calls “a creative valuation methodology.” Adding to this nonsense, Morgan Stanley believes the S&P 500 will rise to 3,000 in twelve months because in 1999 and 2007 stocks rallied for no rational reason. It’s tough to justify irrational stock action by saying it has happened before. This is the exact logic bears utilize when they say the market can crash 20% in one day because the Dow fell 22.6% in 1987. I must admit that the excessive valuations make me think a 20% fall in one day is more likely than a 30% rise in the next year, but I wouldn’t expect either.