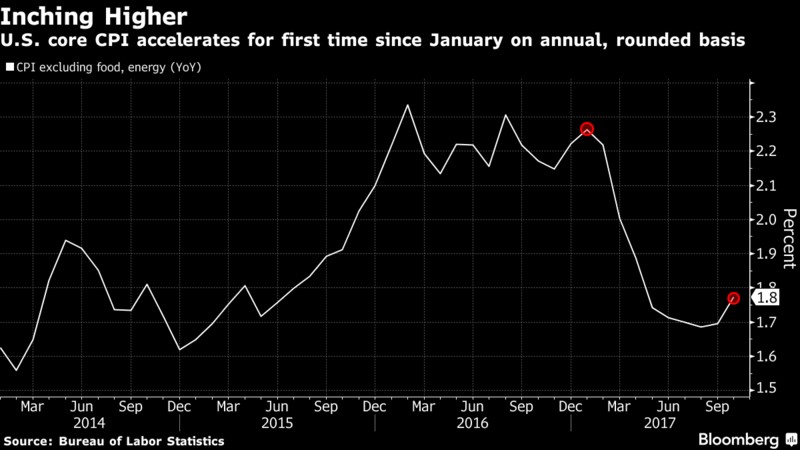

Inflation Picked Up

The latest CPI report for October gives support to that prediction as we saw core CPI accelerate for the first time since January as you can see in the chart below. The CPI increased 0.1% month over month and 2% year over year. Core CPI was up 0.2% month over month and 1.8% year over year which beat estimates by 0.1%. The inflation rate is getting closer to the Fed’s goals even while it starts to unwind the balance sheet. This supports the already obvious point that the Fed will raise rates in December. The housing cost index was up 0.3%. Wireless phone service was up. That was an aspect which Yellen has complaining about for the past few months. The 1% decline in energy hurt inflation. With the recent oil price increase, the chance of energy prices increasing in next month’s report are high. As I have said, there’s slack in the inflation metric where a few tenths of a percent increase isn’t bad. The issue will be if the inflation rate starts to get out of control in 2018. That would be the beginning of the end of the business cycle and cause a selloff in tech stocks. It could be the story of 2018.

Update On The Fed

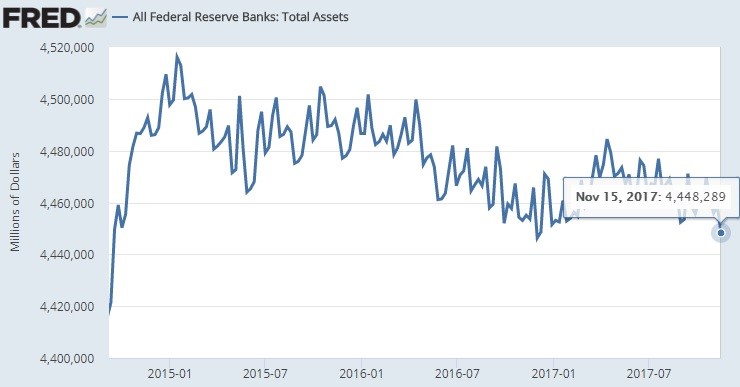

We’ve been trying to get a reading on how the market will react to the unwind of the balance sheet ever since the Fed started this new policy. However, the process has started so slowly, there’s not much to analyze. The chart below gives an updated view of the balance sheet. It still isn’t even at the lowest point of 2017. The decline from 2015 to 2017 was sharper than the decline this year. We will need to wait until 2018, to get a better reading on what will happen to the markets. As I mentioned, the Fed is about to raise rates in 3 weeks. There’s a 91.5% chance of 1 hike and an 8.5% chance of 2 hikes. I doubt Yellen would hike rates an extra 25 basis points just as she is about to leave. It will be up to Powell in 2018 to push rates up further. Given how close the Fed is to its long term expectation for rates, I think 2018 or 2019 could be the last year of hikes.

According to the dot plot, the Fed reaches its longer run projection in 2019. I think the Fed will raise rates twice in 2018. According to the CME Group Fed Watch tool, the most popular guess is for the Fed raise rates twice. The tool shows there is a 54.2% chance the Fed raises rates at least twice next year. There hasn’t been a noticeable change in the policy expectations by the market as a result of the changes in personnel at the Fed. The other indicator to keep in mind besides the CPI is the yield curve. The 10 year yield minus the 2 year yield has fallen to 60 basis points. Its quick fall is worrisome as it points to a recession in 2019 or 2020. If the Fed raises rates twice next year, it can invert the yield curve. Bond investors might see this latest increase in inflation as a sign that the business cycle is ending.

Retail Sales

Besides the positive CPI report, the Fed also welcomed positive results from the retail sales report. Retail sales were up 0.2% month over month which beat estimates by 0.2%. Total yearly sales in the October report showed a 4.6% increase. The ecommerce sales report was also released. It showed the adjusted quarter over quarter sales growth was 3.6%. On a non-adjusted basis, quarter over quarter sales were up 1.9%. On an adjusted and non-adjusted basis, year over year sales were up 15.5%. On an adjusted basis, online sales accounted for 9.1% of retail sales and on a non-adjusted basis it accounted for 8.4% of retail sales. The Bloomberg Consumer Comfort Index came in at 52.1 which was up from 51.5 the week before. The peak was 53.3. Given how confident consumers are, I expect the 2017 holiday season to be one of the most successful in this expansion.

GDP Estimates Singing A Positive Tune

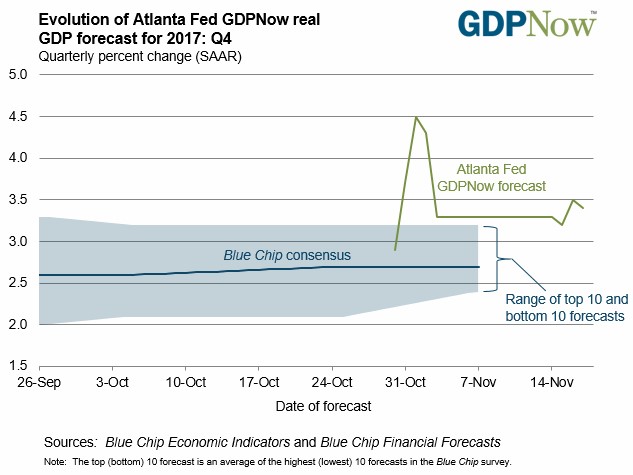

The Q4 GDP report might be the best of the year. Next week we get the first revision for Q3. If it’s revised higher, I may need to rescind that statement. As of now, Q4 looks like the leader as the Atlanta Fed expects 3.4% growth as you can see in the chart below. The forecast was moved up by 0.2% when it was last updated on November 17th because of industrial production report. The new residential construction report sent the forecast lower. The NY Fed Nowcast is extremely optimistic as it has GDP growth coming in at 3.82%. That estimate was also updated on November 17th. It was pushed higher because of the industrial production report, the capacity to utilization report, the housing starts report, and the building permits report. The St. Louis Fed report is the most bearish of the bunch as it expects only 2.63% growth. That means the average growth expected in Q4 is 3.28% which is slightly above the 3.1% growth rate seen in Q2. If the Q3 report stays at 3% and the Q4 report comes in at 3.28%, the 2017 GDP growth rate will be 2.645% which would be the fastest growth in this expansion.

Conclusion

As you can see, Q4 is shaping up to be a great quarter and the holiday season is looking like it will be a blowout. That’s what you would expect from an economy when the stock market is up 15.33% on the year and the realized volatility for the year shows this to be one of the calmest markets ever. Next year will be different as the Fed comes closer to completing its hike cycle and inflation spikes. If inflation stays benign, we could be looking at a few more years of growth