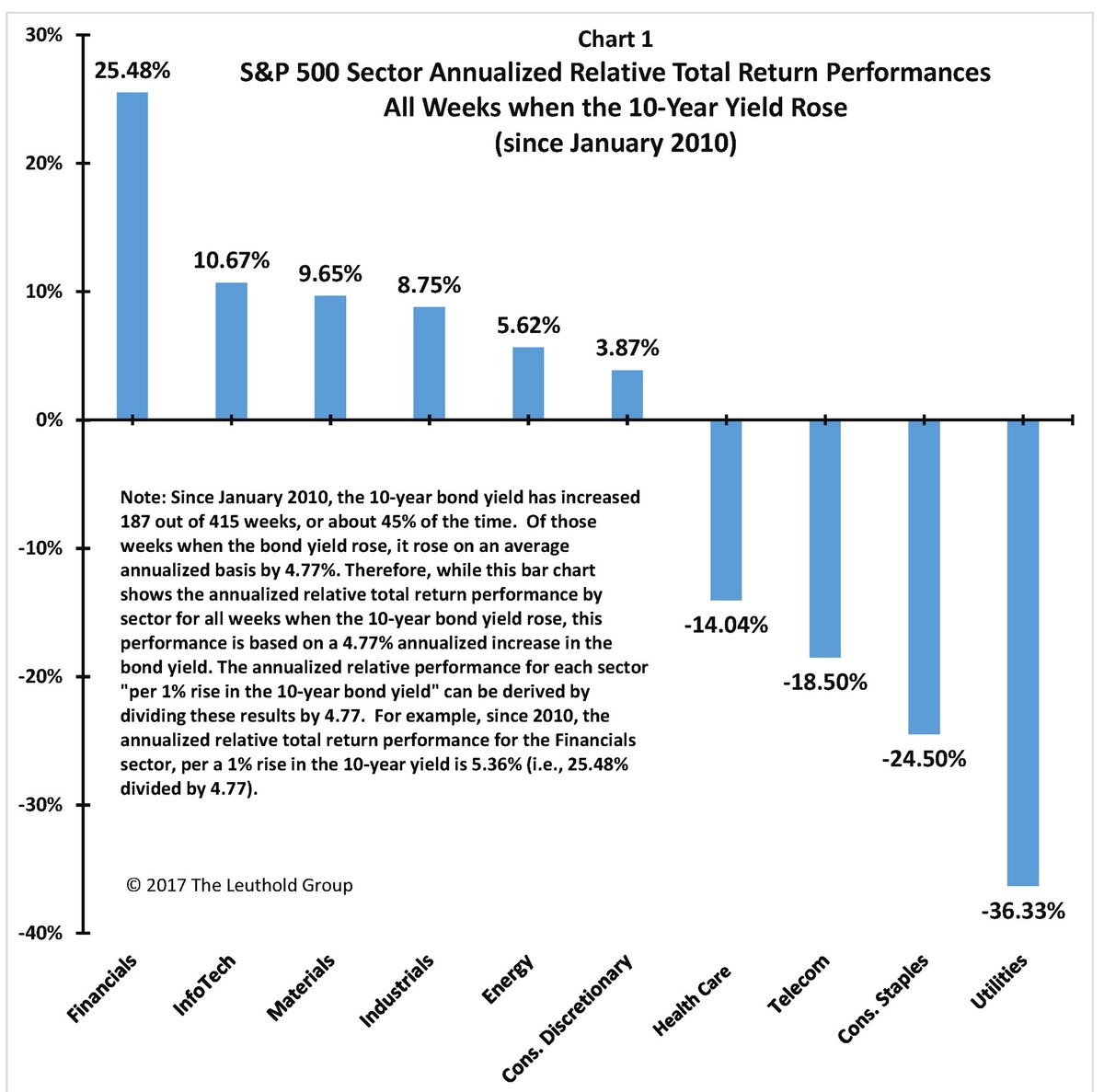

Financials Do Well When The 10 Year Yield Rises

We’ve discussed which sectors do well when the yield curve flattens. Now let’s look at which sectors do well when the 10 year bond yield goes up. The 10 year bond has gone up 45% of the time since 2010. I think inflation will increase in the next year. This should increase long bond yields. With this in mind, it makes sense to buy financials and sell utilities. There are a few trends I’m following. As I mentioned, the yield curve is flattening and inflation might increase. The other two are the effect of the tax cuts and QE tightening. The strategy investors should employ is to figure out which sectors do the best in all circumstances combined and buy them. The best way to invest is to make bets in which you have multiple ways to win. Buying a sector which does well at the end of the cycle when treasury yields are rising would help you do just that.

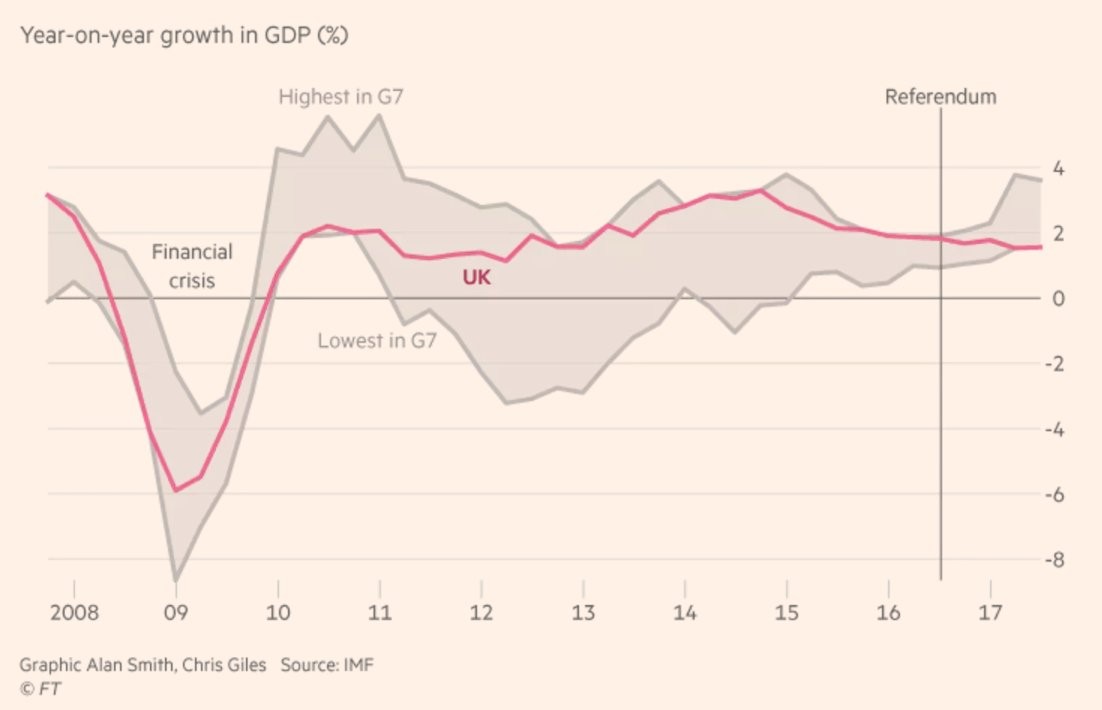

Indian & U.K Effected By Public Policy

The two markets which were the most negatively effected by politics in 2017 were the U.K. and India. Brazil is lucky its economy recovered in 2017 as it avoided making this list again even though there have been a few corruption scandals among its public officials. The U.K. has struggled as I discussed in my article on the Brexit. The uncertainty and the responses to this vote have been negatively impacting the economy. The establishment in change doesn’t like the concept of a Brexit, so they will be taken kicking and screaming towards the finish line. The battle to figure out which path the country goes down has led to uncertainty. The chart below shows the negative impact on the country’s economy. As you can see, the U.K. has fallen from having the highest GDP growth rate in the G7 to the lowest ever since the referendum. It is dragging down the minimum growth among the G7 nations as most experienced a rebound in 2017. The possible results of Brexit are anywhere from a severe decline in trade growth to very little changing.

The Indian economy has been hindered by the demonetization that Prime Minister Modi enacted by surprise in the fall of 2016. It was unknown what the effect would be at the time, but now it’s clear it was a mistake as all the money was returned to the government, so no tax evaders were found. Instead it made life more difficult for small businesses as they usually deal with cash, especially in the poor areas. The reason I’m discussing the Indian economy and political situation is because there was an election in Modi’s home state on Monday. Modi won the election, but there was a scare after the exit polls came out as some feared he would lose. The fear caused the Indian stock market to fall 867 points at the open. That is a drop of 2.59%. When the market realized Modi won, it rallied back to close up 0.41%. There will be more state elections and a national election in 2019. The concern about the demonetization is looking in the rear view mirror. I think it was bad policy, but it’s over now. The future depends on if India can enact reforms to end corruption and if it can open up its markets to free trade instead of being very protectionist.

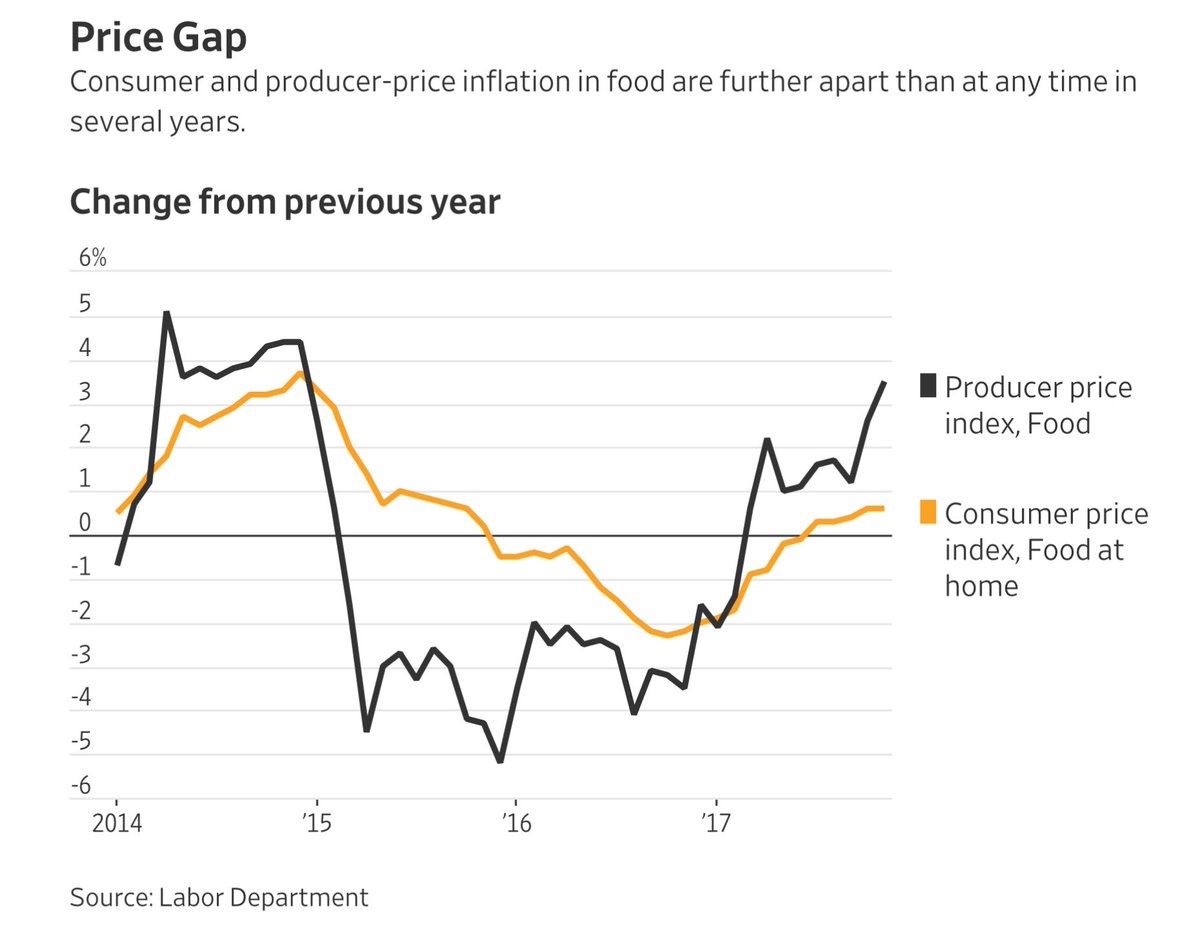

Inflation Gap

We’ve discussed inflation in many articles because it’s the most important data point in macroeconomics. One trend which I haven’t mentioned is that the producer price index for food has gone up much more than the consumer price index for food. I consider food prices to be critical to the inflation story since shelter inflation has started to stabilize. The dynamic playing out in food is that the prices supermarkets pay are increasing, but they aren’t passing down those price increases to the consumer. This hurts the supermarkets’ margins. Looking from a macro lens, we don’t care about the supermarkets; we care about whether the consumer prices will accelerate.

Grocers, discounters, and online retailers increased their prices by 0.6% while the producer price index increased 3.5% in November as you can see from the chart below. This is related to the Amazon effect as the online retailer has been cutting prices on avocados, organic milk, and chicken ever since it bought Whole Foods a few months ago. I think there’s a psychological effect of Amazon entering a market. Before a company has the chance to see Amazon take market share from them, like it has in many other industries, they are cutting prices to stay competitive. Amazon either takes market share from firms or it watches them die as they cut prices below viability. Inflation would be higher without Amazon.

Amazon is one of the reasons the Phillips curve hasn’t been working. It’s ironic because Amazon is suppressing inflation which is helping its stock since it has a high multiple. High multiple growth stocks get crushed when there is high inflation. I am amazed by the leash investors have given Amazon in terms of buying it despite its low margins. However, Amazon looks like a cheap stock compared to the recent craze in cryptocurrencies and the blockchain.

Blockchain Bubble Gets Worrisome

Any firms which add “blockchain” to their company instantly see millions of dollars of gains in their market cap. The tide that is this Christmas rally in stocks is certainly lifting all ships. Usually when euphoria is the highest, the companies with the worst fundamentals rally. To be clear, I’m not saying Amazon has the worst fundamentals. I’m saying Longfin stock going up 2,400% because it acquired a blockchain company that has existed for 2 weeks is probably an unsustainable bubble. The speculation in cryptocurrencies is looking like it will be a disaster for the market. Anyone with experience watching these newly created coins having a $635 billion market cap combined with the S&P 500 rallying of over 20% this year can see this era of euphoria will end badly.