In my article yesterday, I mentioned the market has been in a very narrow range. Today data on the S&P 500’s range was posted on CNBC. The 1.6% range the S&P 500 has been in, in January is the narrowest range since November 1965. The tight August range was 2.1% which was the narrowest since December 1993. There’s still five more trading days in the month, so it can still breakout of this range. Technical analysis will tell you tight ranges lead to an explosion in the market one way, but I don’t buy into that especially in this central bank driven market. There will be a time when it unwinds, but I wouldn’t bet on it happening in the next few weeks because of this constriction.

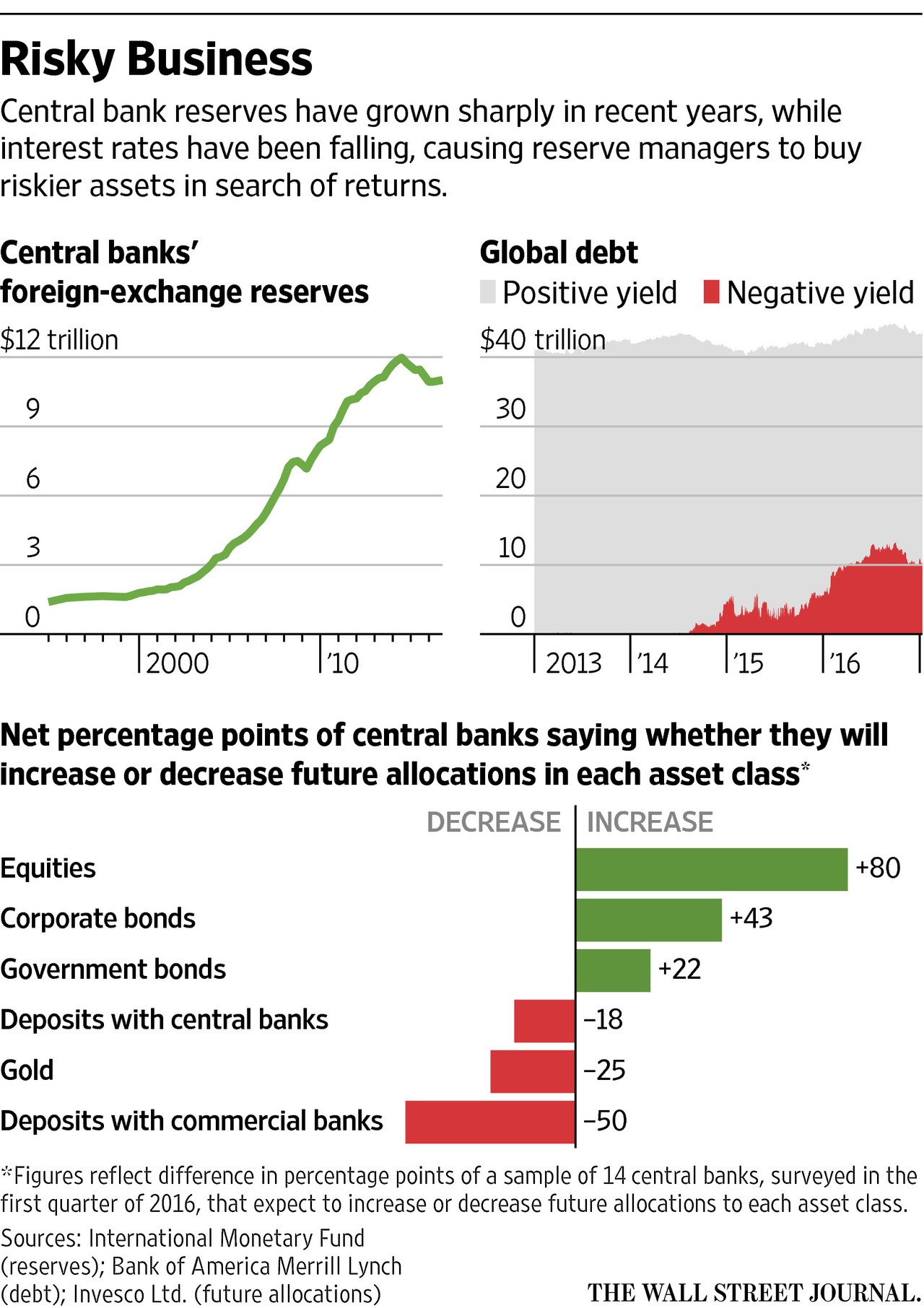

When the central bank buys government bonds, it pushes conservative investors up the risk curve which means it doesn’t matter what the central bank buys. Each asset purchase causes a bubble in that asset and echo bubbles in other assets. Unfortunately, the Fed has exported its plans to ‘solve’ economic crises as other central banks are copying its policies. There is not a conspiracy where the Fed told the other central to do its ‘dirty work.’ What happened was other central banks decided it would be a good idea to copy the Fed. When the Fed saw this occurring, it stopped its own balance sheet expansion. As you can see negative yields and central banks’ foreign exchange reserves have skyrocketed in the past few years and have recently pulled back slightly. There will be no unwind of the total assets purchased. According to the Wall Street Journal survey of 14 central banks, in Q1 2016, 43% said they’d increase their allocation of corporate bonds and 80% said they’d increase their buying of stocks. The central banks are now going up the risk curve as they’ve run out of corporate bonds to buy given many have begun yielding a negative interest rate. Is investing in start-ups and leveraged ETFs next?

This central bank intervention has caused the overvaluation seen in the chart below. The NYSE median price to cash flow ratio is near a record high. This is one of many valuation metrics screaming we are in a bubble. It’s weird to say that the tech bubble was much more rational than this current market. Yes, speculators were buying stocks with no profits and bidding them through the roof, but at least they were companies which had growth potential. The internet was the most revolutionary technology in our lifetimes, so I understand the enthusiasm.

This market is being driven by passive investing. People are parking their savings in the stock market because it has offered great returns lately. When stocks are providing great returns, wise investors know it’s time to be cautious. In the tech bubble, investors knew what they were buying, so they may have had more conviction in their holdings. Countering that conviction was the fact that they were watching their stocks everyday which is why selling pressure spread quickly. This time investors don’t know what they’re buying, so there’s lower conviction. However, they don’t check their holdings everyday which may slow selling pressure. I think these differences counteract each other meaning both crashes will be similar. Passive investing is like real estate investing was 10 years ago. People thought it was common sense to buy real estate because it would always move higher. When common sense becomes too common and everyone is in a trade, it ends badly.

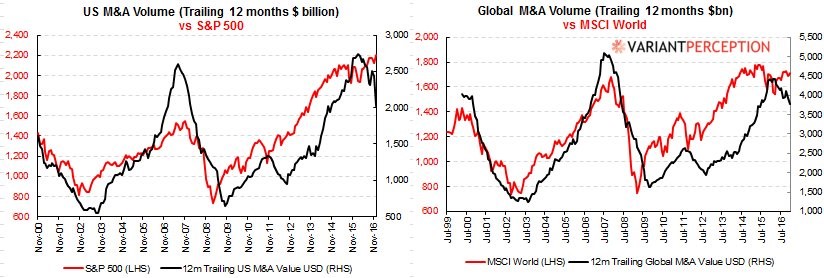

Timing this cycle has been made tougher by central bank intervention. Usually there is peak mania in the M&A market around the market peaks. You see risky activity like the Microsoft deal to buy LinkedIn and the AOL-Time Warner merger. When optimism gets too high, managers take a leap of faith which often doesn’t work out. The motivation to take these risks occurs because at the peak, firms are awash in cash, but are beginning to see revenue deceleration. This time has been different. The S&P 500 has rallied while U.S. M&A volume has taken a sharp dip. The MSCI World Index has also increased while the Global M&A volume has fallen.

The market has gotten excited about rising yields and inflation expectations. If yields fall back down, it could lead investors to lose confidence in the central banks. It’s not that inflation is necessarily a good thing, but since central bankers have been trying to boost inflation for years, when it did increase, investors became more confident in the central bankers. Inflation increased because of optimism related to the Trump victory and oil price increases which was partially due to the OPEC deal to cut production. However, whether the central bankers created this inflation has become immaterial to the narrative.

The only way to topple this equity market is for investors to lose confidence in the Fed and other central bankers. If treasuries rally again, this can do the trick because it will show that the central banks can’t create inflation. The other way would be for inflation to get out of hand, but that doesn’t seem likely in the near term. The high inflation has been in asset bubbles like stocks and bonds, but the Fed and everyday Americans like that type of bubble until it bursts. The chart below shows the latest net short position in treasuries. It’s tough to say if a mean regression would cause treasuries to rally again or if it needs a catalyst to change direction.

Conclusion

In Q1 2016, 80% of central bankers claimed they would buy stocks. Unsurprisingly, stocks rallied due to that buying and other speculation. It has pushed the market to record valuations. This situation wouldn’t work without private investors’ support. Confidence in the central bank can wane if inflation starts to decrease and treasuries rally again. This could catalyze the unwind in the market. I think the amount of negative yielding bonds would have to exceed the peak in July to get market participants worried enough to start going into cash.