The previous discussion about the labor market showed how it’s tough to quantify the slack in the labor market. The Fed has been relatively dovish at the end of this cycle even though the unemployment rate suggests the labor market is near full employment. Another reason why the Fed hasn’t been hawkish has been the lack of inflation. This is related to the labor market discussion because the extra slack in the labor market has prevented labor price inflation. The issue with quantifying the slack in the labor market affects the Fed’s rate hike timing.

Besides labor inflation, the other crucial source of inflation and disinflation is energy. Don’t be confused with the reason core inflation is measured. The core rate is not studied because food and energy costs are not important. It is to highlight what the other aspects are doing without the volatility in energy and food. Whether economists decide to ignore energy costs is irrelevant because it’s still a real cost which affects businesses and consumers. If oil prices doubled overnight, the consumer would drive less. They don’t have the luxury of excluding that cost because it’s volatile.

Changes in energy prices wreak havoc on the CPI. Instead of ignoring the effects energy has on CPI, I think it’s best to call out the changes within the number. The problem with this method for the Fed is that it would make the Fed’s inflation targeting philosophy look silly. The actual data on inflation has been making the Fed look silly for years because it usually misses the 2% target, but it hasn’t caused the Fed to change. As you can see in the chart below, oil price inflation caused the CPI to get above 2% from late 2016 until now.

This effect energy has on CPI isn’t a new phenomenon. The chart below shows changes in energy CPI has been highly correlated with CPI. This isn’t to say oil is the only driver of inflation because this is partially affected by the changes in the dollar as well as global demand for commodities which drive all commodities in a highly-correlated fashion. The main point of this chart is to show how volatile energy can be and how most other aspects aren’t as volatile which is why changes in oil prices can move CPI so much. It also shows the previous point I made about how CPI usually doesn’t stay at the Fed’s 2% goal.

The positive effect oil has on CPI is now starting to wane quickly. My prediction for oil to fall into the high $30s hasn’t worked out as the production cuts from OPEC and the tensions in the middle east have caused oil to rebound from the high $40s back to the low $50s. As you can see, the base effect of oil will be negligible in a few months if oil stays at $53 per barrel. As of Tuesday, the first Fed meeting which shows the Fed expected to hike rates is September. There has been movement in the readings towards later rate hikes because of the volatility in the equity market. By September the Fed will have lower CPI on its side if it decides to not hike rates.

While the exact amount of slack in the labor market is tough to quantify, the source of the slack is easy to determine. Although millennials are the most educated generation ever, they have had a tough time getting that high paying job they thought they would get after graduation. There’s a multitude of factors at play which are causing this trend. One is that student loans are being given for any major. Some majors aren’t applicable to jobs. When I was in college a few years ago, I would tell older adults that the goal of college was the prepare you for a job. They were somewhat impressed which is shows how the point of college has been distorted. You would think that college being more expensive than ever would make students care more about getting their money’s worth, but that’s not the case. When people go to college that shouldn’t be there because a trade school would be better, bad results occur. A degree used to mean more than it does now because so many people have one.

Student loans bog down millennials and cause them to start their lives later. When I say start their lives, I’m referring to the delayed household formation. In a recent poll millennials say they don’t consider themselves adults until 30. That’s not because millennials are immature as some people like to portray them. It’s simply a matter of math. When you have $50,000 in student loans and can’t move out of your parent’s house, you don’t feel like an adult.

Student loans are tough to default on because there’s no asset for the bank to take back. It pushes up default rates on other loans. The chart below breaks down the share of default likelihood by age groups. As you can see over 50% of 21-34 year old people said they were likely to default on loans.

Conclusion

The slack in the labor market is made up mainly by millennials. They also make up a large portion of the part time workers looking for full-time jobs. One reason for this pain millennials face is older people are working more. They have more experience which makes them valued over younger workers. Younger workers are saddled with student loan debt which is already starting to be defaulted on a heightened clip.

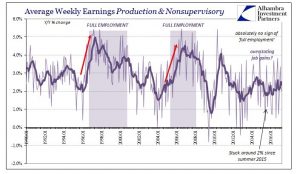

The Fed wants to raise rates because if the economy falls into a recession, they won’t have any flexibility with cutting rates to soothe the negative headwinds the credit market faces. The argument against rate hikes is the millennials who haven’t gotten jobs yet need the Fed to be dovish to finally feel the benefits of the recovery. There will always be groups which don’t do well when the economy is strong, but this group is so large this cycle that the aggregate hourly earnings growth hasn’t been able to meet previous levels of growth. As you can see from the chart, earnings growth is stuck around 2% which is about half the rate it has grown at historically when the economy is at full employment.