Legal Costs & Trading Dog Goldman Sachs

I like to review the notable earnings reports to get a closer look at the overall numbers. Earnings season looks great. Specific data from a few companies helps us understand the direction of corporate earnings. The two earnings reports I’ll discuss here are Goldman Sachs, which reported Tuesday, and Morgan Stanley, which reported Wednesday.

Just like the other banks, Goldman Sachs had high profit growth. Profits were up 40% to $2.57 billion. EPS was $5.98 which beat estimates for $4.66 and revenues were $9.4 billion which beat estimates for $8.74 billion. Even with these results, the stock fell 0.18% on Tuesday. The stock was up 3.66% in the past year as of Tuesday’s close, so it’s not as if the stock is overbought. Investors simply didn’t like the hair on the quarter. Hair is when there are specifics which ruin a good headline report.

One strand of hair was legal expenses. Non-compensation expenses were up 24% to $2.66 billion which was $200 million more than expected. Another strand of hair was weakness in trading. Fixed income trading revenues were $1.68 billion which beat estimates by $30 million. Equity trading revenues were $1.89 billion which missed estimates by $20 million. Other banks had 20% growth in equities trading revenue, meaning Goldman Sachs lost market share. Volatility wasn’t very high in Q2 compared to Q1, but it was higher than 2017.

Investing and lending saw a 23% increase in revenues to $1.94 billion which beat estimates by $300 million. Investment banking and investment management reported revenues of $2.05 billion and $1.84 billion, beating estimates by $210 million and $160 million respectively. There are two other notables about the quarter. Firstly, the firm had to maintain its buyback and dividend because preparation for the tax plan forced it to fail the annual stress test. Next year, the bank will likely get a bigger than usual dividend and buyback increase to make up for that temporary alteration. That could cause the stock to underperform this year. Secondly, 12 year CEO Lloyd Blankfein is retiring on October 1st. He will be replaced by the bank’s president, David Solomon.

Morgan Stanley’s Steller Earnings

Morgan Stanley had a perfect earnings report which is why the stock was up 2.81% on Wednesday. After falling over 20% from its January peak, the stock is up 8.3% since July 5th. The financials, led by Morgan Stanley and Bank of America, could get the S&P 500 to a new record high. The headline results all beat estimates by a lot. Profits were $2.44 billion which beat estimates for $2 billion. EPS was $1.30 which beat estimates by 19 cents. Revenues were up 12% to $10.6 billion which beat estimates for $10.1 billion. Equities trading took share from Goldman Sachs as it did $2.5 billion in revenues which beat estimates for $2.29 billion. Bond trading revenues beat estimates by $110 million, coming in at $1.4 billion.

Considering these great results, it’s not surprising to see the stock up so much since it was down 6.2% in the past year as of Tuesday’s close. It should outperform Goldman Sachs at least in the next 3 months. Investment banking revenues were $1.54 billion which beat estimates for $1.7 billion. The two divisions which missed estimates were wealth management and investment management. Their revenues were $4.3 billion and $691 million which missed estimates for $4.43 billion and $707.9 million. Just like Goldman Sachs, Morgan Stanley ran into trouble with its annual stress test which is why its buyback program is stuck at $4.7 billion. Its quarterly dividend was raised by 5 cents to 30 cents.

Earnings Season Getting Better

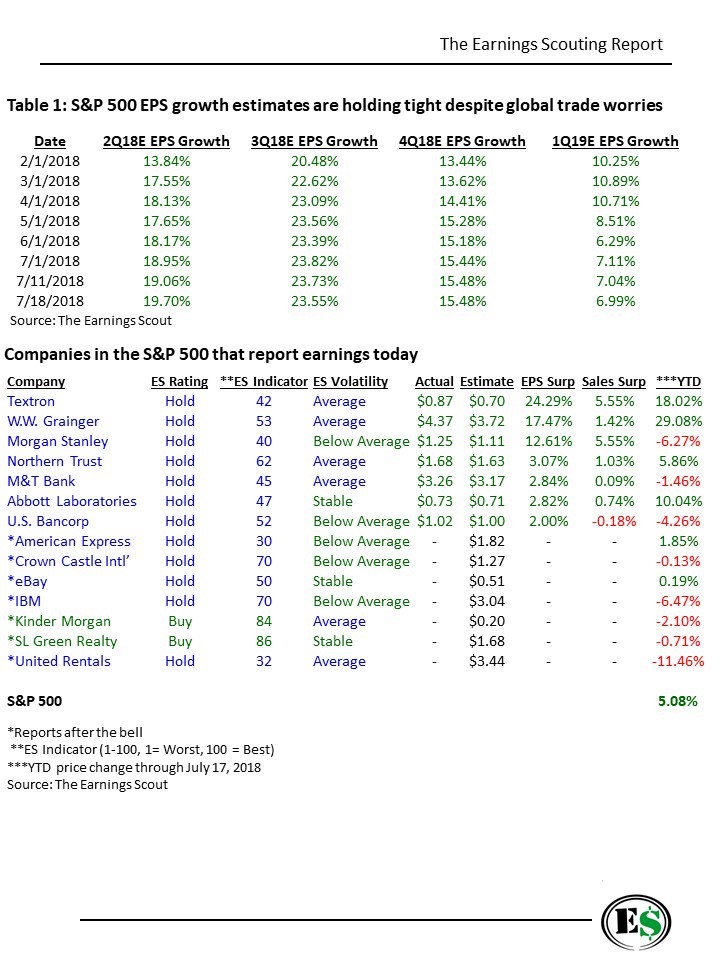

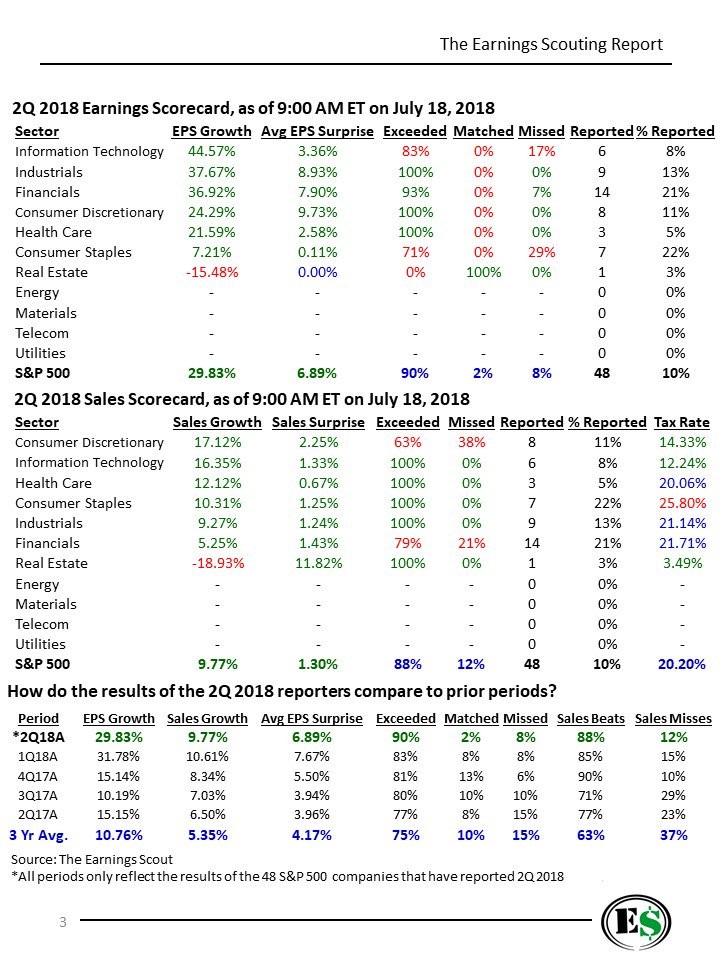

With the ECRI leading indicator showing a slowdown is coming in the second half of 2018 and the yield curve pointing to a recession in 2020, there are worries about the future of this cycle. However, for now stocks must go higher because earnings look strong. As you can see from the chart below, Q2 EPS growth is on pace to be 19.7% if you combine the current reports with the estimates for firms which haven’t reported yet. As of 5:00 PM on Wednesday, out of the 55 firms which have reported earnings, 91% have beaten EPS estimates; they have an average growth rate of 28.75%. 84% have beaten sales growth estimates; the average growth rate is 9.48%. Since the last time I checked, the EPS beat rate is up by 4% and the sales beat rate is down by 3%.

The top chart below shows the earnings estimates for Q3 2018 and Q1 2019 have fallen slightly, while the estimates for Q4 were flat. The fact that earnings growth will fall dramatically in Q4 and Q1 2019 doesn’t matter, but their recent changes do. Furthermore, the 6.99% EPS growth in Q1 justifies my estimation that the stock market should increase about 5% to 10% this year. If it is up more than 10% in 2018, I will be bearish because it is getting more expensive and the risk of a recession is slowly increasing.

The chart below doesn’t include the earnings reports after the close on Wednesday. However, it’s still great to see the latest sector breakdown. There a few notable takeaways from these charts. Firstly, now 9 out of 9 industrial firms have beaten estimates which is remarkable because the sector was supposed to be beleaguered by tariffs and the sagging manufacturing market outside of America. Another great stat is the EPS growth is closing in on the Q1 2018 growth rate. I think it will end up slightly less than Q1, but still very high. The EPS surprise rate is now lower than Q1 2018, but the beat rate is still better.

It will be up to energy, materials, healthcare, and the big tech names to complete this great quarter with more positive results. I will be concerned if the future estimates continue to fall as the rest of the earnings results come out. Q3 might see estimates fall during the quarter unlike the past two quarters.

1 Comment

Souraphong Ratsaphong

July 19, 2018Great report!! Thank you.